Instant Home Estimate

For your home value estimate, enter the access code you received on the postcard, just click here:

In many markets across the country, the number of buyers searching for their dream homes greatly outnumbers the amount of homes for sale. This has led to a competitive marketplace where buyers often need to stand out. One way to show you are serious about buying your dream home is to get pre-qualified or pre-approved for a mortgage before starting your search.

Even if you are in a market that is not as competitive, knowing your budget will give you the confidence of knowing if your dream home is within your reach.

Freddie Mac lays out the advantages of pre-approval in the My Home section of their website:

“It’s highly recommended that you work with your lender to get pre-approved before you begin house hunting. Pre-approval will tell you how much home you can afford and can help you move faster, and with greater confidence, in competitive markets.”

One of the many advantages of working with a local real estate professional is that many have relationships with lenders who will be able to help you with this process. Once you have selected a lender, you will need to fill out their loan application and provide them with important information regarding “your credit, debt, work history, down payment and residential history.”

Freddie Mac describes the 4 Cs that help determine the amount you will be qualified to borrow:

Getting pre-approved is one of many steps that will show home sellers that you are serious about buying, and it often helps speed up the process once your offer has been accepted.

Many potential home buyers overestimate the down payment and credit scores needed to qualify for a mortgage today. If you are ready and willing to buy, you may be pleasantly surprised at your ability to do so as well.

Posted in First Time Home Buyers, For Buyers, Move-Up Buyers

In Realtor.com’s recent article, “Home Buyers’ Top Mortgage Fears: Which One Scares You?” they mention that “46% of potential home buyers fear they won’t qualify for a mortgage to the point that they don’t even try.”

Buyers overestimate the down payment funds needed to qualify for a home loan. According to the First Quarter 2017 Homeownership Program Index (HPI) from Down Payment Resource, saving for a down payment was the barrier that kept 70% of renters from buying.

Rob Chrane, CEO of Down Payment Resource had this to say,

“There are many mortgage-ready renters today, but they don’t know it. Often, homebuyers remain sidelined for years due to the down payment.”

Many believe that they need at least 20% down to buy their dream home, but programs are available that allow buyers put down as little as 3%. Many renters may actually be able to enter the housing market sooner than they ever imagined with new programs that have emerged allowing less cash out of pocket.

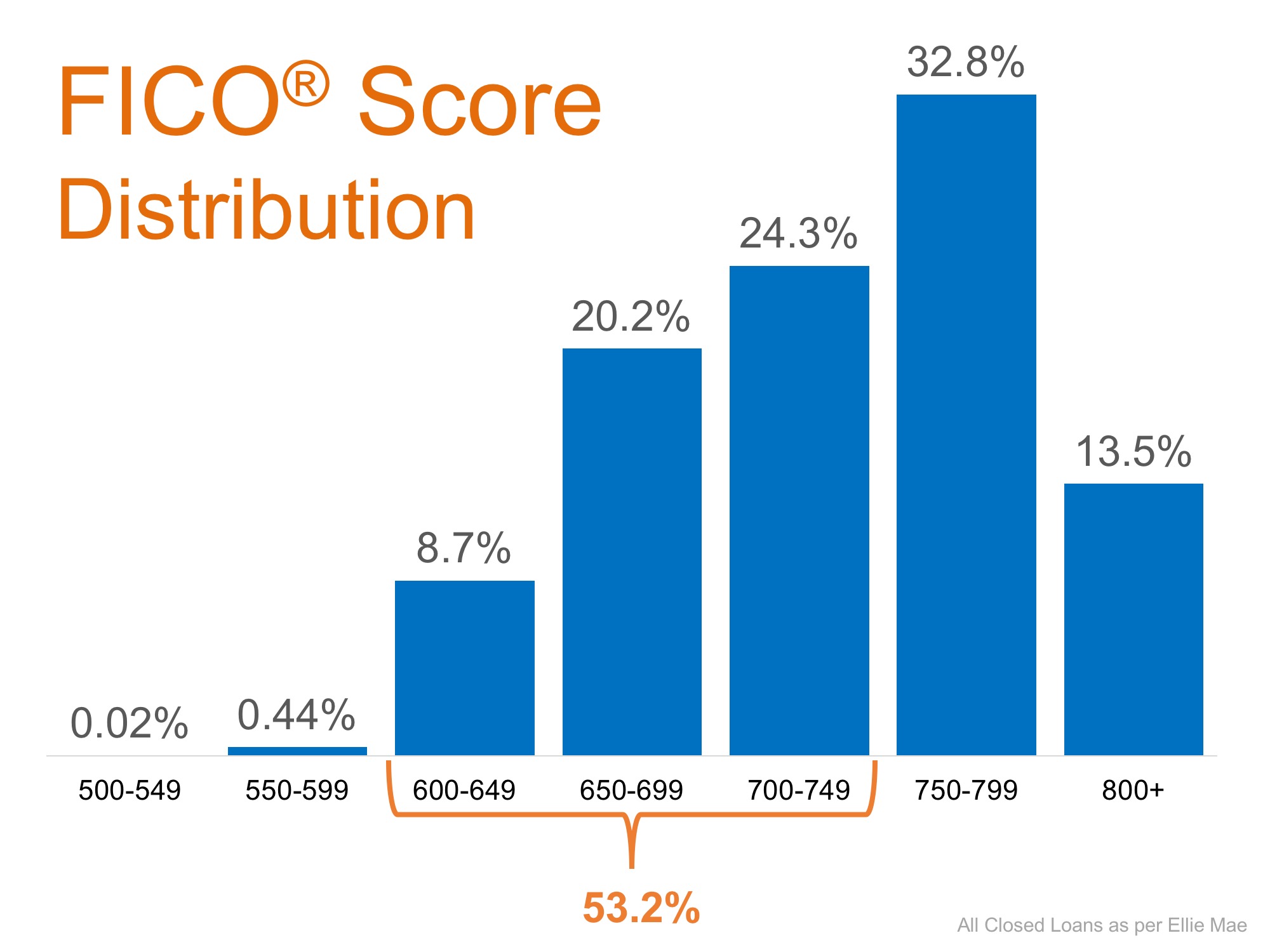

The survey revealed that 59% of Americans either don’t know (54%) or are misinformed (5%) about what FICO® score is necessary to qualify.

Many Americans believe a ‘good’ credit score is 780 or higher.

To help debunk this myth, let’s take a look at Ellie Mae’s latest Origination Insight Report, which focuses on recently closed (approved) loans.

As you can see in the chart above, 53.2% of approved mortgages had a credit score of 600-749.

Whether buying your first home or moving up to your dream home, knowing your options will make the mortgage process easier. Your dream home may already be within your reach.

Posted in Down Payments, First Time Home Buyers, For Buyers, Move-Up Buyers

CoreLogic’s latest Equity Report revealed that 91,000 properties regained equity in the first quarter of 2017. This is great news for the country, as 48.2 million of all mortgaged properties are now in a positive equity situation.

Frank Nothaft, CoreLogic’s Chief Economist, explains:

“One million borrowers achieved positive equity over the last year, which means risk continues to steadily decline as a result of increasing home prices.”

Frank Martell, President and CEO of CoreLogic, believes this is a great sign for the market in 2017 as well, as he had this to say:

“Homeowner equity increased by $766 billion over the last year, the largest increase since Q2 2014. The rising cushion of home equity is one of the main drivers of improved mortgage performance. Since home equity is the largest source of homeowner wealth, the increase in home equity also supports consumer balance sheets, spending and the broader economy.”

According to the Fannie Mae’s Home Purchase Sentiment Index (HPSI), more homeowners are beginning to realize that they may have more equity than they first thought.

“This is only the second time in the survey’s history that the net share of those saying it’s a good time to sell surpassed the net share of those saying it’s a good time to buy.”

This means that many Americans with a mortgage have an opportunity to take advantage of today’s seller’s market. With a sizeable equity position, many homeowners could easily move into a housing situation that better meets their current needs (moving to a larger home or downsizing).

Doug Duncan, Senior Vice President and Chief Economist at Fannie Mae spoke out on this issue:

“High home prices have led many consumers to give us the first clear indication we’ve seen in the National Housing Survey’s seven-year history that they think it’s now a seller’s market. However, we continue to see a lack of housing supply as many potential sellers are unwilling or unable to put their homes on the market…”

If you are one of the many Americans who is unsure of how much equity you have built in your home, don’t let that be the reason you fail to move on to your dream home in 2017! Let’s get together to evaluate your situation!

Posted in For Buyers, For Sellers, Move-Up Buyers

Posted in First Time Home Buyers, For Buyers, For Sellers, Infographics, Move-Up Buyers

Here are four great reasons to consider buying a home today, instead of waiting.

CoreLogic’s latest Home Price Index reports that home prices have appreciated by 7.1% over the last 12 months. The same report predicts that prices will continue to increase at a rate of 4.9% over the next year.

The bottom in home prices has come and gone. Home values will continue to appreciate for years. Waiting no longer makes sense.

Freddie Mac’s Primary Mortgage Market Survey shows that interest rates for a 30-year mortgage have remained around 4%. Most experts predict that they will begin to rise over the next 12 months. The Mortgage Bankers Association, Fannie Mae, Freddie Mac & the National Association of Realtors are in unison, projecting that rates will increase by this time next year.

An increase in rates will impact YOUR monthly mortgage payment. A year from now, your housing expense will increase if a mortgage is necessary to buy your next home.

There are some renters who have not yet purchased a home because they are uncomfortable taking on the obligation of a mortgage. Everyone should realize that, unless you are living with your parents rent-free, you are paying a mortgage – either yours or your landlord’s.

As an owner, your mortgage payment is a form of ‘forced savings’ that allows you to have equity in your home that you can tap into later in life. As a renter, you guarantee your landlord is the person with that equity.

Are you ready to put your housing cost to work for you?

The ‘cost’ of a home is determined by two major components: the price of the home and the current mortgage rate. It appears that both are on the rise.

But what if they weren’t? Would you wait?

Look at the actual reason you are buying and decide if it is worth waiting. Whether you want to have a great place for your children to grow up, you want your family to be safer or you just want to have control over renovations, maybe now is the time to buy.

Posted in First Time Home Buyers, For Buyers, Move-Up Buyers

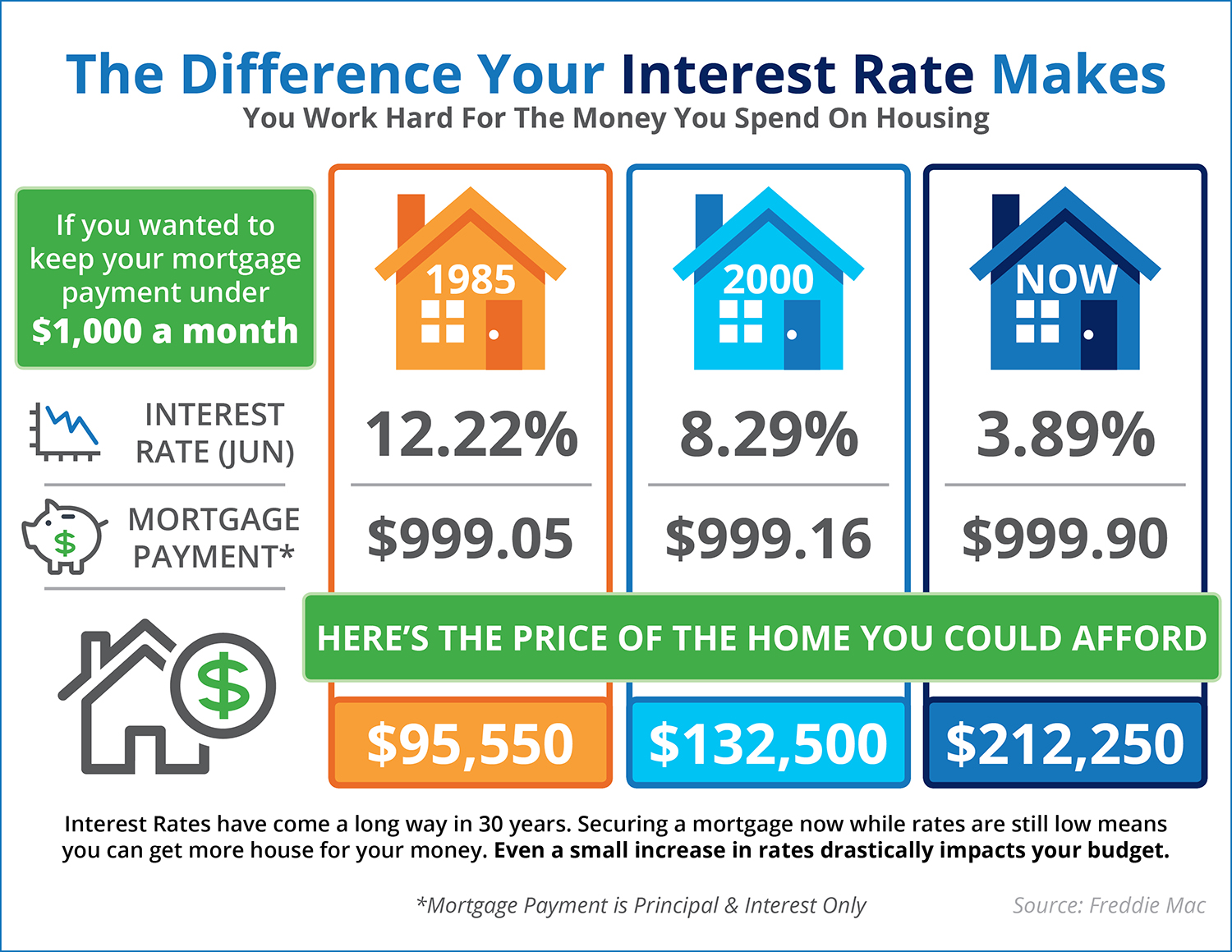

![The Impact Your Interest Rate Makes [INFOGRAPHIC] | Simplifying The Market](http://d39ah2zlibpm3g.cloudfront.net/wp-content/uploads/2017/06/08171202/20170609-Share-STM.jpg)

Posted in First Time Home Buyers, For Buyers, For Sellers, Infographics, Interest Rates, Move-Up Buyers

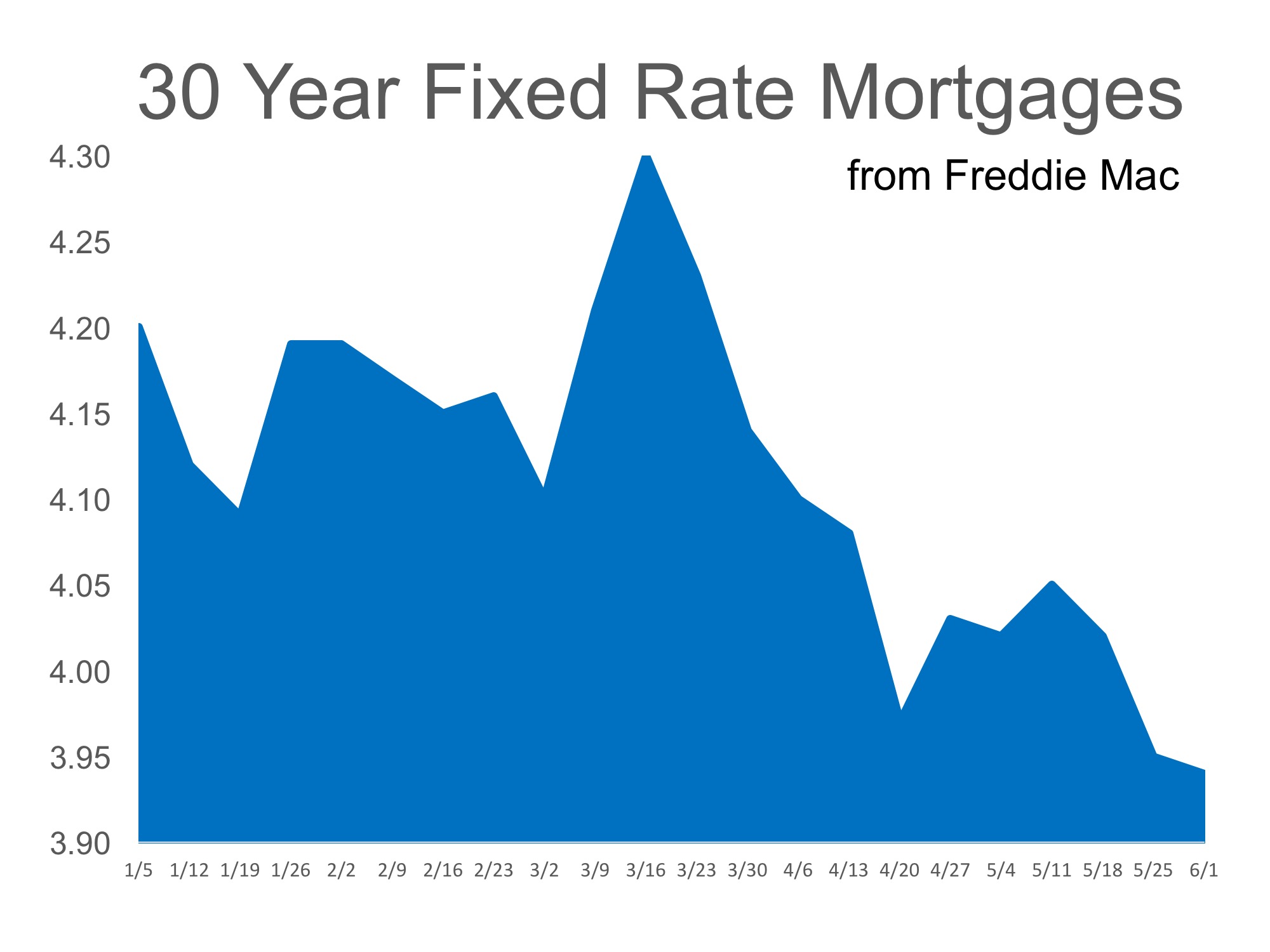

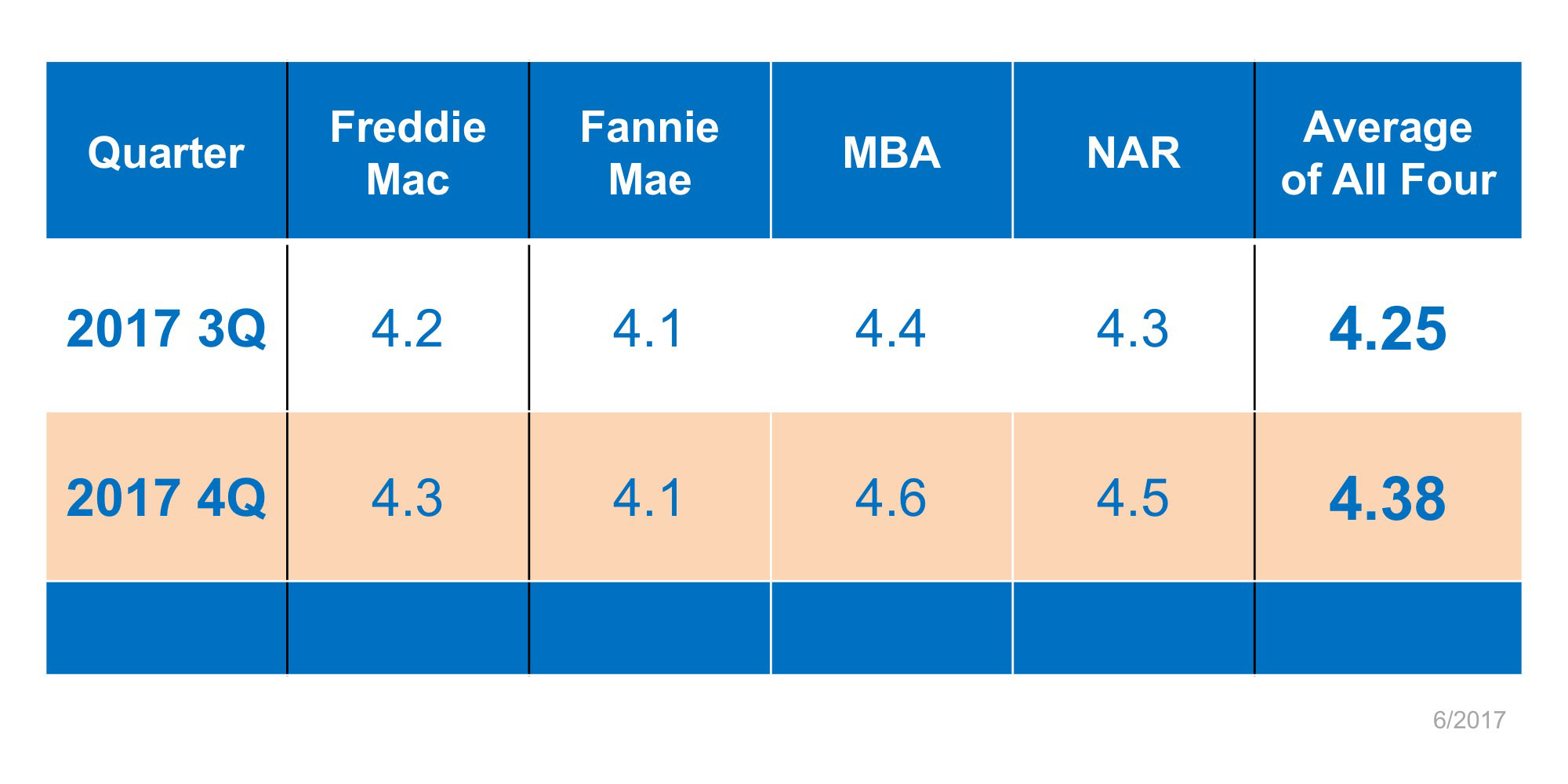

To start the year, housing experts all agreed on one thing: 2017 was going to be the year we would see mortgage interest rates begin to rise. After years of historically low rates, and an improving economy, the question wasn’t if they would increase but instead how much they would increase. Some thought we could see rates hit 5-5.5% by the end of the year.

However, the exact opposite has happened. Instead of higher rates as we head into the middle of 2017, we now have the lowest rates of the year (as reported by Freddie Mac). Here is a graph of mortgage rate movement since the beginning of the year:

Four major entities (Freddie Mac, Fannie Mae, the Mortgage Bankers Association and the National Association of Realtors) are still projecting that rates will increase by the fourth quarter of the year.

No one knows for sure where interest rates will be in six months. However, if you are thinking about buying your first house or trading up to the home of your dreams, you can still get a mortgage at historically low rates RIGHT NOW.

Posted in First Time Home Buyers, For Buyers, For Sellers, Interest Rates, Move-Up Buyers

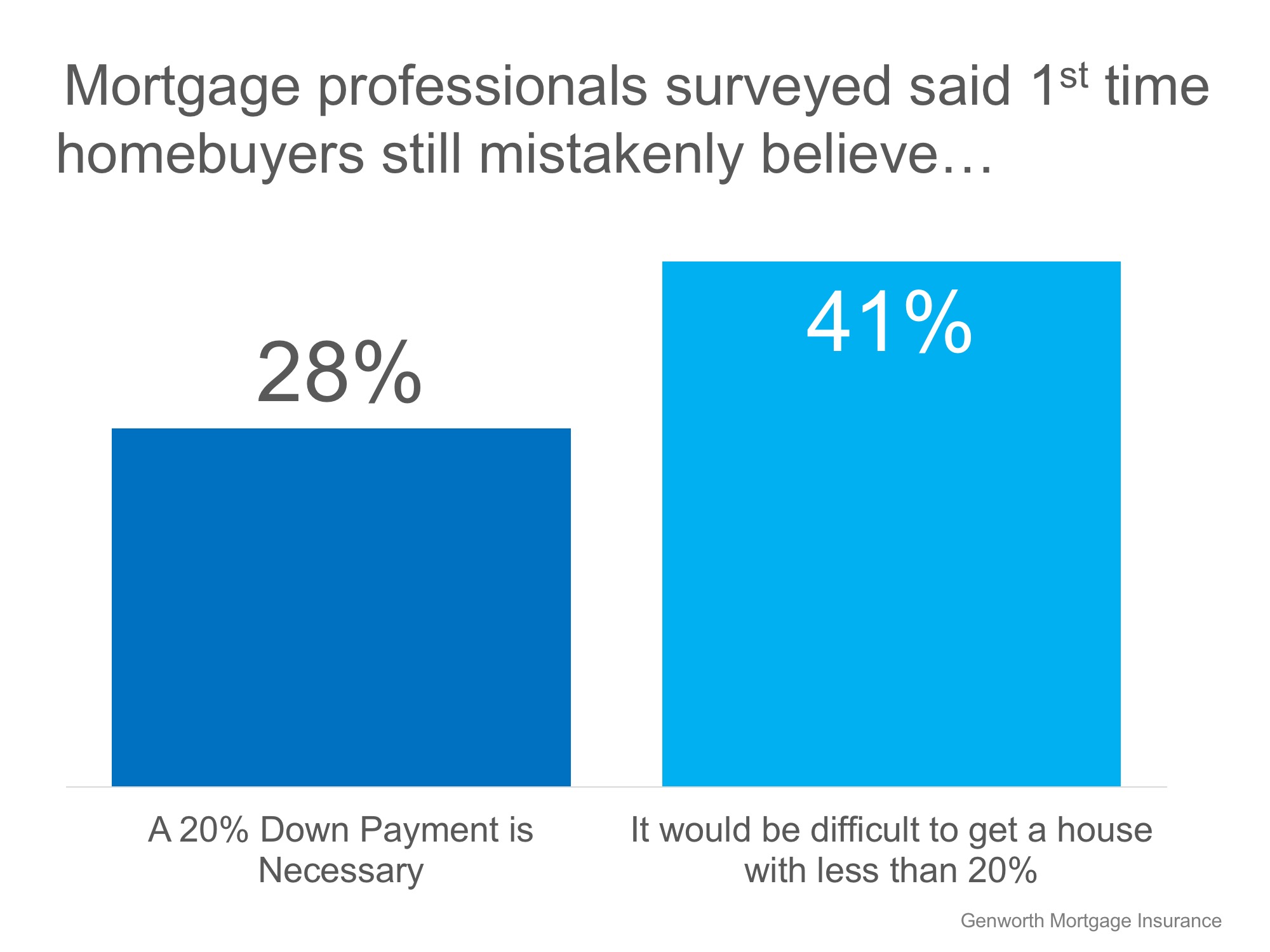

According to a recent survey conducted by Genworth Financial Inc. at the Annual Mortgage Bankers’ Association Secondary Market Conference, mortgage professionals say that first-time buyers still believe a 20% down payment is necessary to buy in today’s market.

Nearly 40% of mortgage industry professionals surveyed believe that a lack of knowledge about the home-buying process is keeping potential buyers on the sidelines. Saving for a down payment is often cited as a huge barrier for first-time homebuyers to make the leap into homeownership.

If homeowners believe that they need a 20% down payment to enter the market, they also believe that they will have to wait years (in some markets) to come up with the necessary funds to buy their dream homes.

The greatest source of confusion cited in the survey results centered around down payments. The results are broken down in the chart below:

Rohit Gupta, CEO of Genworth Mortgage Insurance had this to say,

“While first-time homebuyers continue to drive the purchase market, we believe many are staying on the sidelines due to the misconception that a 20 percent down payment is required to secure a mortgage.

There are various low down payment options available today that allow prospective homebuyers to reach their dreams of homeownership sooner. It is crucial that, as an industry, we proactively educate eligible borrowers about solutions that will enable them to buy a home when they’re ready.”

Don’t let a lack of understanding of the home-buying process keep you and your family out of the housing market. Let’s get together to discuss your options!

Posted in Down Payments, First Time Home Buyers, For Buyers, Move-Up Buyers

Posted in First Time Home Buyers, For Buyers, Infographics, Move-Up Buyers

Whether you are selling or buying a home, the real estate agent you hire is critical to guaranteeing your family makes the right decision. Most agents can walk you through the process and explain the industry ‘lingo,’ but you should expect so much more than that.

The housing crisis made everyone aware that truly understanding the real estate market is more complicated than it seems. Today, there are many questions your real estate agent must be able to answer to ensure your family is making the right decision. Here are just a few:

When you are interviewing an agent to represent your family in your next real estate transaction, make sure they can intelligently answer all your questions, while simply and effectively explaining what is happening in the current housing market.

Posted in First Time Home Buyers, For Buyers, For Sellers, Move-Up Buyers

For your home value estimate, enter the access code you received on the postcard, just click here: