Instant Home Estimate

For your home value estimate, enter the access code you received on the postcard, just click here:

![What State Gives You the Most ‘Bang for Your Buck’? [INFOGRAPHIC] | Simplifying The Market](http://d39ah2zlibpm3g.cloudfront.net/wp-content/uploads/2017/08/04155449/STM-Share.jpg)

Posted in For Buyers, For Sellers, Infographics

The National Association of Realtors (NAR) keeps historical data on many aspects of homeownership. One of the data points that has changed dramatically is the median tenure of a family in a home, meaning how long a family stays in a home prior to moving. As the graph below shows, for over twenty years (1985-2008), the median tenure averaged exactly six years. However, since 2008, that average is almost nine years – an increase of almost 50%.

The reasons for this change are plentiful!

The fall in home prices during the housing crisis left many homeowners in a negative equity situation (where their home was worth less than the mortgage on the property). Also, the uncertainty of the economy made some homeowners much more fiscally conservative about making a move.

With home prices rising dramatically over the last several years, 93.9% of homes with a mortgage are now in a positive equity situation with 78.8% of them having at least 20% equity, according to CoreLogic.

With the economy coming back and wages starting to increase, many homeowners are in a much better financial situation than they were just a few short years ago.

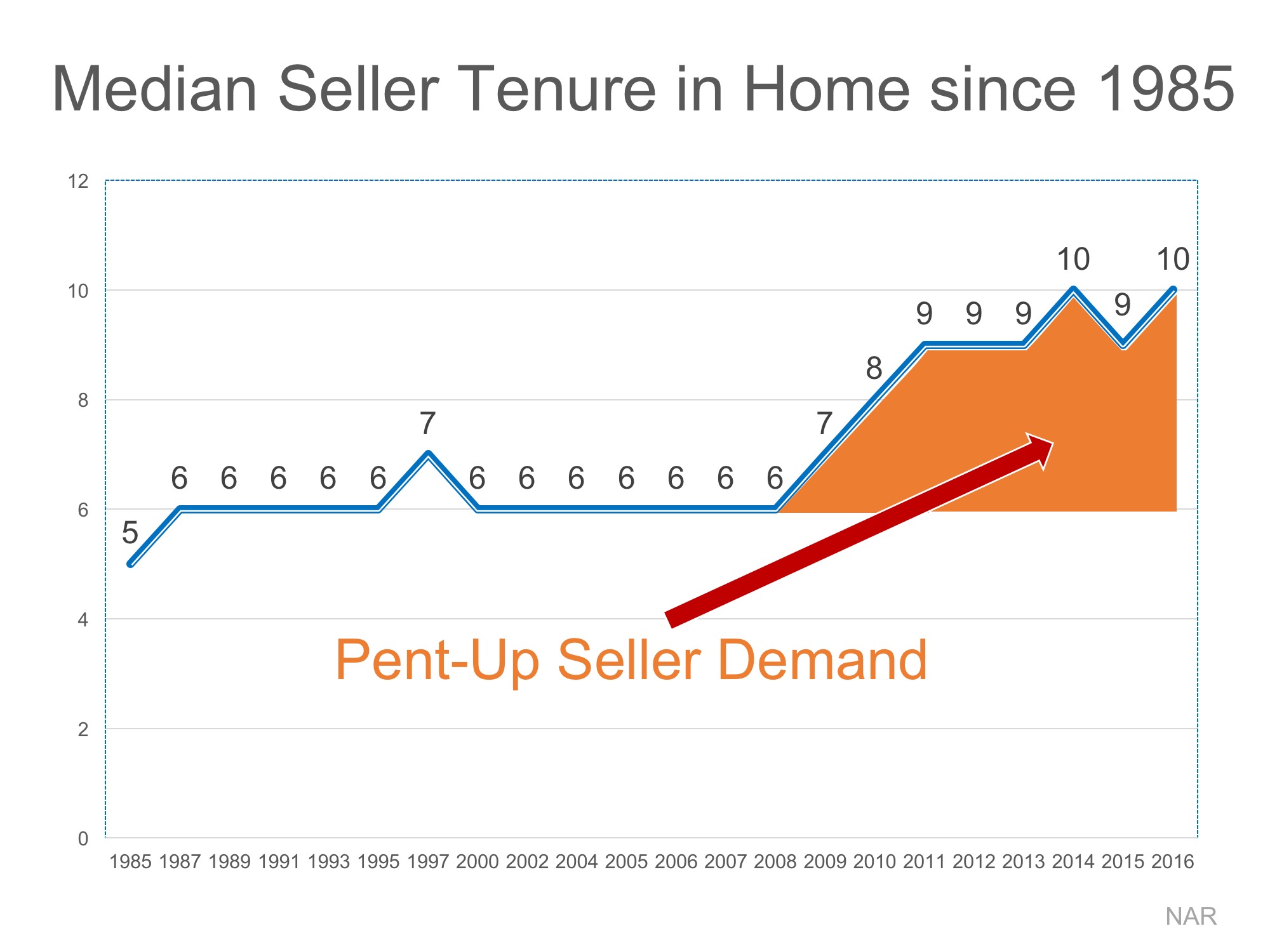

One other reason for the increase was brought to light by NAR in their 2017 Home Buyer and Seller Generational Trends Report. According to the report,

“Sellers 36 years and younger stayed in their home for six years…”

These homeowners who are either looking for more space to accommodate their growing families or for better school districts are more likely to move more often (compared to 10 years for typical sellers in 2016). The homeownership rate among young families, however, has still not caught up to previous generations, resulting in the jump we have seen in median tenure!

Many believe that a large portion of homeowners are not in a house that is best for their current family circumstance; They could be baby boomers living in an empty, four-bedroom colonial, or a millennial couple living in a one-bedroom condo planning to start a family.

These homeowners are ready to make a move, and since a lack of housing inventory is still a major challenge in the current housing market, this could be great news.

Posted in For Buyers, For Sellers, Housing Market Updates, Move-Up Buyers

Recent headlines exclaimed the homeownership rate, as reported by the Census Bureau, rose again in the second quarter of 2017. What didn’t get much attention in the reports is that the homeownership rate for American households under the age of 35 increased a full percentage point from last quarter’s 34.3% to 35.3%. Millennials proved to have the highest increase of any age group.

This came as a surprise to some considering Millennials have come to be known as the “renter” generation. However, a new study by First American, 6 Trends Poised to Reshape Homeownership Demand, revealed reasons why homeownership numbers will continue to increase for Millennials.

Why does that matter? First American explains:

“Our model shows that, all other factors being equal, the likelihood of homeownership increases by 3 percent for those that earn a bachelor’s degree over those with a high school degree. The likelihood of homeownership jumps another 3 percent for those that earn a graduate degree.”

The more educated, the better the likelihood for homeownership. And, as we mentioned: Millennials are the most educated generation in the U.S.

Marriage is a key determinate in homeownership. According to an analysis by First American, the homeownership rate is 30% higher among married couples compared to non-married households.

Millennials have put off marriage in the pursuit of higher education. As this group ages, more and more will marry and purchase a home.

According to the study:

“The homeownership rate is 1.7% higher for households with one or two children compared to households with no children, and it is 5.4 percent higher for households with three or more children.”

The report goes on to say that as Millennials grow older there may be an increase in not just marriage but also in married couples with children. That will probably also create a “corresponding” increase in homeownership demand.

The study goes on to explain that recent gains in income growth and a strengthening economy will also help all generations (including Millennials) be more willing and able to purchase a new home.

We guess the time has come to announce – Here come the Millennials!!

Posted in First Time Home Buyers, For Buyers, Housing Market Updates

There are many benefits to homeownership. One of the top benefits is being able to protect yourself from rising rents by locking in your housing cost for the life of your mortgage.

A recent article by ConsumerAffairs addressed the continuous rise in rents, stating:

“The cost of putting a roof over your head continues to go up. Not only are home prices still rising, but the cost of rent rose 0.5% in June.”

Additionally, in the Joint Center for Housing Studies at Harvard University’s 2017 State of the Nation’s Housing Report, it was revealed that,

“Despite a slight improvement from 2014, fully one-third of US households paid more than 30 percent of their incomes for housing in 2015. Renters continue to be more likely to face cost burdens…the number of cost-burdened renters (21 million) considerably outstrips the number of cost-burdened owners (18 million) even though nearly two-thirds of US households own their homes.”

These households struggle to save for a rainy day and pay other bills, including groceries and healthcare.

As we have previously mentioned, the results of the latest Rent vs. Buy Report from Trulia shows that homeownership remains cheaper than renting with a traditional 30-year fixed rate mortgage in the 100 largest metro areas in the United States.

The updated numbers show that the range is an average of 3.5% less expensive in San Jose (CA), all the way up to 50.1% less expensive in Baton Rouge (LA), and 33.1% nationwide!

Perhaps you have already saved enough to buy your first home. A nationwide survey of about 24,000 renters found that 80% of millennial renters plan to eventually buy a house, but 72% cite affordability as their primary obstacle. Aside from affordability, one in three millennial renters have concerns about their credit scores, and another 53% said that a down payment is an obstacle.

Many first-time homebuyers who believe that they need a large down payment may be holding themselves back from their dream homes. As we have reported before, in many areas of the country, a first-time home buyer can save for a 3% down payment in less than two years. You may have already saved enough!

Don’t get caught in the trap that so many renters are currently in. If you are ready and willing to buy a home, find out if you are able. Let’s get together to determine if you can qualify for a mortgage now!

Posted in First Time Home Buyers, For Buyers

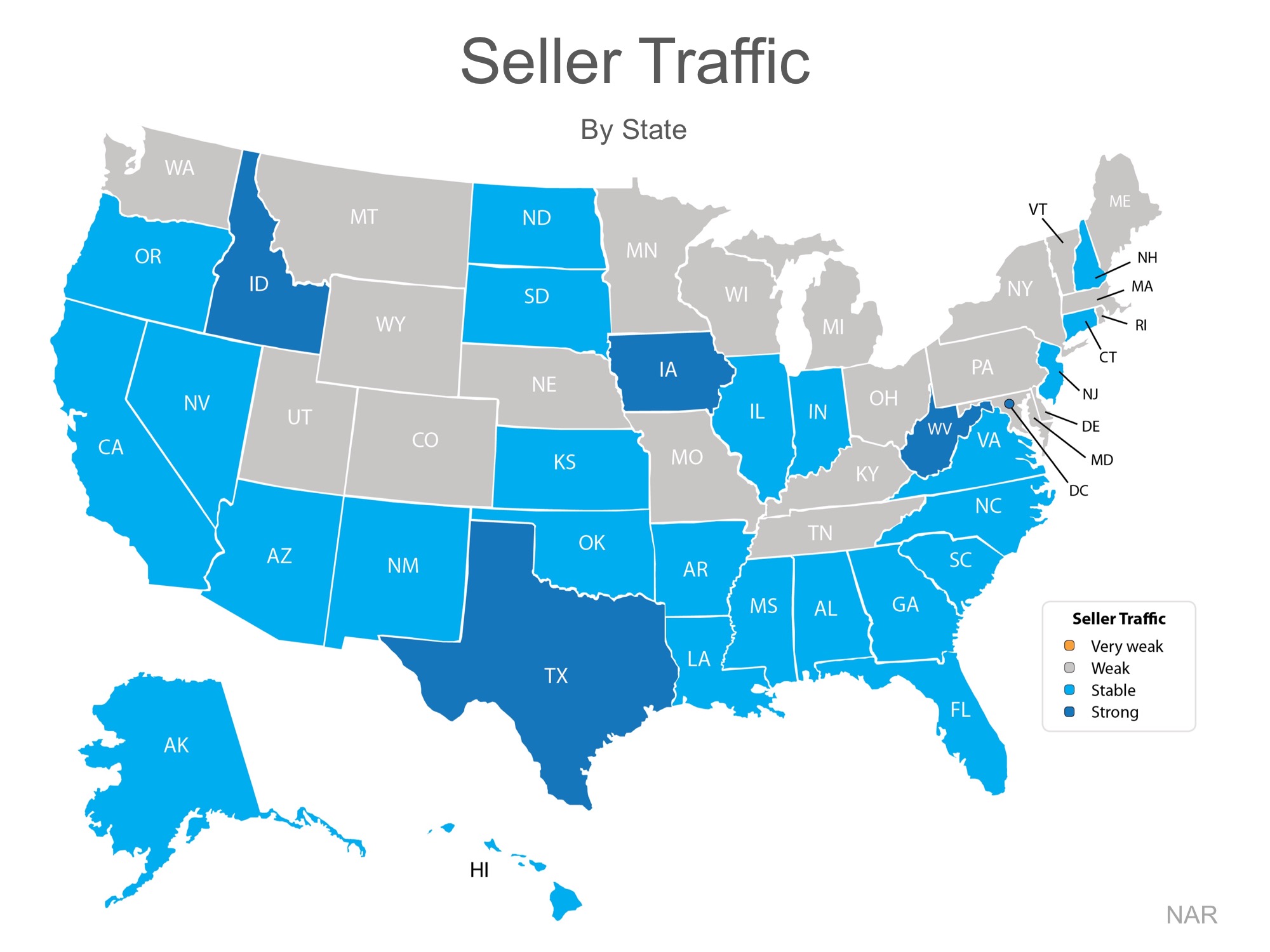

The price of any item is determined by the supply of that item, as well as the market demand. The National Association of REALTORS (NAR) surveys “over 50,000 real estate practitioners about their expectations for home sales, prices and market conditions” for their monthly REALTORS Confidence Index.

Their latest edition sheds some light on the relationship between Seller Traffic (supply) and Buyer Traffic (demand).

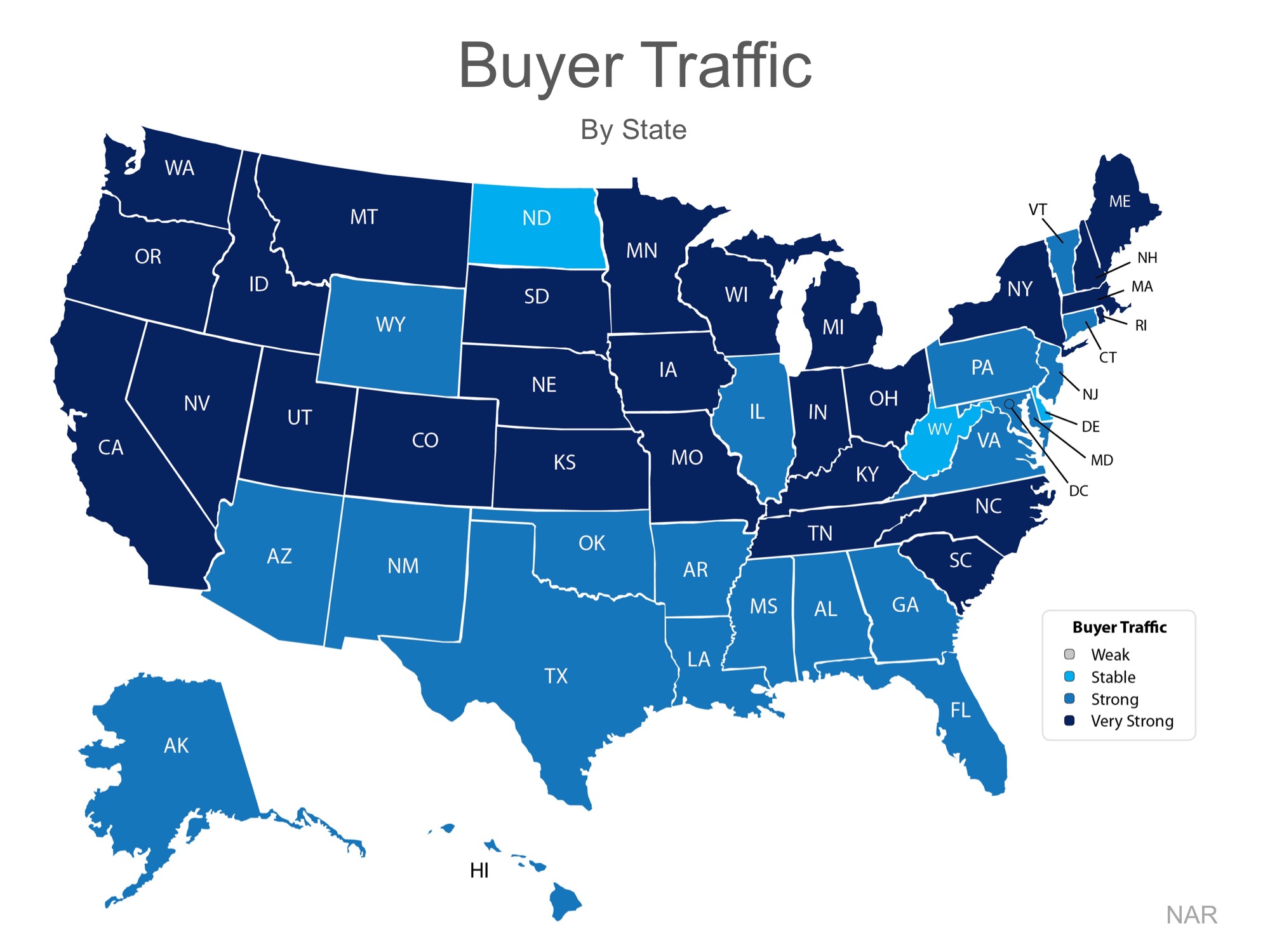

The map below was created after asking the question: “How would you rate buyer traffic in your area?”

The darker the blue, the stronger the demand for homes in that area. Only three states had a ‘stable’ demand level.

The index also asked: “How would you rate seller traffic in your area?”

As you can see from the map below, 21 states report a ‘weak’ sellers traffic, 25 states report a ‘stable’ sellers traffic, only 4 states and DC report a ‘strong’ sellers traffic. Meaning there are far fewer homes on the market than what is needed to satisfy the buyers who are out looking for their dream homes.

Looking at the maps above, it is not hard to see why prices are appreciating in many areas of the country. Until the supply of homes for sale starts to meet the buyer demand, prices will continue to increase. If you are debating listing your home for sale, let’s get together to help you capitalize on the demand in the market now!

Posted in For Buyers, For Sellers

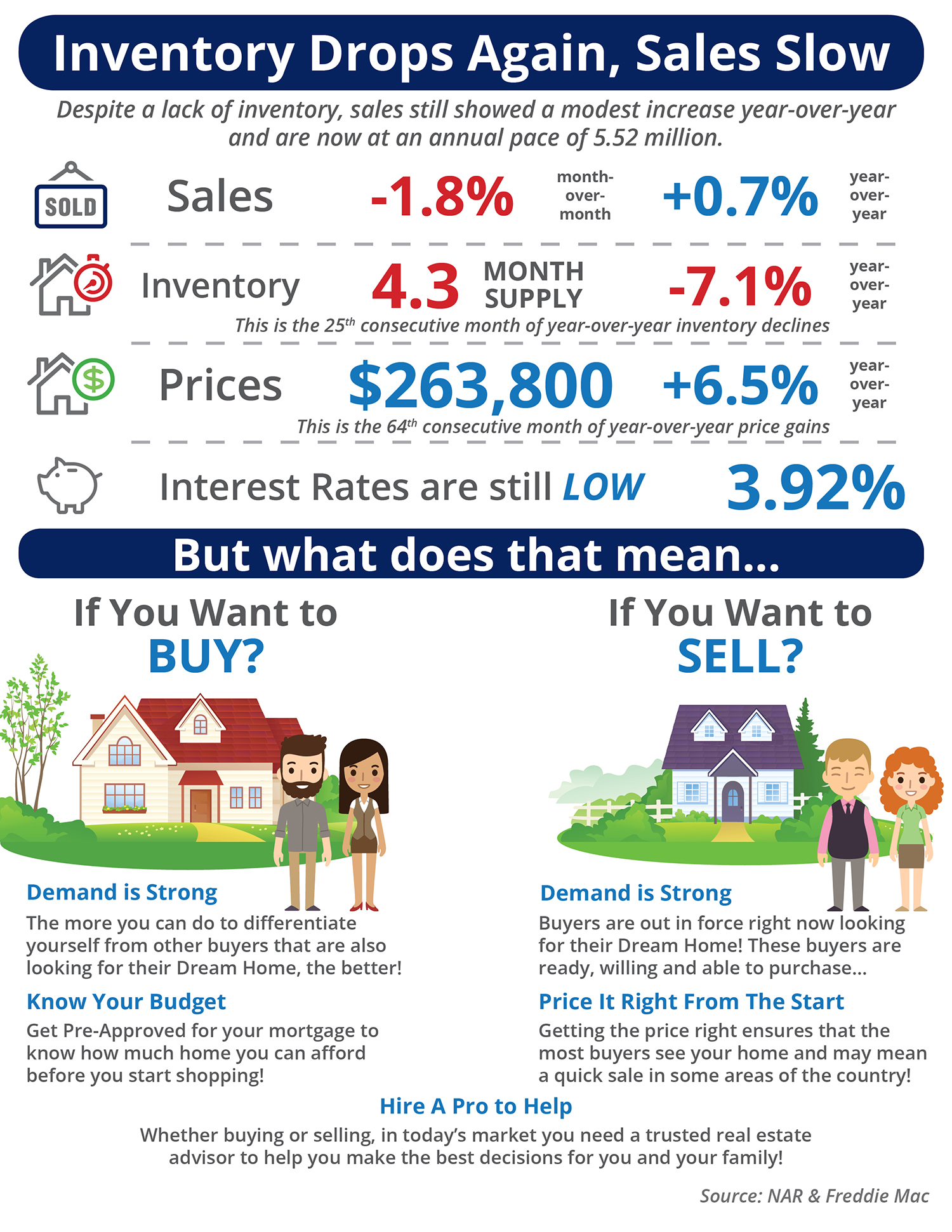

![Inventory Drops Again, Sales Slow [INFOGRAPHIC] | Simplifying The Market](http://d39ah2zlibpm3g.cloudfront.net/wp-content/uploads/2017/07/27114549/20170728-Share-STM.jpg)

Posted in For Buyers, For Sellers, Infographics

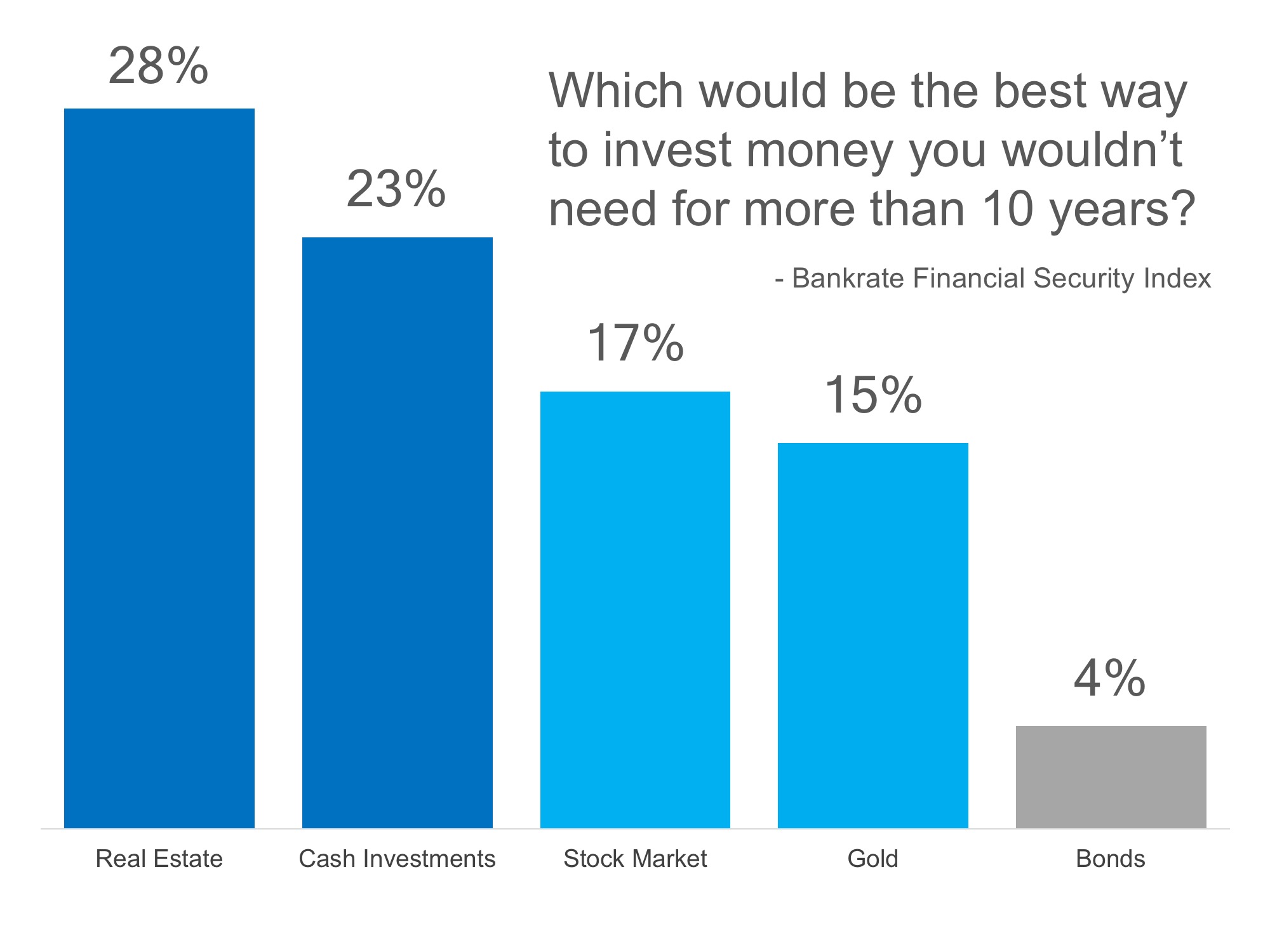

According to Bankrate’s latest Financial Security Index Poll, Americans who have money to set aside for the next 10 years would rather invest in real estate than any other type of investment.

Bankrate asked Americans to answer the following question:

“What is the best way to invest money you wouldn’t need for 10 years or more?”

Real Estate came in as the top choice with 28% of all respondents (3% higher than last year), while cash investments – such as savings accounts and CD’s – came in second with 23% (the same as last year). The chart below shows the full results:

The article points out several reasons for these results:

“After bottoming out at the end of 2011 following the worst housing collapse in generations, home prices have gone gangbusters recently, climbing back above their record pre-crisis levels. Prices jumped 6.6 percent during the 12 months that ended in May, according to CoreLogic.

Toss in persistently low interest rates, tax goodies that come with owning a mortgage, and the psychological payoff from planting your roots, and maybe it’s no wonder real estate remains popular.”

The article also revealed that:

“Bankrate’s Financial Security Index — based on survey questions about how people feel about their debt, savings, net worth, job security and overall financial situation — has hit its third-highest level since the poll’s inception in December 2010.”

We have often written about the financial and non-financial reasons homeownership makes sense. It is nice to see that Americans still believe in homeownership as the best investment.

Posted in First Time Home Buyers, For Buyers, Move-Up Buyers

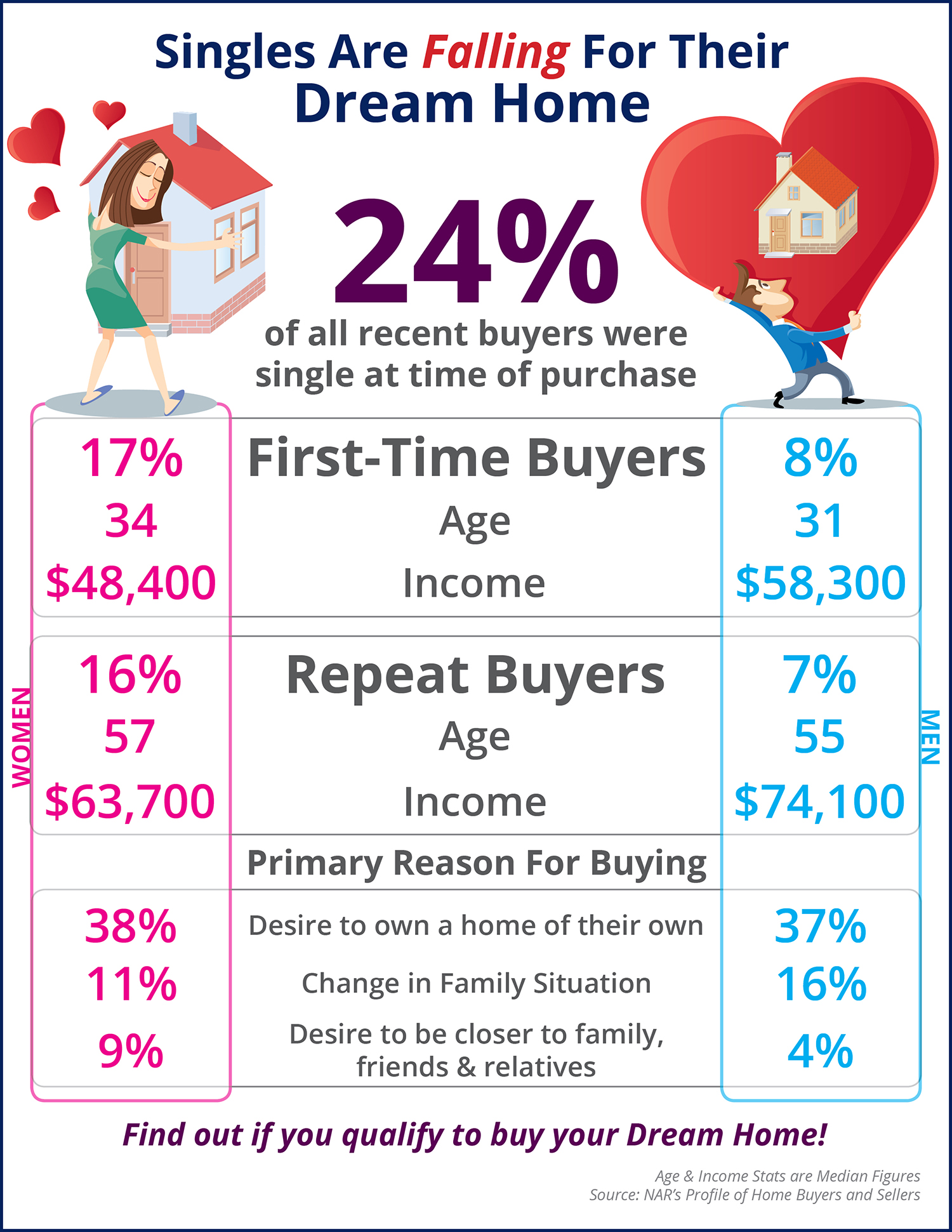

![Singles Are Falling for Their Dream Home First [INFOGRAPHIC] | Simplifying The Market](http://d39ah2zlibpm3g.cloudfront.net/wp-content/uploads/2017/06/26165916/20170721-Share-STM.jpg)

Posted in First Time Home Buyers, For Buyers, Infographics

According to the National Association of Realtors®’ 2017 National Housing Pulse Survey, 84% of Americans now believe that purchasing a home is a good financial decision. This is the highest percentage since 2007 – before the housing crisis. Those surveyed pointed out five major reasons why they believe homeownership is a good financial decision:

The survey also revealed that the majority of Americans strongly agree that homeownership helps create safe, secure, and stable environments.

Homeownership has always been and still is a crucial part of the American Dream.

Posted in First Time Home Buyers, For Buyers, Move-Up Buyers

In today’s highly competitive real estate market, where inventory levels are not keeping up with the constant stream of buyer demand, there are steps you can take to ensure you are most prepared for success when buying a home.

The 3 tips we are going to expand on today come from a recent blog by Trulia entitled, The Skinny on Skinny Inventory.

“Homebuyers should talk with a lender, real estate agent, and a home inspector BEFORE finding a home to make an offer on.”

Being intentional, pre-approved, and prepared will set you up for the accelerated time tables that come with a highly competitive market. If you are the most prepared buyer interested in a home, if you have already secured financial approval, and if you are ready to move fast, your bid will be that much more attractive to a seller.

“Starter homebuyers don’t have a home to sell and can be flexible on closing dates compared to homebuyers who are also trying to sell at the same time.”

If you are one of the many first-time buyers looking for your dream home, know that being strategic and flexible about closing dates can also help your offer stand out from the rest. But don’t fret if you are a homeowner who will also have to sell your own house first – be upfront about your timeline with your agent and with any offers you make.

“Buyers might consider looking for homes that have been on the market for a while and investigate why. The reasons may be a deal-killer but all it takes is one ugly duckling to turn into a swan.”

Finding a fixer-upper or a home that needs a little love might be your best way to guarantee that you are able to find a home in the neighborhood that you want. The worst house on the best block will go for a steal and offer instant equity once you fix it up!

In today’s market, full of bidding wars and tough competition, finding ways to stand out from the rest by getting creative will improve your chances of having a home to call your own.

Posted in First Time Home Buyers, For Buyers, For Sellers, Move-Up Buyers

For your home value estimate, enter the access code you received on the postcard, just click here: