Instant Home Estimate

For your home value estimate, enter the access code you received on the postcard, just click here:

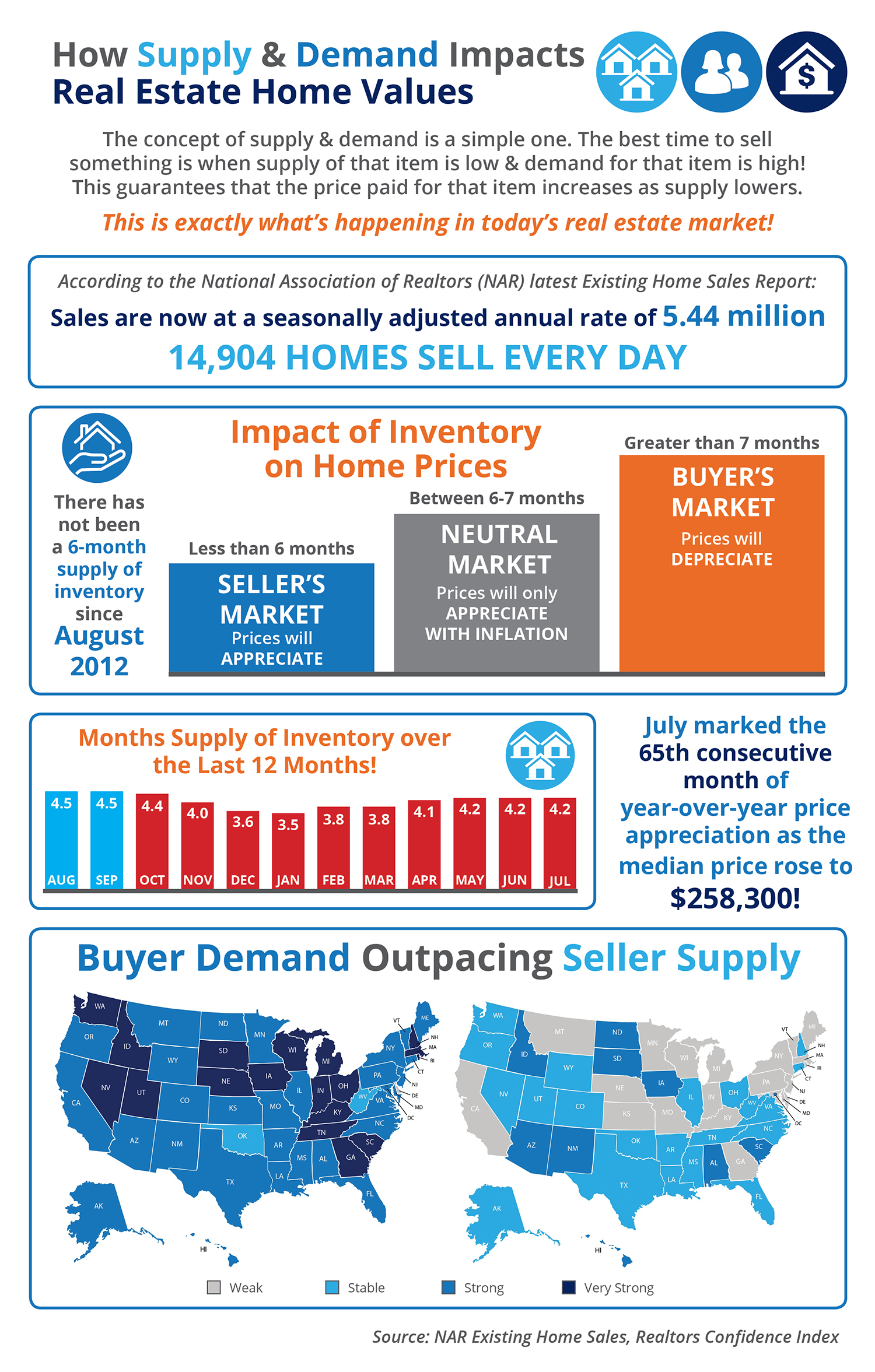

![How Supply and Demand Impacts Real Estate Home Values [INFOGRAPHIC] | Simplifying The Market](http://d39ah2zlibpm3g.cloudfront.net/wp-content/uploads/2017/09/06153544/20170908-Share-STM.jpg)

Posted in For Buyers, For Sellers, Housing Market Updates, Infographics

The biggest challenge in today’s real estate market is a lack of housing inventory. How big of a challenge is the housing shortage? Here are what four industry economists are saying on the issue (emphases added):

“The underlying fundamental issue is an overwhelming lack of supply… The supply of newly constructed homes is also sagging, adding to the supply challenges. Over the last eight years, housing demand has increased by 5.9 million, but the net new number of housing units has only increased by 3.5 million.”

“Everyone has been talking about tight inventory but I think we are OK calling it a straight up inventory crisis at this point. We just don’t have enough homes.”

“House prices today are higher than they were at the peak in the summer of 2006, near-record-low mortgage rates have boosted housing demand, and sales volume is robust. The spoiler is the lean inventory of houses for sale.”

“Listings in the affordable price range continue to be scooped up rapidly, but the severe housing shortages inflicting many markets are keeping a large segment of would-be buyers on the sidelines.”

If you are considering selling your house soon, now may be the time to get it on the market. The lack of competition could lead to a faster sale at a higher price.

Posted in For Buyers, For Sellers, Housing Market Updates, Move-Up Buyers

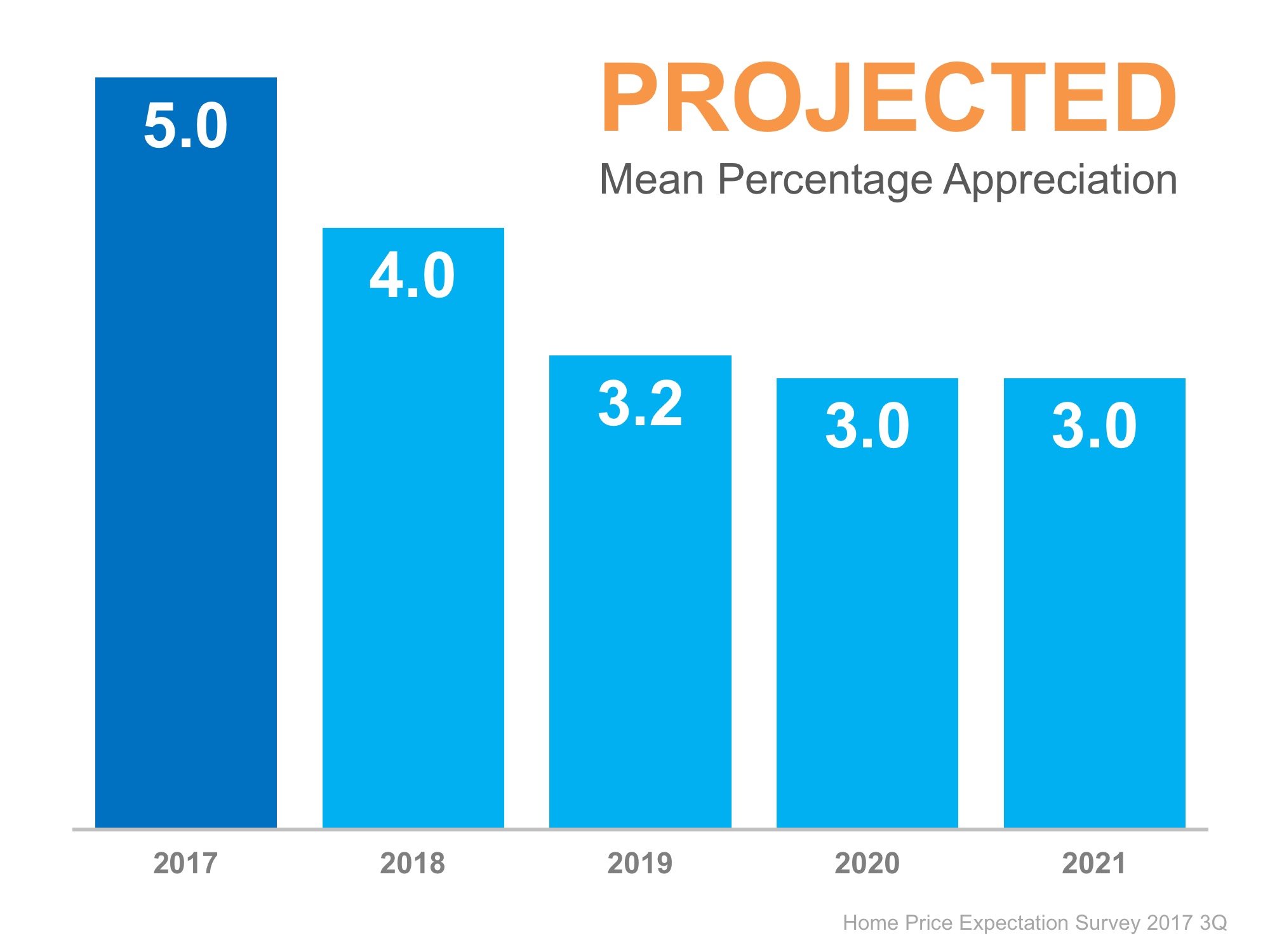

Today, many real estate conversations center on housing prices and where they may be headed. That is why we like the Home Price Expectation Survey.

Every quarter, Pulsenomics surveys a nationwide panel of over one hundred economists, real estate experts, and investment & market strategists about where they believe prices are headed over the next five years. They then average the projections of all 100+ experts into a single number.

Home values will appreciate by 5.0% over the course of 2017, 4.0% in 2018, 3.2% in 2019, 3.0% in 2020, and 3.0% in 2021. That means the average annual appreciation will be 3.64% over the next 5 years.

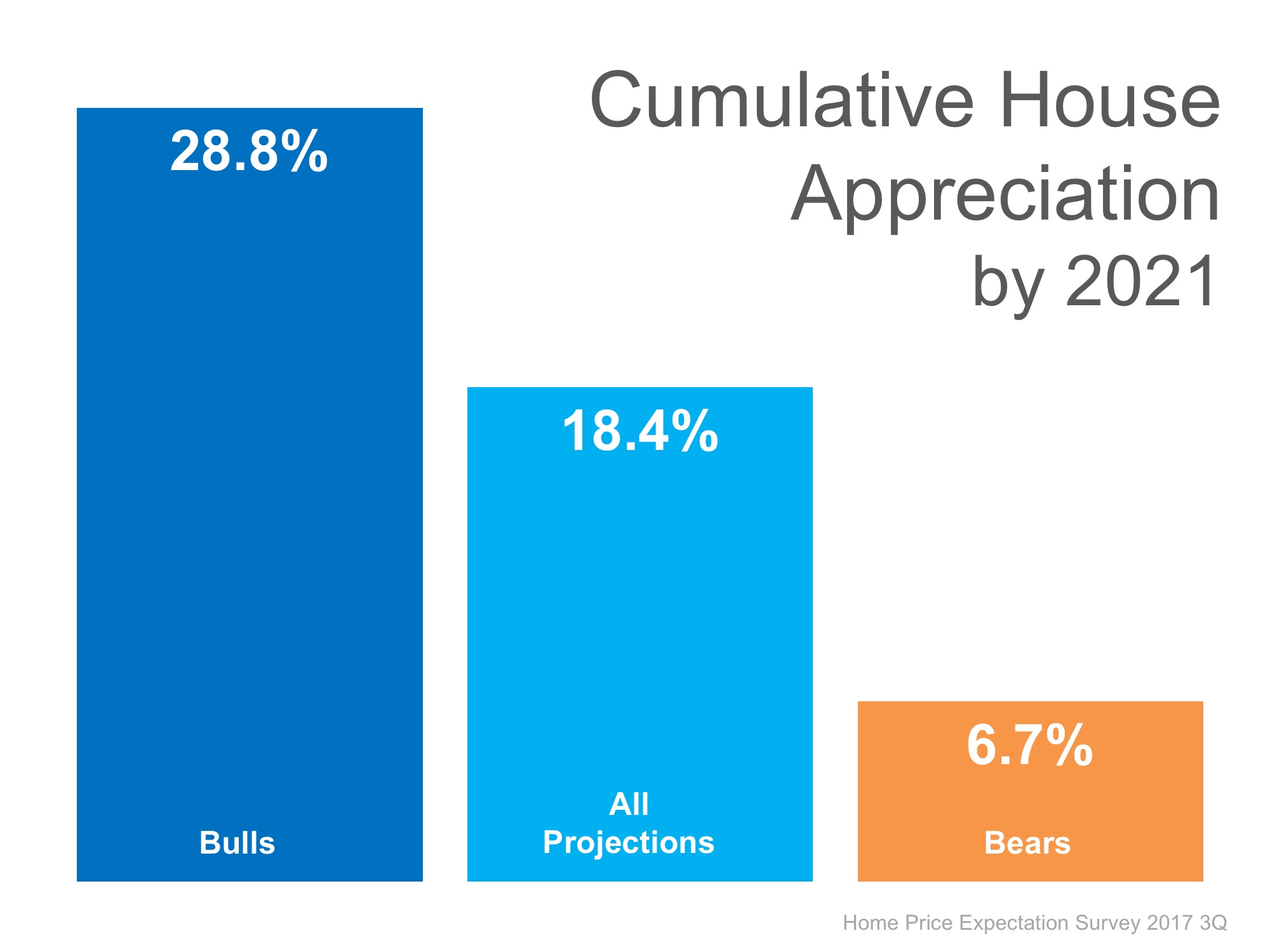

The prediction for cumulative appreciation increased from 17.8% to 18.4% by 2021. The experts making up the most bearish quartile of the survey are projecting a cumulative appreciation of 6.7%.

Individual opinions make headlines. We believe this survey is a fairer depiction of future values.

Posted in First Time Home Buyers, For Buyers, Housing Market Updates, Move-Up Buyers, Pricing

Does your current house fit your needs? Does it seem like everyone else is moving up and moving on to more luxurious surroundings? Are you wondering what it would take to start living your dream life?

Market conditions around the country have presented an opportunity like no other for those who are looking to make the jump to a premium or luxury home.

The National Association of Realtors reports that national inventory levels are now at a 4.3-month supply. A normal market, where prices appreciate with inflation, has 6-7-months inventory. The national market has echoed the conditions felt in the starter and trade-up markets as inventory has declined year-over-year for 25 consecutive months.

The chart below shows the relationship between the inventory of homes for sale and prices.

According to Trulia’s latest Inventory Report, the inventory of homes for sale in the two lower priced markets has dropped by double digit percentages over the last 12 months (16% for starter and 13% for trade-up homes). While the inventory of homes in the premium home category has dropped by only 4%.

This has created a seller’s market in the lower-priced markets, as 54% of homes were on the market for less than a month in the last Realtors Confidence Index, and a buyer’s market in the luxury market, where homes were on the market for an average of 160 days according to the Institute for Luxury Home Marketing.

If you are even thinking of listing your home and moving up to a luxury home, let’s get together to evaluate your ability to do so. Homeowners across the country are upgrading their homes, why can’t you? Your dream home is waiting!

Posted in For Buyers, For Sellers, Housing Market Updates, Move-Up Buyers

We previously informed you about a study conducted by TransUnion titled, “The Bubble, the Burst and Now – What Happened to the Consumer?” The study revealed that 1.5 million homeowners who were negatively impacted by the housing crisis could re-enter the housing market between 2016-2019.

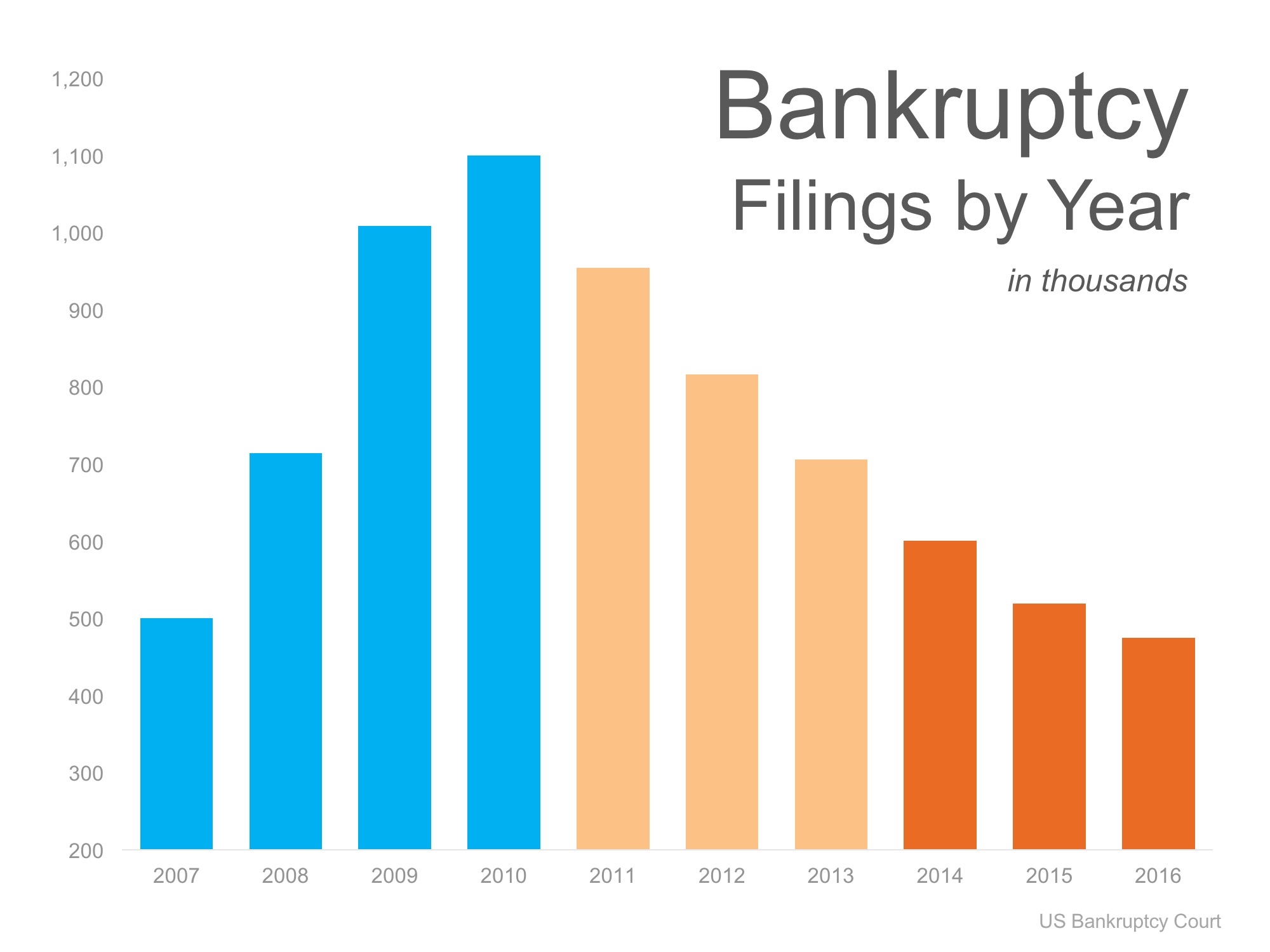

Recently, HousingWire analyzed data from the US Bankruptcy Courts and revealed that 6 million Americans will have their bankruptcies disappear off their credit reports over the next five years and that this could “possibly send a flood of more homebuyers into the housing market.”

The chart below shows the total number of bankruptcies filed by year in the US over the last 10 years. The light blue bars represent over 3.3 million people who have already waited the 7 years necessary for their reports to no longer include their bankruptcies.

As the article mentioned, in 2010 the number of chapter 7 bankruptcies increased to nearly 1.14 million. Now, 7 years later, they will begin to fade from credit histories, enabling prospective buyers to become homeowners again once their credit scores improve.

As we can see from both reports, the homeownership rate has the opportunity to increase drastically over the next few years with all of these boomerang buyers returning to the market.

If your family was negatively impacted by the housing bust, here is the light at the end of the tunnel! You may be able to purchase your dream home faster than you think!

Posted in For Buyers, Housing Market Updates

According to the recently released Modern Homebuyer Survey from ValueInsured, 58 percent of homeowners think there will be a “housing bubble and price correction” within the next 2 years.

After what transpired just ten years ago, we can understand the concern Americans have about the current increase in home prices. However, this market has very little in common with what happened last decade.

Today, housing inventory is at a 20-year low with new construction starts well below historic norms and financing a home is anything but simple in the current mortgage environment. The elements that precipitated the housing crash a decade ago do not exist in today’s real estate market.

The current increase in home prices is the result of a standard economic equation: when demand is high and supply is low, prices rise.

If you are one of the 58% of homeowners who are concerned about home values depreciating over the next two years and are hesitant to move up to the home of your dreams, take comfort in the latest Home Price Expectation Survey.

Once a quarter, a nationwide panel of over one hundred economists, real estate experts and investment & market strategists are surveyed and asked to project home values over the next five years. The experts predicted that houses would continue to appreciate through the balance of this year and in 2018, 2019, 2020 and 2021. They do expect lower levels of appreciation during these years than we have experienced over the last five years but do not call for a decrease in values (depreciation) in any of the years mentioned.

If you currently own a home and are thinking of moving-up to the home your family dreams about, don’t let the fear of another housing bubble get in the way as this housing market in no way resembles the market of a decade ago.

Posted in For Buyers, Housing Market Updates, Move-Up Buyers

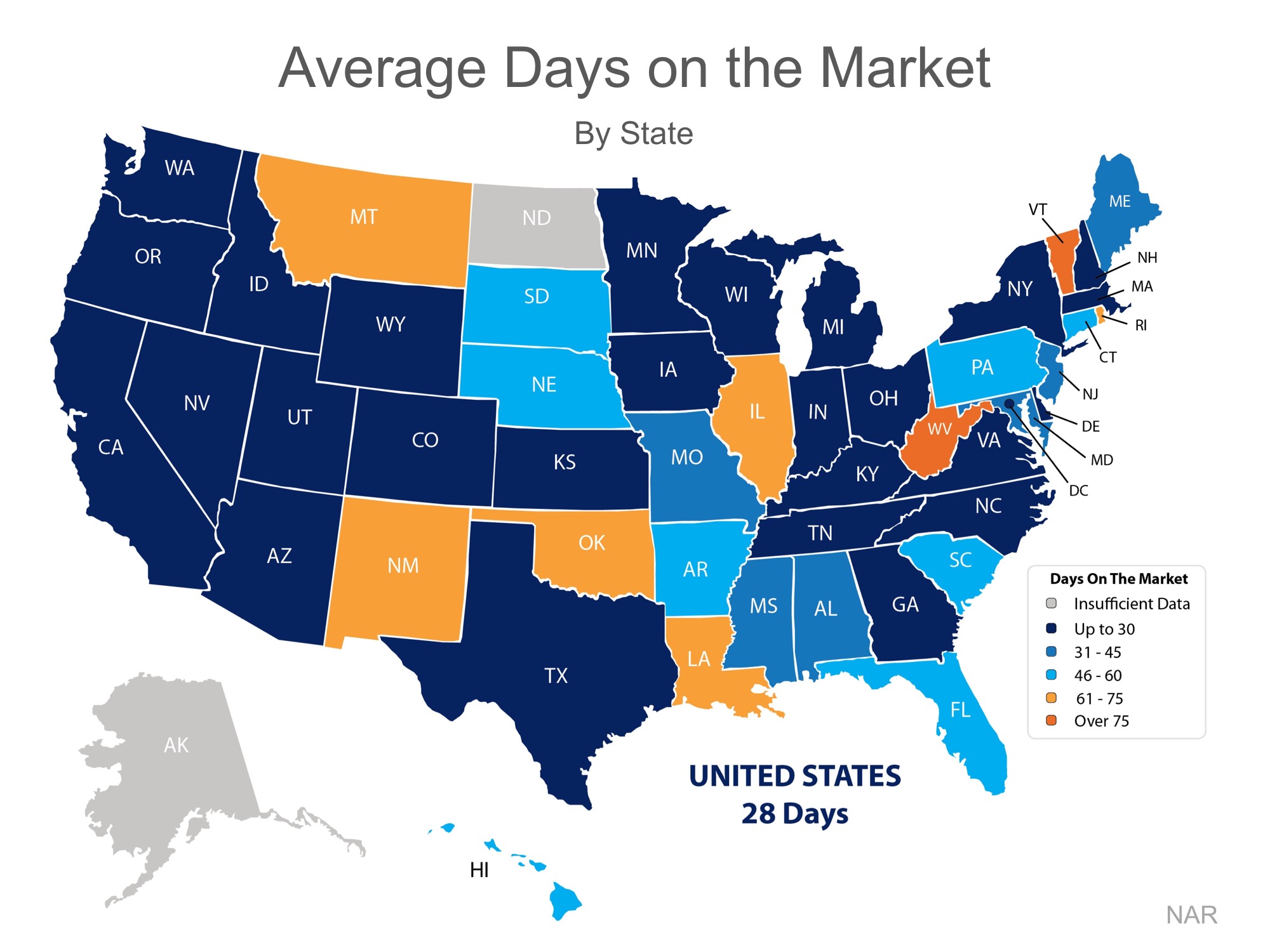

The National Association of Realtors (NAR) recently released their latest Existing Home Sales Report, which revealed that homes were on the market for an average of 28 days in June. This is a slight increase from the 27 days reported in May, but down from 34 days reported a year ago.

Among the 27 states with homes selling in 30 days or less are Washington, Utah, California, and Colorado. The map below was created using results from NAR’s Monthly Realtors Confidence Index Survey.

Buyer demand is increasing as the inventory of homes available for sale remains low. If you are thinking about listing your home for sale this year, let’s meet up so I can help you take advantage of current market conditions!

Posted in For Sellers, Housing Market Updates, Move-Up Buyers

Spring is traditionally the busiest season for real estate. Buyers, experiencing cabin fever all winter, emerge like flowers through the snow in search of their dream home. Homeowners, in preparation for the increased demand, are enticed to list their house for sale and move on to the home that will better fit their needs.

New data from CoreLogic shows that even though buyers came out in force, as predicted, homeowners did not make the jump to list their home in the second quarter of this year. Frank Nothaft, Chief Economist for CoreLogic had this to say,

“The growth in sales is slowing down, and this is not due to lack of affordability, but rather a lack of inventory. As of Q2 2017, the unsold inventory as a share of all households is 1.9 percent, which is the lowest Q2 reading in over 30 years.”

CoreLogic’s President & CEO, Frank Martell added,

“Home prices are marching ever higher, up almost 50 percent since the trough in March 2011.

While low mortgage rates are keeping the market affordable from a monthly payment perspective, affordability will likely become a much bigger challenge in the years ahead until the industry resolves the housing supply challenge.”

Overall inventory across the United States is down for the 25th consecutive month according to the latest report from the National Association of Realtors and now stands at a 4.3-month supply.

Market conditions in the starter and trade-up home markets are in line with the median US figures, but conditions in the luxury and premium markets are following an opposite path. Premium homes are staying on the market longer with ample inventory to suggest a buyer’s market.

Buyers are out in force, and there has never been a better time to move-up to a premium or luxury home. If you are considering selling your starter or trade-up home and moving up this year, let’s get together to discuss the exact conditions in our area.

Posted in For Sellers, Housing Market Updates

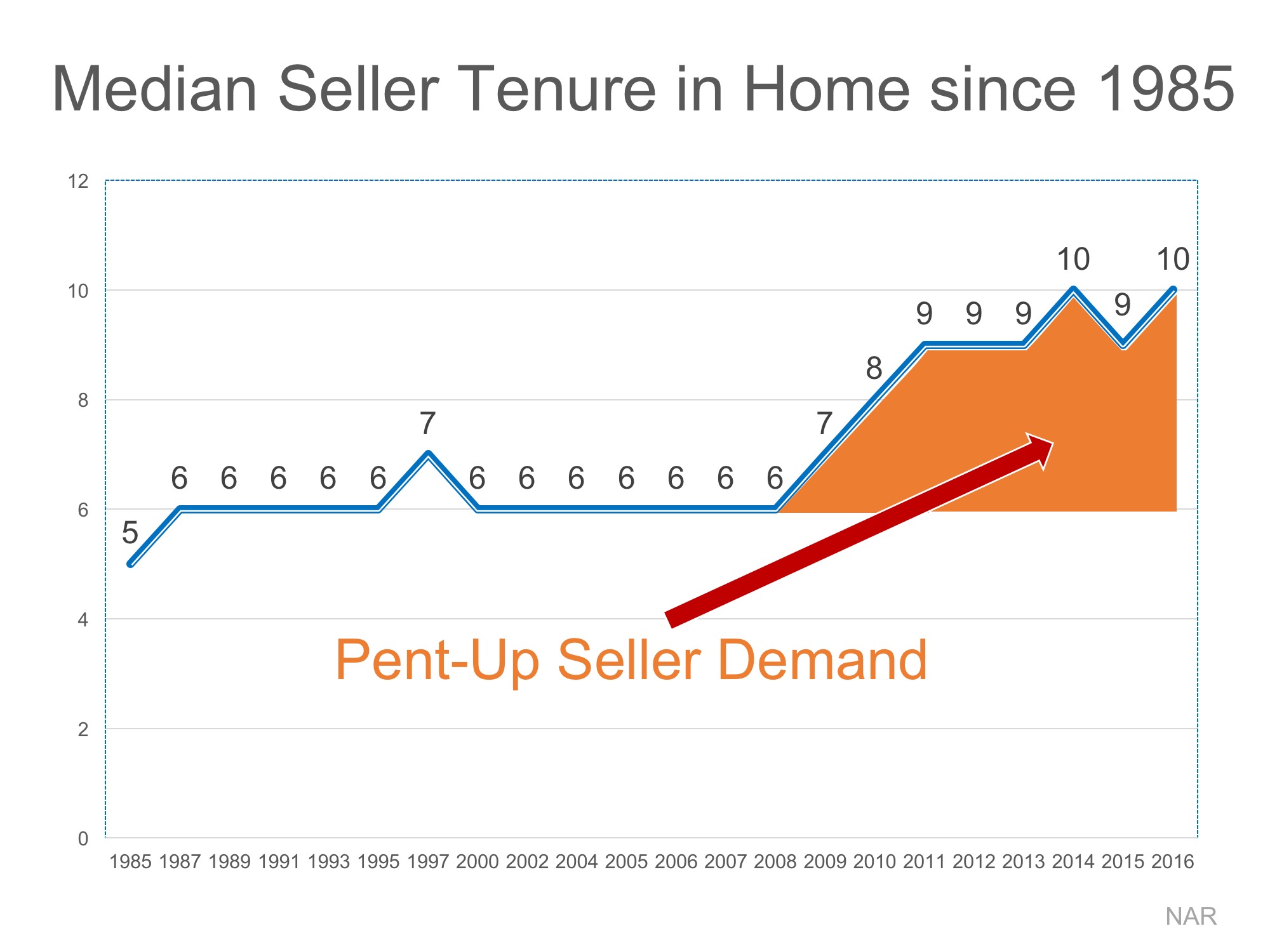

The National Association of Realtors (NAR) keeps historical data on many aspects of homeownership. One of the data points that has changed dramatically is the median tenure of a family in a home, meaning how long a family stays in a home prior to moving. As the graph below shows, for over twenty years (1985-2008), the median tenure averaged exactly six years. However, since 2008, that average is almost nine years – an increase of almost 50%.

The reasons for this change are plentiful!

The fall in home prices during the housing crisis left many homeowners in a negative equity situation (where their home was worth less than the mortgage on the property). Also, the uncertainty of the economy made some homeowners much more fiscally conservative about making a move.

With home prices rising dramatically over the last several years, 93.9% of homes with a mortgage are now in a positive equity situation with 78.8% of them having at least 20% equity, according to CoreLogic.

With the economy coming back and wages starting to increase, many homeowners are in a much better financial situation than they were just a few short years ago.

One other reason for the increase was brought to light by NAR in their 2017 Home Buyer and Seller Generational Trends Report. According to the report,

“Sellers 36 years and younger stayed in their home for six years…”

These homeowners who are either looking for more space to accommodate their growing families or for better school districts are more likely to move more often (compared to 10 years for typical sellers in 2016). The homeownership rate among young families, however, has still not caught up to previous generations, resulting in the jump we have seen in median tenure!

Many believe that a large portion of homeowners are not in a house that is best for their current family circumstance; They could be baby boomers living in an empty, four-bedroom colonial, or a millennial couple living in a one-bedroom condo planning to start a family.

These homeowners are ready to make a move, and since a lack of housing inventory is still a major challenge in the current housing market, this could be great news.

Posted in For Buyers, For Sellers, Housing Market Updates, Move-Up Buyers

Recent headlines exclaimed the homeownership rate, as reported by the Census Bureau, rose again in the second quarter of 2017. What didn’t get much attention in the reports is that the homeownership rate for American households under the age of 35 increased a full percentage point from last quarter’s 34.3% to 35.3%. Millennials proved to have the highest increase of any age group.

This came as a surprise to some considering Millennials have come to be known as the “renter” generation. However, a new study by First American, 6 Trends Poised to Reshape Homeownership Demand, revealed reasons why homeownership numbers will continue to increase for Millennials.

Why does that matter? First American explains:

“Our model shows that, all other factors being equal, the likelihood of homeownership increases by 3 percent for those that earn a bachelor’s degree over those with a high school degree. The likelihood of homeownership jumps another 3 percent for those that earn a graduate degree.”

The more educated, the better the likelihood for homeownership. And, as we mentioned: Millennials are the most educated generation in the U.S.

Marriage is a key determinate in homeownership. According to an analysis by First American, the homeownership rate is 30% higher among married couples compared to non-married households.

Millennials have put off marriage in the pursuit of higher education. As this group ages, more and more will marry and purchase a home.

According to the study:

“The homeownership rate is 1.7% higher for households with one or two children compared to households with no children, and it is 5.4 percent higher for households with three or more children.”

The report goes on to say that as Millennials grow older there may be an increase in not just marriage but also in married couples with children. That will probably also create a “corresponding” increase in homeownership demand.

The study goes on to explain that recent gains in income growth and a strengthening economy will also help all generations (including Millennials) be more willing and able to purchase a new home.

We guess the time has come to announce – Here come the Millennials!!

Posted in First Time Home Buyers, For Buyers, Housing Market Updates

For your home value estimate, enter the access code you received on the postcard, just click here: