Instant Home Estimate

For your home value estimate, enter the access code you received on the postcard, just click here:

According to Freddie Mac’s latest Primary Mortgage Market Survey, interest rates for a 30-year fixed rate mortgage are currently at 3.96%, which is still near record lows in comparison to recent history!

The interest rate you secure when buying a home not only greatly impacts your monthly housing costs, but also impacts your purchasing power.

Purchasing power, simply put, is the amount of home you can afford to buy for the budget you have available to spend. As rates increase, the price of the house you can afford will decrease if you plan to stay within a certain monthly housing budget.

The chart below shows what impact rising interest rates would have if you planned to purchase a home within the national median price range, and planned to keep your principal and interest payments between $1,850-$1,900 a month.

With each quarter of a percent increase in interest rate, the value of the home you can afford decreases by 2.5% (in this example, $10,000). Experts predict that mortgage rates will be closer to 5% by this time next year.

Posted in First Time Home Buyers, For Buyers, Interest Rates, Move-Up Buyers

Posted in For Buyers, For Sellers, Infographics

Interest rates have hovered around 4% for the majority of 2017, which has given many buyers relief from rising home prices and has helped with affordability. Experts predict that rates will increase by the end of 2017 and will be about three-quarters of a percentage point higher, at 4.5%, by the end of 2018.

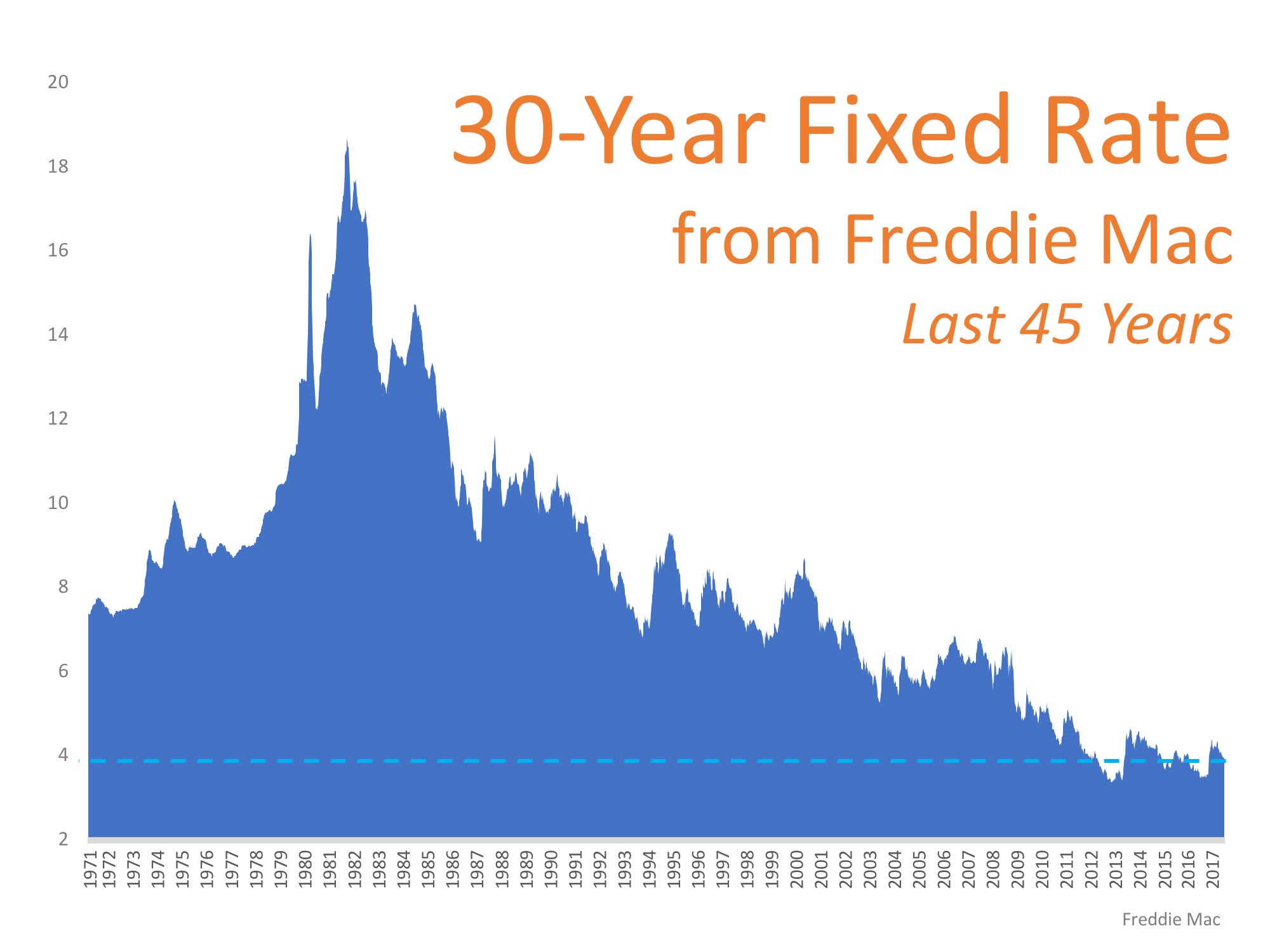

Last week’s Freddie Mac Primary Mortgage Market Survey revealed that interest rates for a 30-year fixed rate mortgage have fallen to their lowest mark this year, at 3.88%. This is great news for homebuyers looking to purchase and homeowners looking to refinance.

The rate you secure greatly impacts your monthly mortgage payment and the amount you will ultimately pay for your home.

Let’s take a look at a historical view of interest rates over the last 45 years.

Be thankful that you can still get a better interest rate than your older brother or sister did ten years ago, a lower rate than your parents did twenty years ago, and a better rate than your grandparents did forty years ago.

Posted in First Time Home Buyers, For Buyers, Interest Rates, Move-Up Buyers

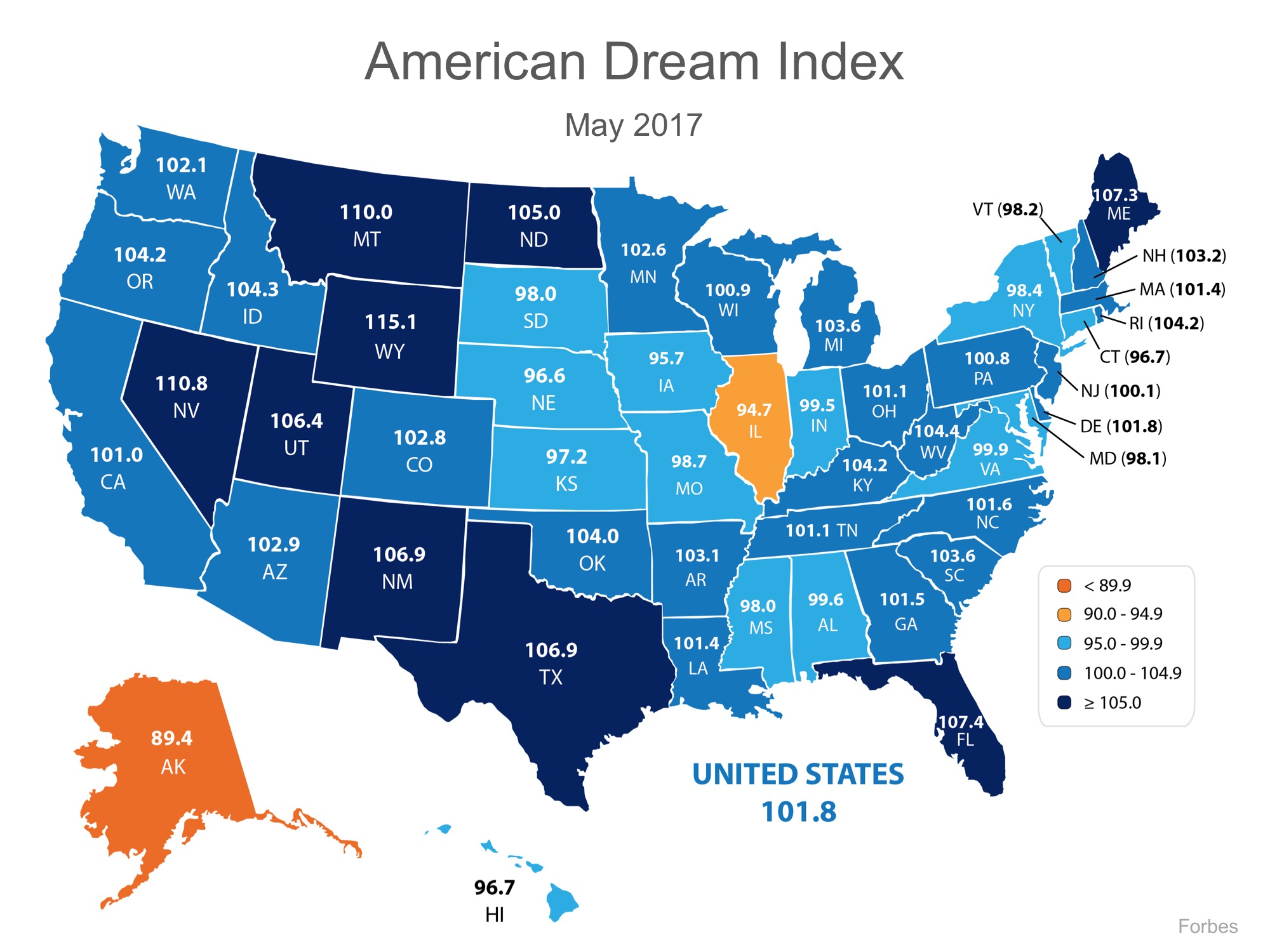

Forbes.com recently released the latest results of their American Dream Index, in which they measure “the prosperity of the middle class, and…examine which states best support the American Dream.”

The monthly index measures several different economic factors, including goods-producing employment, personal and commercial bankruptcies, building permits, startup activity, unemployment insurance claims, labor force participation, and layoffs.

The national index score was rounded out to 100.0 in January as a baseline for comparison and it rose the fourth straight month in a row to 101.8.

Alaska, coming in at 89.4, represented the lowest score on the index due in part to the recent collapse in oil prices. In contrast, Wyoming came in with the highest score at 115.1. The full results can be seen in the map below.

Forbes Senior Editor Kurt Badenhausen explained why many states saw a boost in the index last month:

“The American Dream Index rose for the fourth straight month to 101.8 propelled by gains in goods-producing jobs and building permits, as well as declines in unemployment claims and mass layoffs.

Goods-producing jobs (manufacturing, mining, construction and agriculture) were up for the ninth straight month in May…Building permits rose for the fourth straight month compared to the prior year.”

The American Dream, for many, includes being able to own a home of one’s own. With the economy improving in many areas of the country, that dream can finally become a reality.

Posted in First Time Home Buyers, For Buyers, Move-Up Buyers

Posted in For Buyers, For Sellers, Housing Market Updates, Infographics

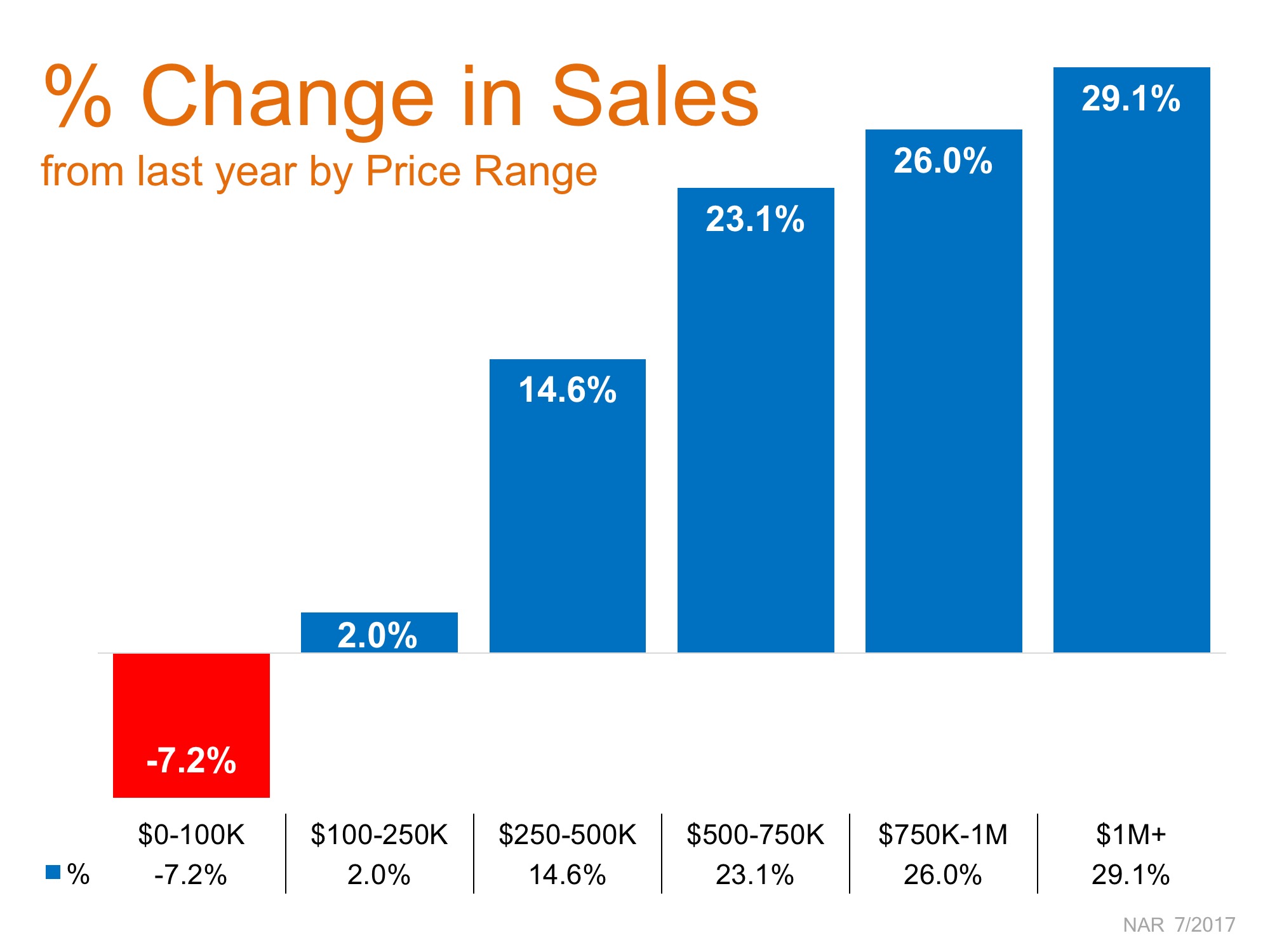

We previously reported how a shortage of inventory in the starter and trade-up home markets is driving prices up and causing bidding wars, creating a true seller’s market. At the same time, in the premium home market, an over-abundance of inventory has started to see prices come down and put buyers in the driver’s seat, creating the beginning of a buyer’s market.

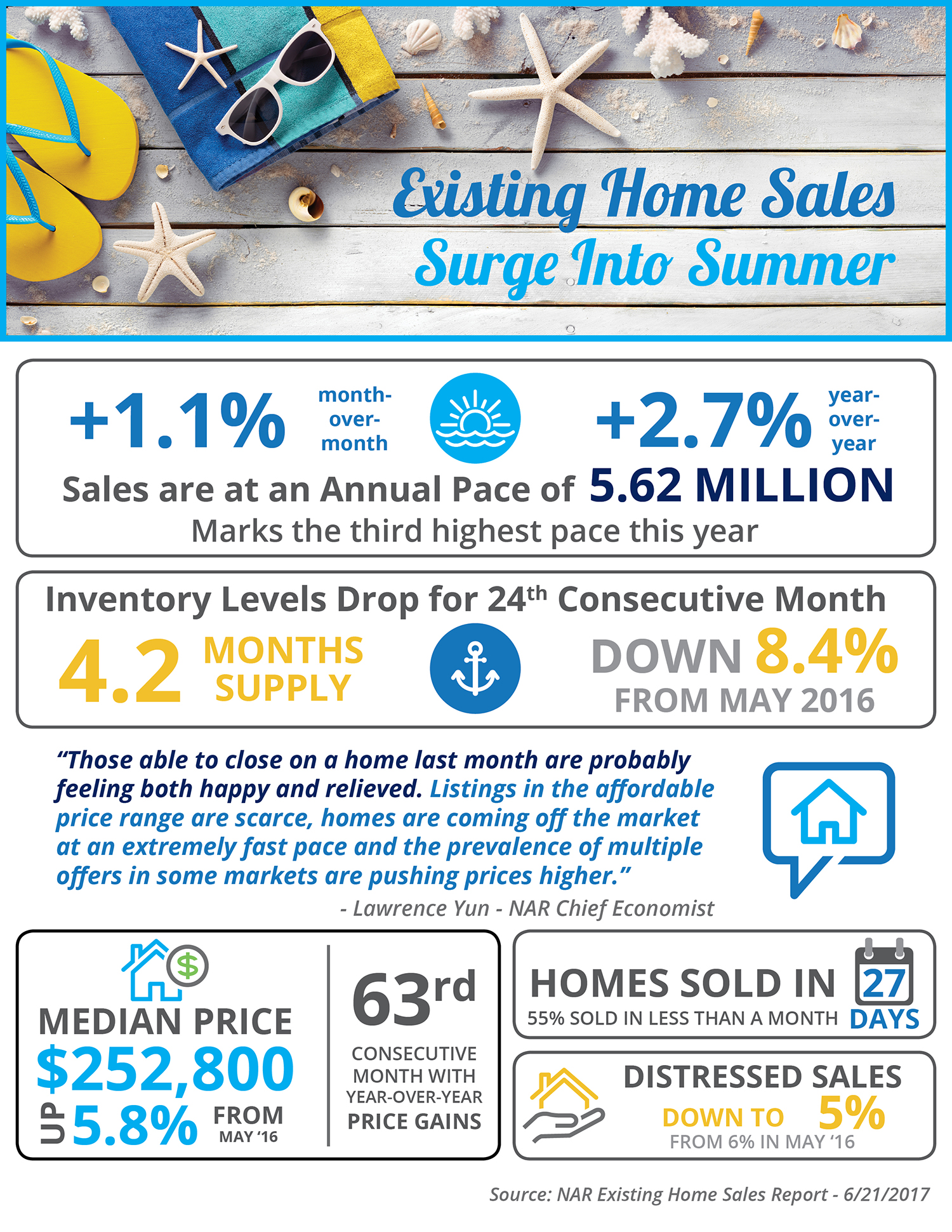

Last week, the National Association of Realtors released their Existing Home Sales Report which shed some additional light on the impact of inventory levels on sales in each price range.

The chart below shows the year-over-year difference in sales at each price range.

The under $100K range has shown declines in recent years due to the shortage of distressed homes available for sale (just 5% of sales this past month, compared to 35% in January 2012). Sales in the next two price ranges are no doubt being hindered by low inventory as buyers compete for the same home.

NAR’s Chief Economist, Lawrence Yun, explained:

“Those able to close on a home last month are probably feeling both happy and relieved. Listings in the affordable price range are scarce, homes are coming off the market at an extremely fast pace and the prevalence of multiple offers in some markets are pushing prices higher.”

The biggest surprise? This is the first time in years where the $1M and up price range had the highest jump in sales when compared to last year and to all other price ranges (29.1%)! The two price ranges right underneath the $1M range were a close second and third. As the price went up, so did the sales!

With additional inventory available in the higher price ranges, and the economy improving, many luxury buyers are finding it easier to find their dream homes. Yun commented,

“The job market in most of the country is healthy and the recent downward trend in mortgage rates continues to keep buyer interest at a robust level.”

If you are one of the many homeowners who is looking to sell your starter or trade up home and move up to a luxury home, now is the time!

Posted in First Time Home Buyers, For Buyers, For Sellers, Move-Up Buyers

In many markets across the country, the number of buyers searching for their dream homes greatly outnumbers the amount of homes for sale. This has led to a competitive marketplace where buyers often need to stand out. One way to show you are serious about buying your dream home is to get pre-qualified or pre-approved for a mortgage before starting your search.

Even if you are in a market that is not as competitive, knowing your budget will give you the confidence of knowing if your dream home is within your reach.

Freddie Mac lays out the advantages of pre-approval in the My Home section of their website:

“It’s highly recommended that you work with your lender to get pre-approved before you begin house hunting. Pre-approval will tell you how much home you can afford and can help you move faster, and with greater confidence, in competitive markets.”

One of the many advantages of working with a local real estate professional is that many have relationships with lenders who will be able to help you with this process. Once you have selected a lender, you will need to fill out their loan application and provide them with important information regarding “your credit, debt, work history, down payment and residential history.”

Freddie Mac describes the 4 Cs that help determine the amount you will be qualified to borrow:

Getting pre-approved is one of many steps that will show home sellers that you are serious about buying, and it often helps speed up the process once your offer has been accepted.

Many potential home buyers overestimate the down payment and credit scores needed to qualify for a mortgage today. If you are ready and willing to buy, you may be pleasantly surprised at your ability to do so as well.

Posted in First Time Home Buyers, For Buyers, Move-Up Buyers

In Realtor.com’s recent article, “Home Buyers’ Top Mortgage Fears: Which One Scares You?” they mention that “46% of potential home buyers fear they won’t qualify for a mortgage to the point that they don’t even try.”

Buyers overestimate the down payment funds needed to qualify for a home loan. According to the First Quarter 2017 Homeownership Program Index (HPI) from Down Payment Resource, saving for a down payment was the barrier that kept 70% of renters from buying.

Rob Chrane, CEO of Down Payment Resource had this to say,

“There are many mortgage-ready renters today, but they don’t know it. Often, homebuyers remain sidelined for years due to the down payment.”

Many believe that they need at least 20% down to buy their dream home, but programs are available that allow buyers put down as little as 3%. Many renters may actually be able to enter the housing market sooner than they ever imagined with new programs that have emerged allowing less cash out of pocket.

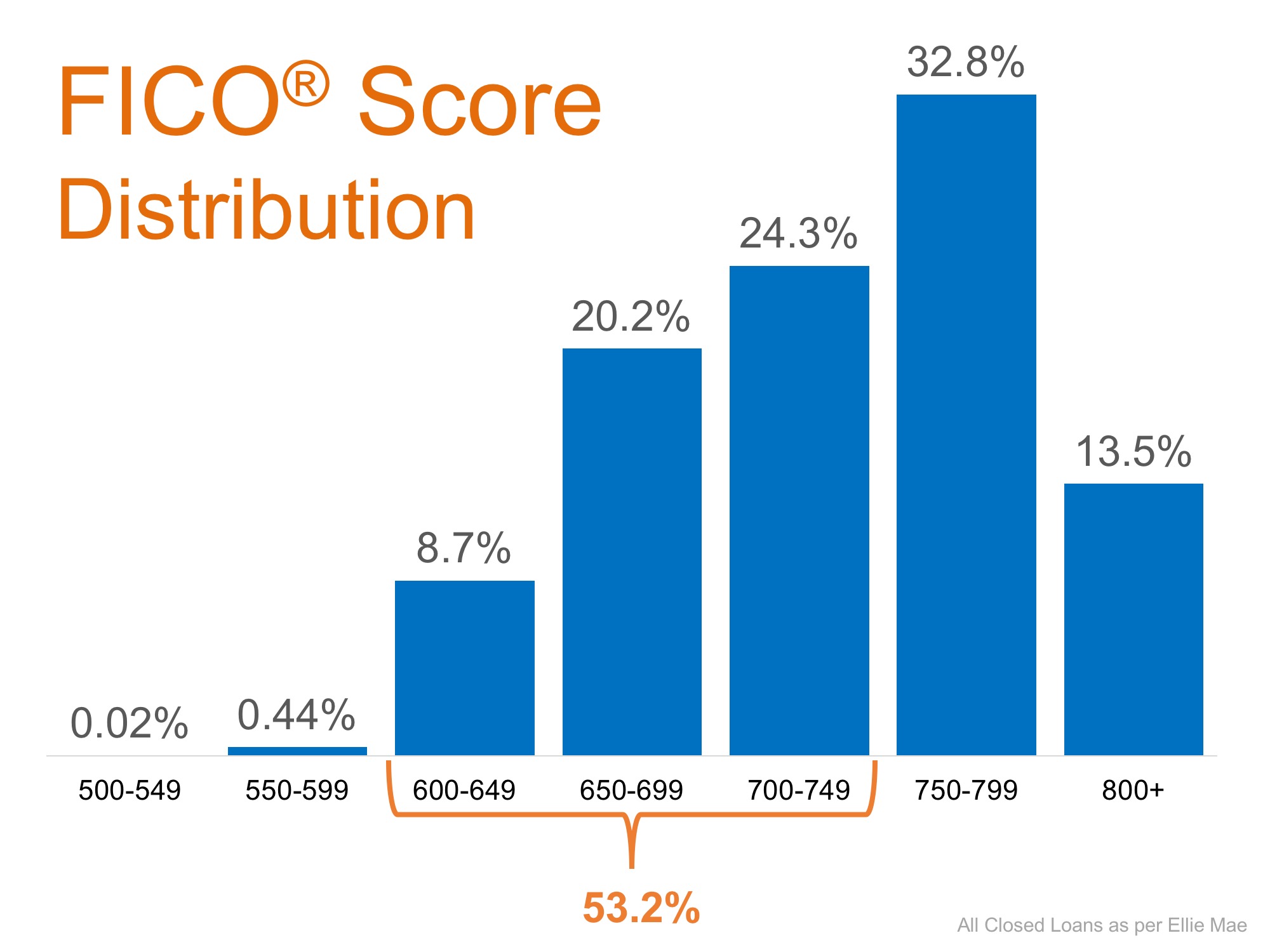

The survey revealed that 59% of Americans either don’t know (54%) or are misinformed (5%) about what FICO® score is necessary to qualify.

Many Americans believe a ‘good’ credit score is 780 or higher.

To help debunk this myth, let’s take a look at Ellie Mae’s latest Origination Insight Report, which focuses on recently closed (approved) loans.

As you can see in the chart above, 53.2% of approved mortgages had a credit score of 600-749.

Whether buying your first home or moving up to your dream home, knowing your options will make the mortgage process easier. Your dream home may already be within your reach.

Posted in Down Payments, First Time Home Buyers, For Buyers, Move-Up Buyers

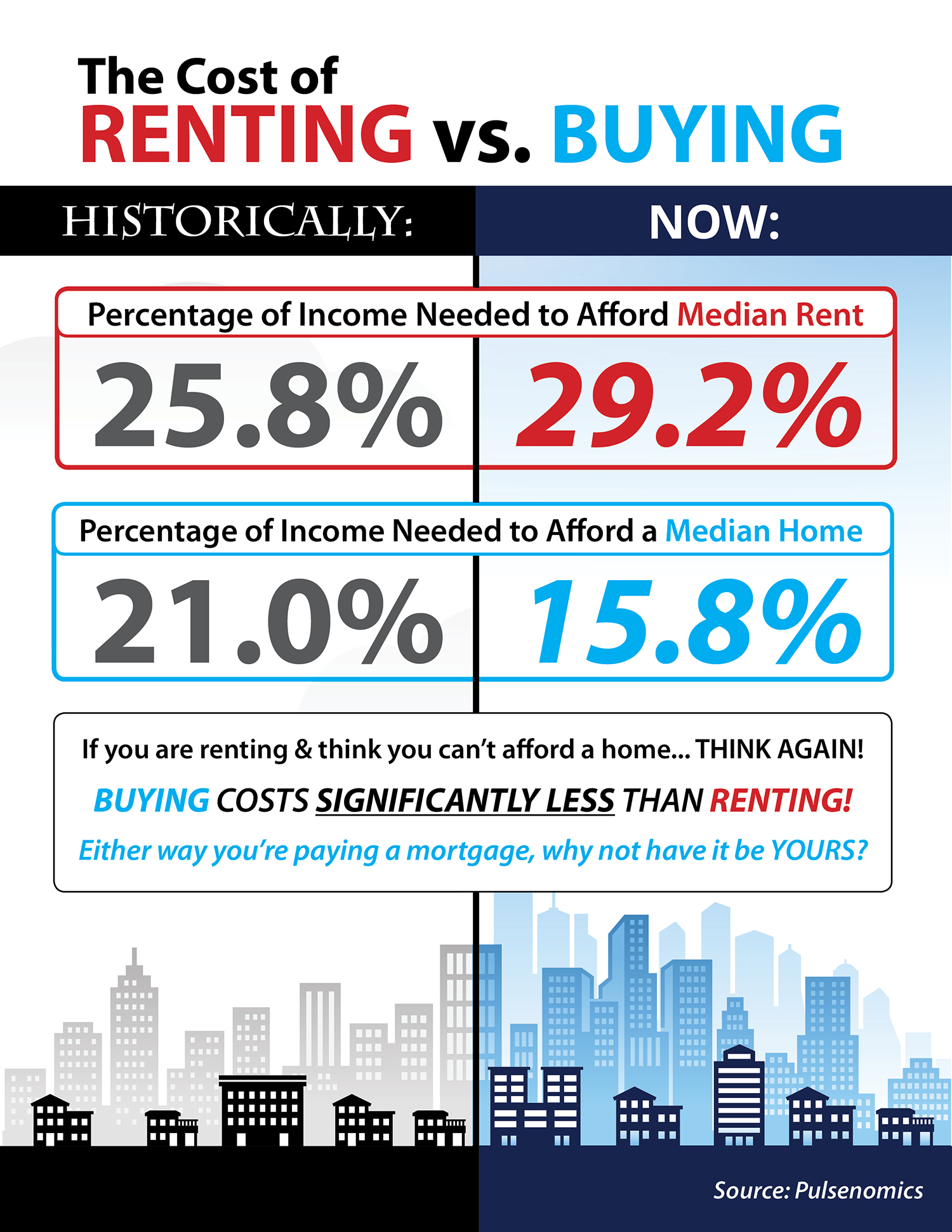

![The Cost of Renting vs. Buying in the US [INFOGRAPHIC] | Simplifying The Market](http://d39ah2zlibpm3g.cloudfront.net/wp-content/uploads/2017/06/20140325/20170623-Share-STM.jpg)

Posted in First Time Home Buyers, For Buyers, Infographics

We often discuss the difference in family wealth between homeowner households and renter households. Much of that difference is the result of the equity buildup that homeowners experience over the time that they own their home. In a report recently released by the nonpartisan Employee Benefit Research Institute (EBRI), they reveal how valuable equity can be in retirement planning.

Craig Copeland, Senior Research Associate at EBRI, recently authored a report, Importance of Individual Account Retirement Plans and Home Equity in Family Total Wealth, in which he reveals:

“Individual account retirement plan assets, plus home equity, represent almost all of what families have to use for retirement expenses outside of Social Security and traditional pensions. Those families without individual account assets typically have very low overall assets, so they have almost nothing to draw from for retirement expenses.”

The report echoed the findings of a working paper, Home Equity Patterns among Older American Households, authored by Barbara Butrica and Stipica Mudrazija of Urban Institute. Fannie Mae highlighted these findings for their blog The Home Story this past winter, quoting Butrica and Mudrazija:

“For most adults near traditional retirement age, a home is their most valuable asset — dwarfing retirement accounts, other financial assets, and other nonfinancial assets. Although relatively few retirees tap into their home equity, having it provides financial security… In fact, many retirement security experts argue that the conventional three-legged stool of retirement resources — Social Security, pensions, and savings — is incomplete because it ignores the home.”

USAToday interviewed two area experts to comment on the EBRI report. Randy Bruns, a private wealth adviser with HighPoint Planning Partners, agreed with the findings:

“Social Security and home equity are major pieces of the retirement puzzle.”

Wade Pfau, Professor of Retirement Income at The American College of Financial Services and author of “Reverse Mortgages: How to use Reverse Mortgages to Secure Your Retirement,” said having the equity without a plan to use it won’t help:

“Home equity is a very important asset for American retirees, and so it is important to think about how to make best use of home equity in retirement planning.”

Whether you use the equity in your home through a reverse mortgage or by selling and downsizing to a less expensive home, it should be a crucial piece of your retirement planning.

Posted in For Buyers, For Sellers

For your home value estimate, enter the access code you received on the postcard, just click here: