Instant Home Estimate

For your home value estimate, enter the access code you received on the postcard, just click here:

As home values continue to increase at levels greater than historic norms, some are concerned that we are heading for another crash like the one we experienced ten years ago. We recently explained that the lenient lending standards of the previous decade (which created false demand) no longer exist. But what about prices?

Are prices appreciating at the same rate that they were prior to the crash of 2006-2008? Let’s look at the numbers as reported by Freddie Mac:

We must also realize that, to a degree, the current run-up in prices is the market trying to catch up after a crash that dramatically dropped prices for five years.

Prices are appreciating at levels greater than historic norms. However, we are not at the levels that led to the housing bubble and bust.

Posted in For Buyers, For Sellers, Housing Market Updates, Pricing

The National Association of Realtors (NAR) recently released their 2017 Profile of Home Buyers and Sellers in which they surveyed recent home buyers and sellers about their experiences. An entire section of the profile is dedicated to buyers’ experiences with their real estate agents.

If you are looking to buy in 2018, here are the top 5 benefits of using a real estate agent when buying your dream home as cited by recent buyers:

If you are new to the home buying process, an experienced real estate professional can explain exactly what to expect during the entire transaction so you aren’t caught off guard.

Whether it’s pointing out possible uses for an extra bedroom/office, or using their trained eye to see potentially disastrous hazards that may be hiding out of site, your agent is there to protect your interests and make sure your home buying experience is a good one.

When it comes to negotiating the complex terms of your contract and coming to an agreement with the seller, it never hurts to have someone who has been there before on your side. If earlier in your search you found a couple of less than desirable features on the home you are going to purchase, your agent can make sure that contingencies are in place for you to pay the best price. Their analysis of comparable properties in the area will also help to make sure that your dream home is priced properly for the market.

Real estate agents are titans of networking. Many have a list of preferred providers who they have worked with in the past and who they trust to work as a part of your team to make your dream come true. This can include mortgage professionals (listed as the #8 reason to use an agent at 22%), home inspectors, plumbers, contractors, painters, landscapers, home stagers, and so many more!

Local real estate professionals are often members of community organizations and are usually well versed in their area’s history. Their ties to the community make them a great resource whether you plan to relocate to a new area or across town.

If your plans for 2018 include purchasing your dream home, let’s get together to discuss your options and to help you make the most powerful and confident decisions for you and your family.

Posted in First Time Home Buyers, For Buyers, For Sellers, Move-Up Buyers

There are many benefits to homeownership. One of the top benefits is protecting yourself from rising rents, by locking in your housing cost for the life of your mortgage.

A recent article by Apartment List addressed rising rents by stating:

“Rents are up 2.7% year-over-year at the national level. Year-over-year growth continues to fall between the 2.1% rate from this time last year and the 3.4% growth rate from October 2015.”

The article continues explaining that:

“Despite the seasonal slowdown, rents are still up year-over-year in 89 of the 100 Largest cities.

Additionally, the Urban Institute revealed that,

“Over a quarter of renters, or 11.1 million households, are severely cost burdened, spending at least half their income on rental housing.

These households struggle to save for a rainy day and pay other bills, including groceries and healthcare.

As we have previously mentioned, the results of the latest Rent vs. Buy Report from Trulia shows that homeownership remains cheaper than renting with a traditional 30-year fixed rate mortgage in the 100 largest metro areas in the United States.

The updated numbers show that the range is an average of 6.5% less expensive in San Jose (CA), all the way up to 57% less expensive in Detroit (MI) and 37.4% nationwide!

Perhaps you have already saved enough to buy your first home. A nationwide survey of about 24,000 renters found that 80% of millennial renters plan to eventually buy a house, but 72% cite affordability as their primary obstacle. Aside from affordability, one in three millennial renters have concerns about their credit scores, and another 53% said that a down payment is an obstacle.

Many first-time homebuyers who believe that they need a large down payment may be holding themselves back from their dream homes. As we have reported before, in many areas of the country, a first-time home buyer can save for a 3% down payment in less than two years. You may have already saved enough!

Don’t get caught in the trap that so many renters are currently in. If you are ready and willing to buy a home, find out if you are able. Let’s get together to determine if you can qualify for a mortgage now!

Posted in First Time Home Buyers, For Buyers, Rent vs. Buy

Here are four great reasons to consider buying a home today instead of waiting.

CoreLogic’s latest Home Price Index reports that home prices have appreciated by 7.0% over the last 12 months. The same report predicts that prices will continue to increase at a rate of 4.7% over the next year.

The bottom in home prices has come and gone. Home values will continue to appreciate for years. Waiting no longer makes sense.

Freddie Mac’s Primary Mortgage Market Survey shows that interest rates for a 30-year mortgage have hovered around 4%. Most experts predict that rates will rise over the next 12 months. The Mortgage Bankers Association, Fannie Mae, Freddie Mac and the National Association of Realtors are in unison, projecting that rates will increase by this time next year.

An increase in rates will impact YOUR monthly mortgage payment. A year from now, your housing expense will increase if a mortgage is necessary to buy your next home.

There are some renters who have not yet purchased a home because they are uncomfortable taking on the obligation of a mortgage. Everyone should realize that unless you are living with your parents rent-free, you are paying a mortgage – either yours or your landlord’s.

As an owner, your mortgage payment is a form of ‘forced savings’ that allows you to have equity in your home that you can tap into later in life. As a renter, you guarantee your landlord is the person with that equity.

Are you ready to put your housing cost to work for you?

The ‘cost’ of a home is determined by two major components: the price of the home and the current mortgage rate. It appears that both are on the rise.

But what if they weren’t? Would you wait?

Look at the actual reason you are buying and decide if it is worth waiting. Whether you want to have a great place for your children to grow up, you want your family to be safer, or you just want to have control over renovations, maybe now is the time to buy.

Posted in First Time Home Buyers, For Buyers, Move-Up Buyers

We recently shared that over the course of the last 12 months, home prices have appreciated by 7.0%. Over the same amount of time, interest rates have remained historically low which has allowed many buyers to enter the market.

As a seller, you will likely be most concerned about ‘short-term price’ – where home values are headed over the next six months. As a buyer, however, you must not be concerned about price, but instead about the ‘long-term cost’ of the home.

The Mortgage Bankers Association (MBA), Freddie Mac, and Fannie Mae all project that mortgage interest rates will increase by this time next year. According to CoreLogic’s most recent Home Price Index Report, home prices will appreciate by 4.7% over the next 12 months.

If home prices appreciate by 4.7% over the next twelve months as predicted by CoreLogic, here is a simple demonstration of the impact that an increase in interest rate would have on the mortgage payment of a home selling for approximately $250,000 today:

If buying a home is in your plan for 2018, doing it sooner rather than later could save you thousands of dollars over the terms of your loan.

Posted in First Time Home Buyers, For Buyers, For Sellers, Interest Rates, Move-Up Buyers, Pricing

So, you’ve been searching for that perfect house to call a ‘home,’ and you finally found it! The price is right, and in such a competitive market, you want to make sure that you make a good offer so that you can guarantee that your dream of making this house yours comes true!

Freddie Mac covered “4 Tips for Making an Offer” in their Executive Perspective. Here are the 4 tips they covered along with some additional information for your consideration:

“While it’s not nearly as fun as house hunting, fully understanding your finances is critical in making an offer.”

This ‘tip’ or ‘step’ should really take place before you start your home search process.

Getting pre-approved is one of many steps that will show home sellers that you are serious about buying, and will allow you to make your offer with the confidence of knowing that you have already been approved for a mortgage for that amount. You will also need to know if you are prepared to make any repairs that may need to be made to the house (ex: new roof, new furnace).

“Even though there are fewer investors, the inventory of homes for sale is also low and competition for housing continues to heat up in many parts of the country.”

The inventory of homes listed for sale has remained well below the 6-month supply that is needed for a ‘normal’ market. Buyer demand has continued to outpace the supply of homes for sale, causing buyers to compete with each other for their dream homes.

Make sure that as soon as you decide that you want to make an offer, you work with your agent to present it as soon as possible.

Freddie Mac offers this advice to help make your offer the strongest it can be:

“Your strongest offer will be comparable with other sales and listings in the neighborhood. A licensed real estate agent active in the neighborhoods you are considering will be instrumental in helping you put in a solid offer based on their experience and other key considerations such as recent sales of similar homes, the condition of the house and what you can afford.”

Talk with your agent to find out if there are any ways that you can make your offer stand out in this competitive market!

“It’s likely that you’ll get at least one counteroffer from the sellers so be prepared. The two things most likely to be negotiated are the selling price and closing date. Given that, you’ll be glad you did your homework first to understand how much you can afford.

Your agent will also be key in the negotiation process, giving you guidance on the counteroffer and making sure that the agreed-to contract terms are met.”

If your offer is approved, Freddie Mac urges you to “always get an independent home inspection, so you know the true condition of the home.” If the inspector uncovers undisclosed problems or issues, you can discuss any repairs that may need to be made with the seller, or cancel the contract.

Whether buying your first home or your fifth, having a local real estate professional who is an expert in their market on your side is your best bet to make sure the process goes smoothly. Let’s talk about how we can make your dreams of homeownership a reality!

Posted in First Time Home Buyers, For Buyers, Move-Up Buyers

![3 Tips for Making Your Dream Home a Reality [INFOGRAPHIC] | Simplifying The Market](http://files.simplifyingthemarket.com/wp-content/uploads/2017/12/06164805/20171208-Share-STM.jpg)

Posted in Down Payments, First Time Home Buyers, For Buyers, Infographics

According to CoreLogic’s latest Home Price Index, national home prices have appreciated by 7.0% from October 2016 to October 2017. This marks the second month in a row with a 7.0% year-over-year increase.

A lack of supply of homes for sale has led to upward pressure on home prices across the country, especially in areas where both existing and new home inventory have not kept up with buyer demand.

CoreLogic’s Chief Economist Frank Nothaft elaborated on the significance of such a large year-over-year gain,

“Single-family residential sales and prices continued to heat up in October. On a year-over-year basis, home prices grew in excess of 6 percent for four consecutive months ending in October, the longest such streak since June 2014.

This escalation in home prices reflects both the acute lack of supply and the strengthening economy.”

This is great news for homeowners who have gained over $13,000 in equity in their home over the last year! Those homeowners who had been on the fence as to whether or not to sell will be pleasantly surprised to find out that they now have an even larger profit to help cover a down payment on their dream home.

CoreLogic’s President & CEO Frank Martell had this to say,

“The acceleration in home prices is good news for both homeowners and the economy because it leads to higher home equity balances that support consumer spending and is a cushion against mortgage risk. However, for entry-level renters and first-time homebuyers, it leads to tougher affordability challenges.”

Any time the price of a home goes up there will likely be concern about the affordability of that home, but there is good news. Mortgage interest rates remain at historic lows, allowing buyers to enter the housing market and lock in a low monthly housing cost.

The report went on to mention that over the same 12-month period, median rental prices for a single-family home have also risen by 4.2%.

With rents and home prices rising at the same time, first-time buyers may find the task of saving for a down payment a little daunting. Low down payment programs are available and have been a very popular option for first-time buyers. The median down payment for first-time buyers in 2017 was only 5%!

If you are looking to enter the housing market, as either a buyer or a seller, let’s get together to go over exactly what’s going on in our neighborhood and discuss your options!

Posted in Down Payments, First Time Home Buyers, For Buyers, For Sellers, Move-Up Buyers, Pricing

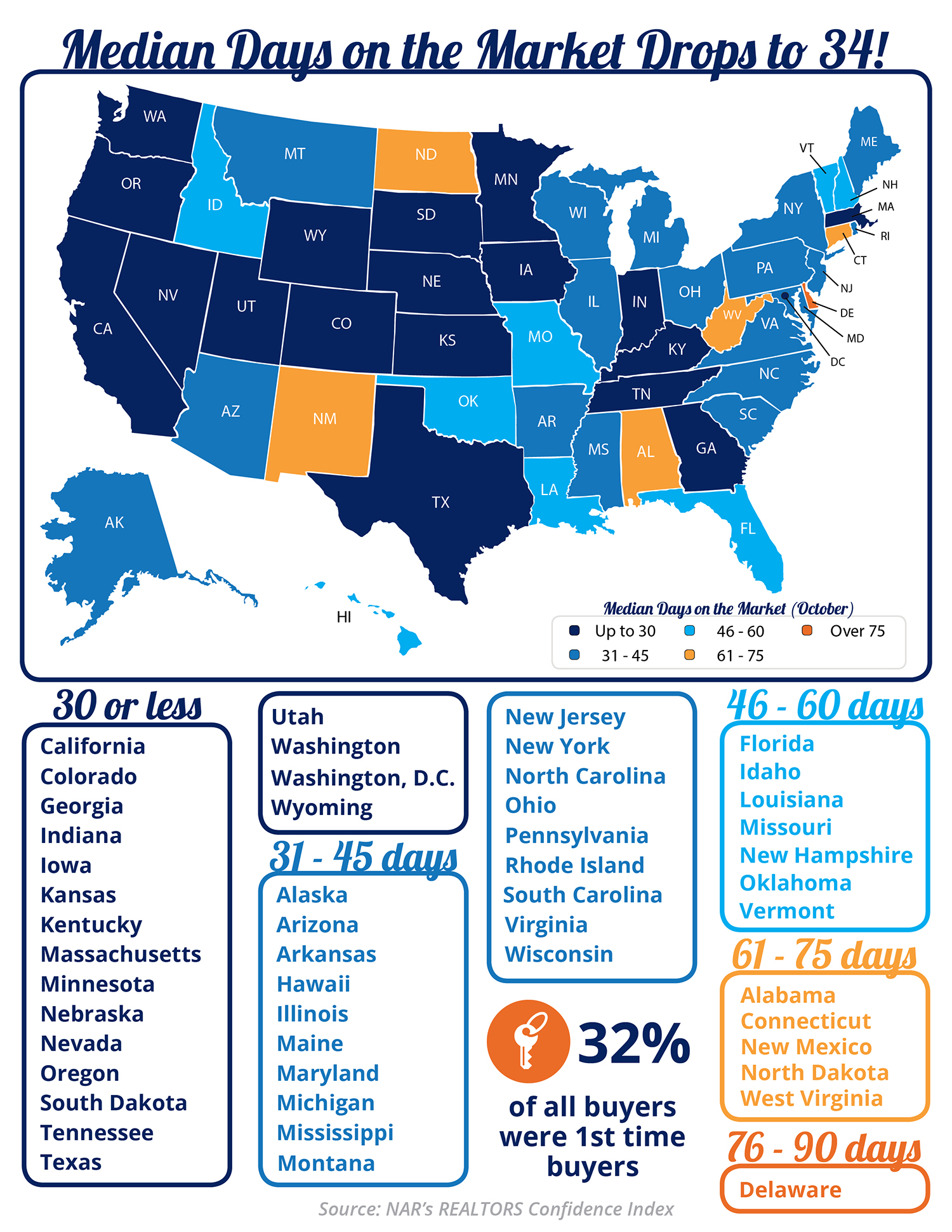

![Median Days on the Market Drops to 34! [INFOGRAPHIC] | Simplifying The Market](http://d39ah2zlibpm3g.cloudfront.net/wp-content/uploads/2017/11/30154450/20171201-Share-STM.jpg)

Posted in For Buyers, For Sellers, Infographics

There are many unsubstantiated theories as to why home values are continuing to increase. From those who are worried that lending standards are again becoming too lenient (data shows this is untrue), to those who are concerned that prices are again approaching boom peaks because of “irrational exuberance” (this is also untrue as prices are not at peak levels when they are adjusted for inflation), there seems to be no shortage of opinion.

However, the increase in prices is easily explained by the theory of supply & demand. Whenever there is a limited supply of an item that is in high demand, prices increase.

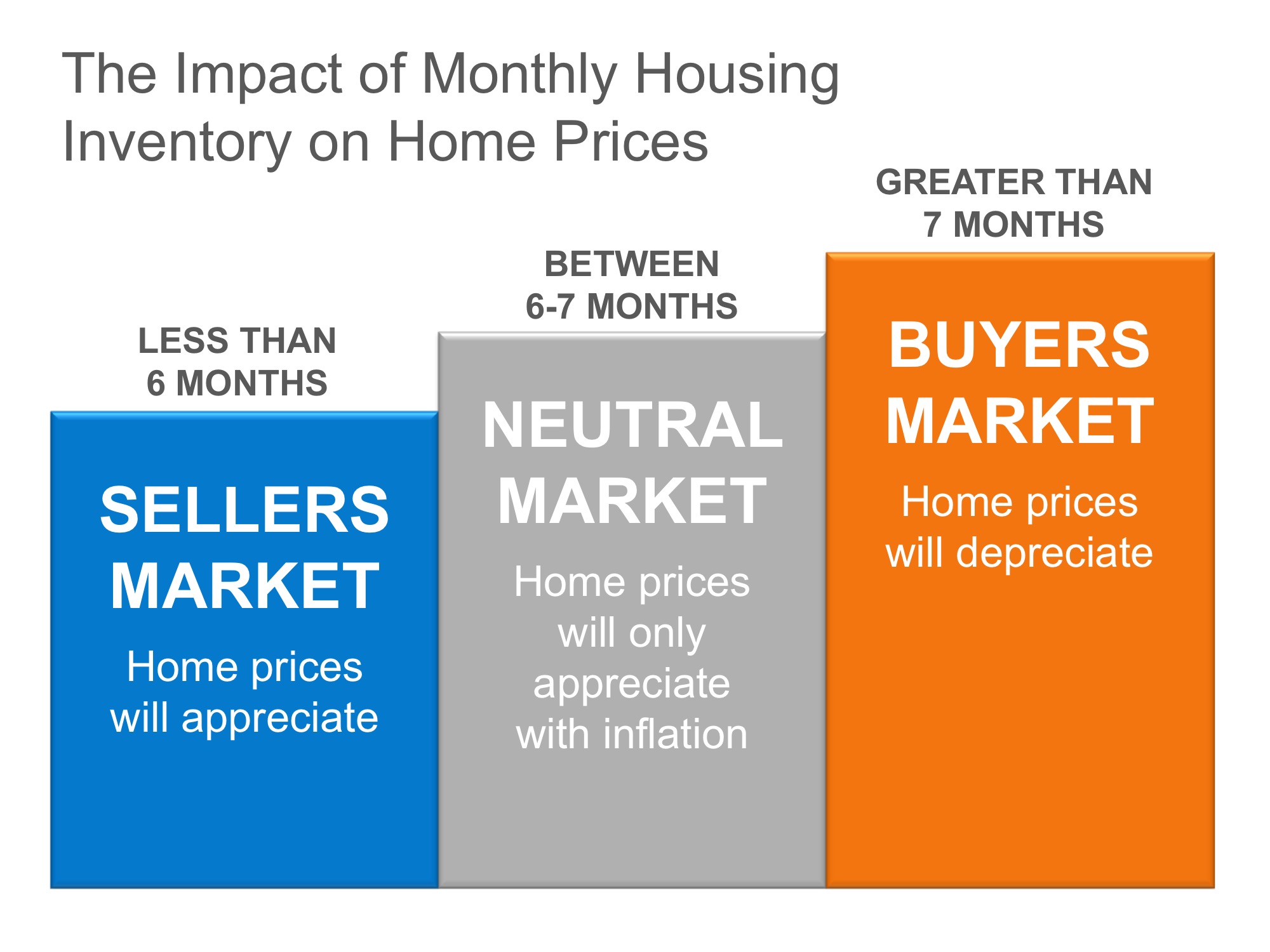

It is that simple. In real estate, it takes a six-month supply of existing salable inventory to maintain pricing stability. In most housing markets, anything less than six months will cause home values to appreciate and anything more than seven months will cause prices to depreciate (see chart 1).

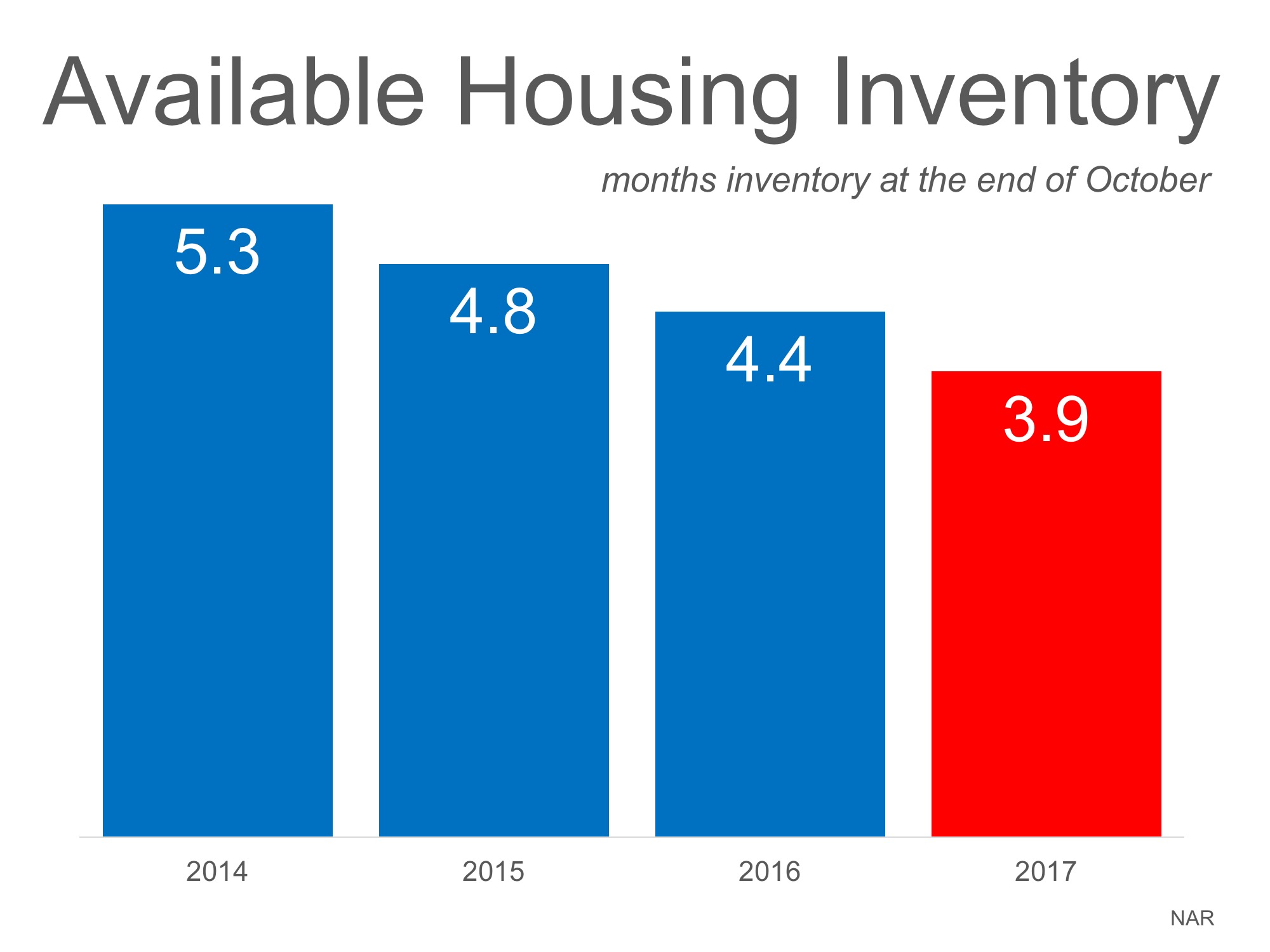

According to the Existing Home Sales Report from the National Association of Realtors (NAR), the monthly inventory of homes has been below six months for the last four years (see chart 2).

If buyer demand outpaces the current supply of existing homes for sale, prices will continue to appreciate. Nothing nefarious is taking place. It is simply the theory of supply & demand working as it should.

Posted in Buying Myths, First Time Home Buyers, For Buyers, Housing Market Updates, Move-Up Buyers, Pricing

For your home value estimate, enter the access code you received on the postcard, just click here: