Instant Home Estimate

For your home value estimate, enter the access code you received on the postcard, just click here:

The media has extensively covered the rise in mortgage interest rates since last fall (from 3.42% last September to the current 4.1% according to Freddie Mac). However, a less covered aspect of the mortgage market is that requirements to get a mortgage have eased while rates have risen.

The Mortgage Bankers Association (MBA) quantifies the availability of mortgage credit each month with their Mortgage Credit Availability Index (MCAI). According to the MBA, the MCAI is:

“A summary measure which indicates the availability of mortgage credit at a point in time.”

The higher the index, the easier it is to get a mortgage. Here is a chart showing the MCAI over the last several months as rates have increased.

Yes. Here are two examples:

Whether you are a current homeowner looking to move to a home that will better serve your family’s current needs, or a first-time buyer looking for a starter home, it is easier to get a mortgage today than it has been at any other time in the last ten years.

Posted in Down Payments, First Time Home Buyers, For Buyers, Interest Rates, Move-Up Buyers

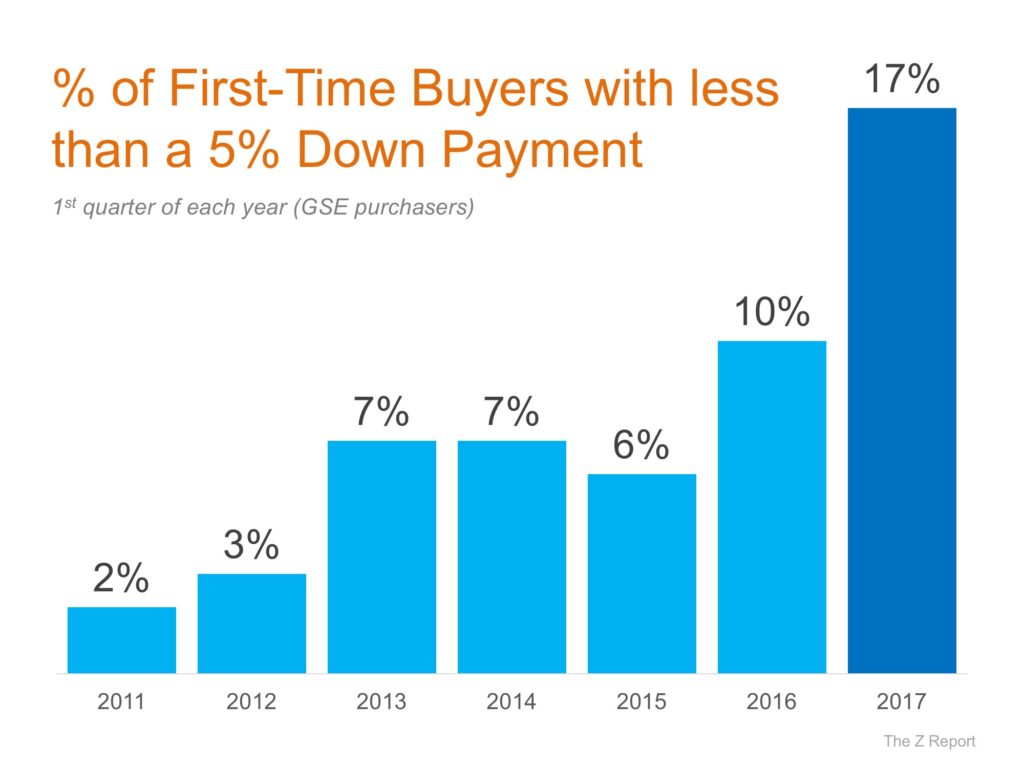

A recent report released by Down Payment Resource shows that 65% of first-time homebuyers purchased their homes with a down payment of 6% or less in the month of January.

The trend continued through all buyers with a mortgage, as 62% made a down payment of less than 20%, which is consistent with findings from December.

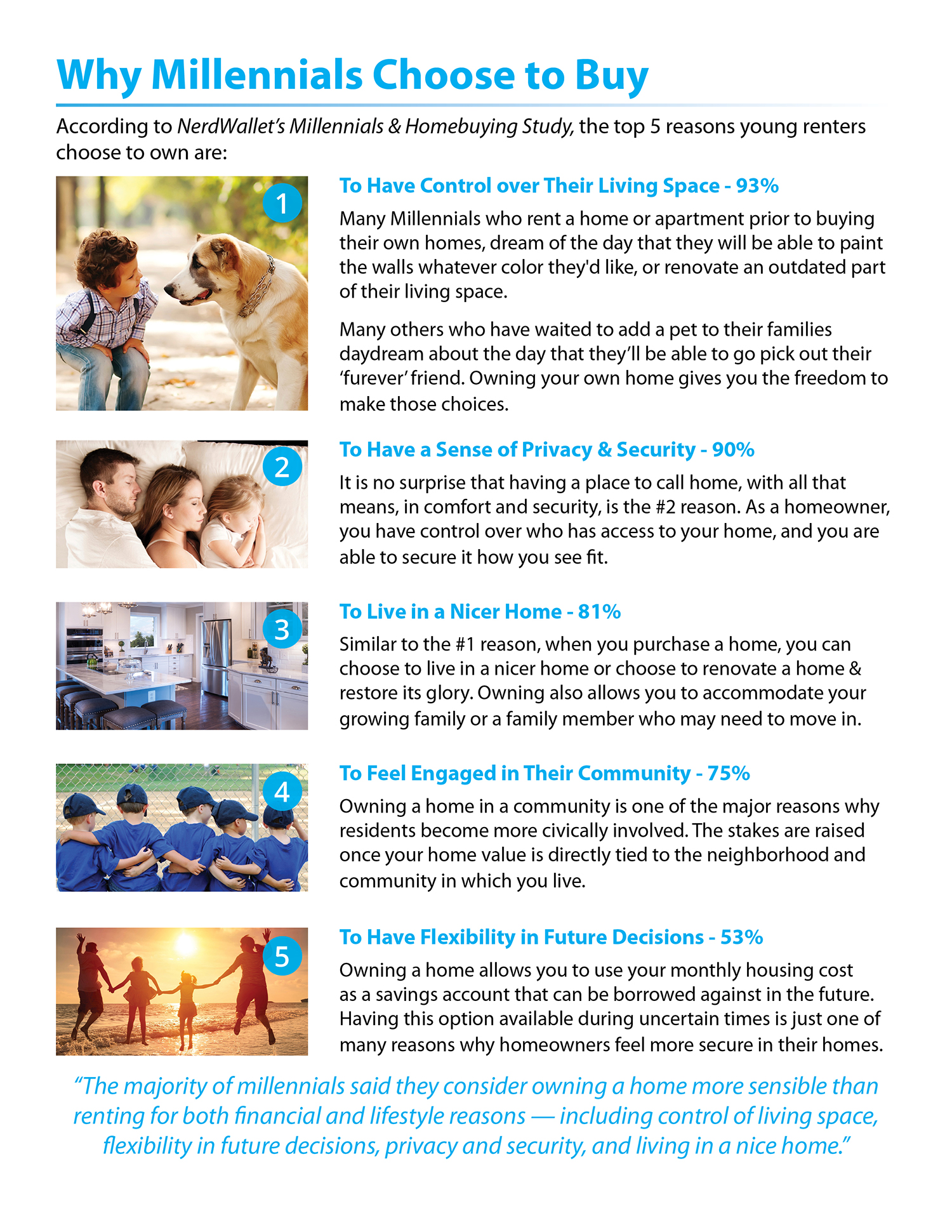

An article by DS News points to the new wave of millennial homebuyers:

“It seems that the long-awaited influx of millennial home buyers is beginning. Ellie Mae reported that mortgages to millennial borrowers for new home purchases continued their ascent in January, accounting for 84 percent of closed loans.”

Among millennials who purchased homes in January, FHA loans remained popular, making up 35% of all loans closed. Ellie Mae’s Executive Vice President of Corporate Strategy Joe Tyrrell gave some insight into why:

“It is not surprising to see Millennial borrowers leverage FHA loans because they typically offer lower down payments and lower average FICO score requirements than conventional loans. Across the board, we’re continuing to see strong interest in homeownership from this younger generation.”

If you are one of the many millennials who is debating a home purchase this year, let’s get together to help you understand your options and set you on the path to preapproval.

Posted in Down Payments, First Time Home Buyers, For Buyers, Millennials, Move-Up Buyers

There are many benefits to homeownership. One of the top benefits is being able to protect yourself from rising rents by locking in your housing cost for the life of your mortgage.

Jonathan Smoke, Chief Economist at realtor.com, reported on what he calls a “Rental Affordability Crisis.” He warns that,

“Low rental vacancies and a lack of new rental construction are pushing up rents, and we expect that they’ll outpace home price appreciation in the year ahead.”

In the Joint Center for Housing Studies at Harvard University’s 2016 State of the Nation’s Housing Report, they revealed that “The number of cost-burdened households rose to 21.3 million. Even more troubling, the number with severe burdens (paying more than 50% of income for housing) jumped to a record 11.4 million.” These households struggle to save for a rainy day and pay other bills, such as food and healthcare.

In Smoke’s article, he went on to say,

“Housing is central to the health and well-being of our country and our local communities. In addition, this (rental affordability) crisis threatens the future value of owned housing, as the burdensome level of rents will trap more aspiring owners into a vicious financial cycle in which they cannot save and build a solid credit record to eventually buy a home.”

“While more than 85% of markets have burdensome rents today, it’s perplexing that in more than 75% of the counties across the country, it is actually cheaper to buy than rent a home. So why aren’t those unhappy renters choosing to buy?”

Perhaps you have already saved enough to buy your first home. HousingWire reported that analysts at Nomura believe:

“It’s not that Millennials and other potential homebuyers aren’t qualified in terms of their credit scores or in how much they have saved for their down payment.

It’s that they think they’re not qualified or they think that they don’t have a big enough down payment.” (emphasis added)

Many first-time homebuyers who believe that they need a large down payment may be holding themselves back from their dream home. As we have reported before, in many areas of the country, a first-time home buyer can save for a 3% down payment in less than two years. You may have already saved enough!

Don’t get caught in the trap so many renters are currently in. If you are ready and willing to buy a home, find out if you are able. Let’s get together to determine if you can qualify for a mortgage now!

Posted in First Time Home Buyers, For Buyers, Move-Up Buyers

Posted in First Time Home Buyers, For Buyers, Infographics, Millennials, Move-Up Buyers

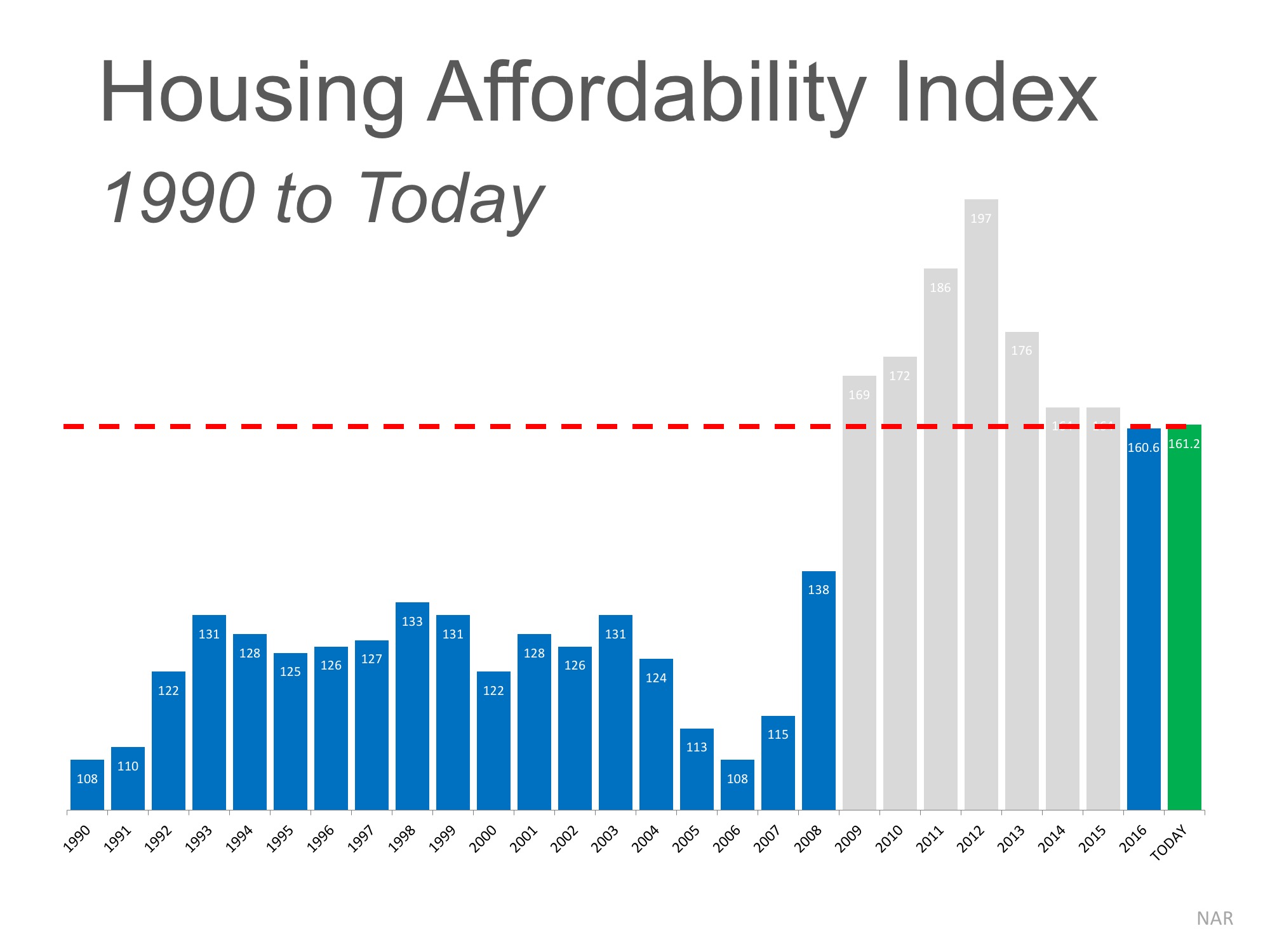

Some industry experts are claiming that the housing market may be headed for a slowdown as we proceed through 2017, based on rising home prices and a potential jump in mortgage interest rates. One of the data points they use is the Housing Affordability Index, as reported by the National Association of Realtors (NAR).

Here is how NAR defines the index:

“The Housing Affordability Index measures whether or not a typical family earns enough income to qualify for a mortgage loan on a typical home at the national level based on the most recent price and income data.”

Basically, a value of 100 means a family earning the median income earns enough to qualify for a mortgage on a median-priced home, based on the price and mortgage interest rates at the time. Anything above 100 means the family has more than enough to qualify.

The higher the index, the easier it is to afford a home.

The index has been declining over the last several years as home values increased. Some are concerned that too many buyers could be priced out of the market.

But, wait a minute…

Though the index skyrocketed from 2009 through 2013, we must realize that during that time, the housing crisis left the market with an overabundance of distressed properties (foreclosures and short sales). All prices dropped dramatically and distressed properties sold at major discounts. Then, mortgage rates fell like a rock.

The market is recovering, and values are coming back nicely. That has caused the index to fall.

However, let’s remove the crisis years (shaded in gray) and look at the current index as compared to the index from 1990 – 2008:

Though prices and rates appear to be increasing, we must realize that affordability is composed of three ingredients: home prices, interest rates, and income. And, incomes are finally rising.

ATTOM Data Solutions recently released their Q1 2017 U.S. Home Affordability Index. The report explained:

“Stronger wage growth is the silver lining in this report, outpacing home price growth in more than half of the markets for the first time since Q1 2012, when median home prices were still falling nationwide. If that pattern continues, it will help turn the tide in the eroding home affordability trend.”

Compared to historic norms, it is still a great time to buy from an affordability standpoint.

Posted in First Time Home Buyers, For Buyers, Move-Up Buyers

Traditionally, spring is the busiest season for real estate. Buyers come out in force and homeowners list their houses for sale hoping to capitalize on buyer activity. This year will be no different!

Buyers have already been out in force looking for their dream homes and more are on their way, but the challenge is that the inventory of homes for sale has not kept up with demand, which has lead to A LOT of competition for the homes that are available.

A recent Bloomberg article touched on the current market conditions:

“It’s the 2017 U.S. spring home-selling season, and listings are scarcer than they’ve ever been. Bidding wars common in perennially hot markets like the San Francisco Bay area, Denver and Boston are now also prevalent in the once slow-and-steady heartland, sending prices higher and sparking desperation among buyers across the country.”

Sam Khater, Deputy Chief Economist at CoreLogic went on to explain why buyers are flocking to the market in big numbers:

“In today’s market, many buyers think the trough in [interest] rates is over. If you don’t get in now, it’s just going to be worse later. Rates will be higher, prices will be higher, and maybe inventory selection will be lower.”

In some markets, “thirty-five percent of properties are selling within the first week or two of hitting the market.” Homes are selling at a rapid clip in places like:

Let’s get together to discuss your exact market conditions and help you create a strategy to secure your new home in this competitive atmosphere!

Posted in First Time Home Buyers, For Buyers, For Sellers, Housing Market Updates, Move-Up Buyers

A survey by Ipsos found that the American public is still somewhat confused about what is required to qualify for a home mortgage loan in today’s housing market. There are two major misconceptions that we want to address today.

The survey revealed that consumers overestimate the down payment funds needed to qualify for a home loan. According to the report, 40% of consumers think a 20% down payment is always required. In actuality, there are many loans written with a down payment of 3% or less.

Many renters may actually be able to enter the housing market sooner than they ever imagined with new programs that have emerged allowing less cash out of pocket.

The survey also revealed that 62% of respondents believe they need excellent credit to buy a home, with 43% thinking a “good credit score” is over 780. In actuality, the average FICO® scores of approved conventional and FHA mortgages are much lower.

The average conventional loan closed in February had a credit score of 752, while FHA mortgages closed with a score of 686. The average across all loans closed in February was 720. The chart below shows the distribution of FICO® Scores for all loans approved in February.

If you are a prospective buyer who is ‘ready’ and ‘willing’ to act now, but are not sure if you are ‘able’ to, let’s sit down to help you understand your true options.

Posted in Down Payments, First Time Home Buyers, For Buyers, Move-Up Buyers

Posted in First Time Home Buyers, For Buyers, For Sellers, Infographics, Move-Up Buyers, Pricing

The success of the housing market is strongly tied to the consumer’s confidence in the overall economy. For that reason, we believe 2017 will be a great year for real estate. Here is just a touch of the news coverage on the subject.

“Consumers’ faith in the housing market is stronger than it’s ever been before, according to a newly released survey from Fannie Mae.”

“Americans’ confidence continued to mount last week as the Bloomberg Consumer Comfort Index reached the highest point in a decade on more-upbeat assessments about the economy and buying climate.”

“Confidence continues to rise among America’s consumers…the latest consumer sentiment numbers from the University of Michigan showed that in March confidence rose again.”

“U.S. consumers are the most confident in the U.S. economy in 15 years, buoyed by the strongest job market since before the Great Recession. The survey of consumer confidence rose…according to the Conference Board, the private company that publishes the index. That’s the highest level since July 2001.”

“The results were incredibly strong and…offer one of the most positive consumer takes on housing since the recovery started.”

Posted in For Buyers, For Sellers, Housing Market Updates

If your house no longer fits your needs and you are planning on buying a luxury home, now is a great time to do so! We recently shared data from Trulia’s Market Mismatch Study which showed that in today’s premium home market, buyers are in control.

The inventory of homes for sale in the luxury market far exceeds those searching to purchase these properties in many areas of the country. This means that homes are often staying on the market longer, or can be found at a discount.

Those who have a starter or trade-up home to sell will find buyers competing, and often entering bidding wars, to be able to call your house their new home.

The sale of your starter or trade-up house will aid in coming up with a larger down payment for your new luxury home. Even a 5% down payment on a million-dollar home is $50,000.

But not all who are buying luxury properties have a home to sell first.

In a recent Washington post article, Daryl Judy, an associate broker with Washington Fine Properties, gave some insight into what many millennials are choosing to do:

“Some high-earning millennials save money until they are in their early 30s to buy a place and just skip over that starter-home phase. They’ll stay in an apartment until they can afford to pay for the place they want.”

The best time to sell anything is when demand is high and supply is low. If you are currently in a starter or trade-up house that no longer fits your needs, and are looking to step into a luxury home… Now’s the time to list your house for sale and make your dreams come true.

Posted in First Time Home Buyers, For Buyers, Millennials, Move-Up Buyers

For your home value estimate, enter the access code you received on the postcard, just click here: