Category: Move-Up Buyers

January 16th, 2017 by LHugh

In many markets across the country, the number of buyers searching for their dream homes greatly outnumbers the amount of homes for sale. This has led to a competitive marketplace where buyers often need to stand out. One way to show you are serious about buying your dream home is to get pre-qualified or pre-approved for a mortgage before starting your search.

Even if you are in a market that is not as competitive, knowing your budget will give you the confidence of knowing if your dream home is within your reach.

Freddie Mac lays out the advantages of pre-approval in the My Home section of their website:

“It’s highly recommended that you work with your lender to get pre-approved before you begin house hunting. Pre-approval will tell you how much home you can afford and can help you move faster, and with greater confidence, in competitive markets.”

One of the many advantages of working with a local real estate professional is that many have relationships with lenders who will be able to help you with this process. Once you have selected a lender, you will need to fill out their loan application and provide them with important information regarding “your credit, debt, work history, down payment and residential history.”

Freddie Mac describes the 4 Cs that help determine the amount you will be qualified to borrow:

- Capacity: Your current and future ability to make your payments

- Capital or cash reserves: The money, savings and investments you have that can be sold quickly for cash

- Collateral: The home, or type of home, that you would like to purchase

- Credit: Your history of paying bills and other debts on time

Getting pre-approved is one of many steps that will show home sellers that you are serious about buying, and it often helps speed up the process once your offer has been accepted.

Bottom Line

Many potential home buyers overestimate the down payment and credit scores needed to qualify for a mortgage today. If you are ready and willing to buy, you may be pleasantly surprised at your ability to do so as well.

Posted in First Time Home Buyers, For Buyers, Move-Up Buyers

January 12th, 2017 by Lum Hugh

It appears that Americans are regaining faith in the U.S. economy. The following indexes have each shown a dramatic jump in consumer confidence in their latest surveys:

- The University of Michigan Consumer Sentiment Index

- National Federation of Independent Businesses’ Small Business Optimism Index

- CNBC All-America Economic Survey

- The Conference Board Consumer Confidence Survey

It usually means good news for the housing market when the country sees an optimistic future. People begin to dream again about the home their family has always wanted, and some make plans to finally make that dream come true.

If you are considering moving up to your dream home, it may be better to do it earlier in the year than later. The two components of your monthly mortgage payment (home prices and interest rates) are both projected to increase as the year moves forward, and interest rates may increase rather dramatically. Here are some predictions on where rates will be by the end of the year:

HSH.com:

“We think that conforming 30-year fixed rates probably make it into the 4.625 percent to 4.75 percent range at some point during 2017 as a peak.”

Svenja Gudell, Zillow’s Chief Economist:

“I wouldn’t be surprised if the 30-year fixed mortgage rate hits 4.75 percent.”

Mark Fleming, the Chief Economist at First American:

“[I see] mortgage rates getting much closer to 5 percent at the end of next year.”

Lawrence Yun, NAR Chief Economist:

“By this time next year, expect the 30-year fixed rate to likely be in the 4.5 percent to 5 percent range.”

Bottom Line

If you are feeling good about your family’s economic future and are considering making a move to your dream home, doing it sooner rather than later makes the most sense.

Posted in For Buyers, Interest Rates, Move-Up Buyers

January 10th, 2017 by Lum Hugh

Many people wonder whether they should hire a real estate professional to assist them in buying their dream home or if they should first try to do it on their own. In today’s market: you need an experienced professional!

You Need an Expert Guide if You Are Traveling a Dangerous Path

The field of real estate is loaded with land mines; you need a true expert to guide you through the dangerous pitfalls that currently exist. Finding a home that is priced appropriately and is ready for you to move into can be tricky. An agent listens to your wants and needs, and can sift through the homes that do not fit within the parameters of your “dream home.”

A great agent will also have relationships with mortgage professionals and other experts that you will need in securing your dream home.

You Need a Skilled Negotiator

In today’s market, hiring a talented negotiator could save you thousands, perhaps tens of thousands of dollars. Each step of the way – from the original offer to the possible renegotiation of that offer after a home inspection, to the possible cancellation of the deal based on a troubled appraisal – you need someone who can keep the deal together until it closes.

Realize that when an agent is negotiating their commission with you, they are negotiating their own salary; the salary that keeps a roof over their family’s head; the salary that puts food on their family’s table. If they are quick to take less when negotiating for themselves and their families, what makes you think they will not act the same way when negotiating for you and your family?

If they were Clark Kent when negotiating with you, they will not turn into Superman when negotiating with the buyer or seller in your deal.

Bottom Line

Famous sayings become famous because they are true. You get what you pay for. Just like a good accountant or a good attorney, a good agent will save you money…not cost you money.

Posted in First Time Home Buyers, For Buyers, Move-Up Buyers

January 5th, 2017 by Lum Hugh

Last week, CNBC ran an article quoting self-made millionaire David Bach explaining that not purchasing a home is “the single biggest mistake millennials are making” because buying real estate is “an escalator to wealth.”

Bach went on to explain:

“If millennials don’t buy a home, their chances of actually having any wealth in this country are little to none. The average homeowner to this day is 38 times wealthier than a renter.”

In his bestselling book, “The Automatic Millionaire,” Bach does the math:

“As a renter, you can easily spend half a million dollars or more on rent over the years ($1,500 a month for 30 years comes to $540,000), and in the end wind up just where you started — owning nothing. Or you can buy a house and spend the same amount paying down a mortgage, and in the end wind up owning your own home free and clear!”

Who is David Bach?

Bach is a self-made millionaire who has written nine consecutive New York Times bestsellers. His book, “The Automatic Millionaire,” spent 31 weeks on the New York Times bestseller list. He is one of the only business authors in history to have four books simultaneously on the New York Times, Wall Street Journal, BusinessWeek and USA Today bestseller lists.

He has been a contributor to NBC’s Today Show appearing more than 100 times, has been a regular on ABC, CBS, Fox, CNBC, CNN, Yahoo, The View, and PBS, and has been profiled in many major publications, including The New York Times, BusinessWeek, USA Today, People, Reader’s Digest, Time, Financial Times, The Washington Post, The Wall Street Journal, Working Woman, Glamour, Family Circle, Redbook, Huffington Post, Business Insider, Investors’ Business Daily, and Forbes.

Bottom Line

Whenever a well-respected millionaire gives investment advice, people usually clamor to hear it. This millionaire gave simple advice – if you don’t yet live in your own home, go buy one.

Posted in First Time Home Buyers, For Buyers, Millennials, Move-Up Buyers

December 30th, 2016 by Lum Hugh

![5 Reasons to Resolve to Hire a Real Estate Professional [INFOGRAPHIC] | Simplifying The Market](http://www.simplifyingthemarket.com/wp-content/uploads/2016/12/5-Reasons-to-Resolve-STM.jpg)

Some Highlights:

- As we usher in the new year, one thing is for certain… if you plan to buy or sell a house this year, you need a real estate professional on your team!

- There are many benefits to using a local professional!

- Pick a pro who knows your local market and can help you navigate the housing market!

Posted in First Time Home Buyers, For Buyers, For Sellers, Infographics, Move-Up Buyers

December 27th, 2016 by LHugh

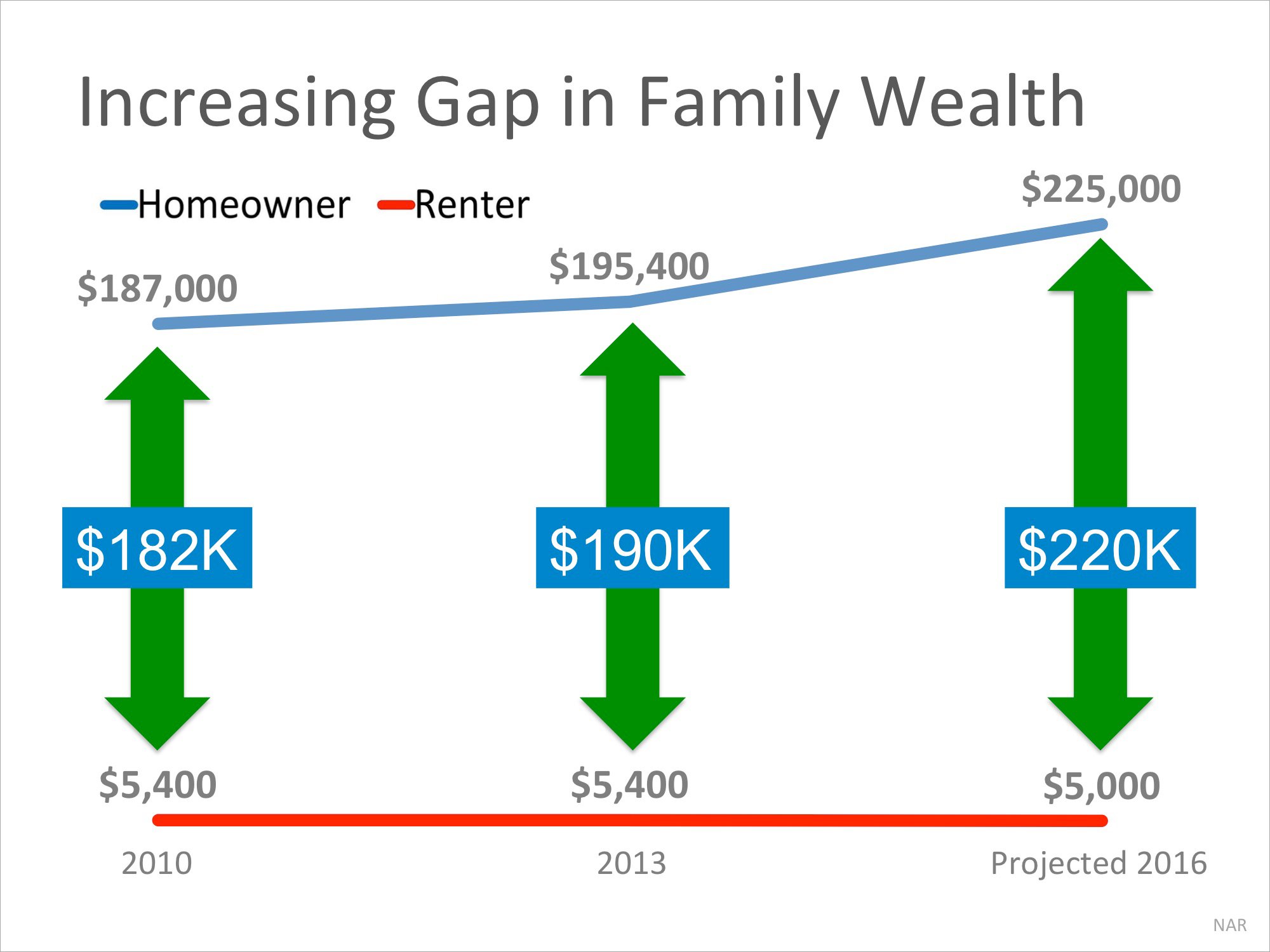

Every three years, the Federal Reserve conducts a Survey of Consumer Finances in which they collect data across all economic and social groups. The latest survey, which includes data from 2010-2013, reports that a homeowner’s net worth is 36 times greater than that of a renter ($194,500 vs. $5,400).

In a Forbes article, the National Association of Realtors’ (NAR) Chief Economist Lawrence Yun predicts that by the end of 2016, the net worth gap will widen even further to 45 times greater.

The graph below demonstrates the results of the last two Federal Reserve studies and Yun’s prediction:

Put Your Housing Cost to Work for You

As we’ve said before, simply put, homeownership is a form of ‘forced savings.’ Every time you pay your mortgage, you are contributing to your net worth. Every time you pay your rent, you are contributing to your landlord’s net worth.

The latest National Housing Pulse Survey from NAR reveals that 85% of consumers believe that purchasing a home is a good financial decision. Yun comments:

“Though there will always be discussion about whether to buy or rent, or whether the stock market offers a bigger return than real estate, the reality is that homeowners steadily build wealth. The simplest math shouldn’t be overlooked.”

Bottom Line

If you are interested in finding out if you could put your housing cost to work for you by purchasing a home, let’s get together and evaluate your ability to buy today!

Posted in First Time Home Buyers, For Buyers, Move-Up Buyers

December 1st, 2016 by LHugh

According to a recent report by Trulia, “buying is cheaper than renting in 100 of the largest metro areas by an average of 37.7%.” That may have some thinking about buying a home instead of signing another lease extension, but does that make sense from a financial perspective?

In the report, Ralph McLaughlin, Trulia’s Chief Economist explains:

“Owning a home is one of the most common ways households build long-term wealth, as it acts like a forced savings account. Instead of paying your landlord, you can pay yourself in the long run through paying down a mortgage on a house.”

The report listed five reasons why owning a home makes financial sense:

- Mortgage payments can be fixed while rents go up.

- Equity in your home can be a financial resource later.

- You can build wealth without paying capital gains.

- A mortgage can act as a forced savings account.

- Overall, homeowners can enjoy greater wealth growth than renters.

Bottom Line

Before you sign another lease, let’s get together and discuss all your options.

Posted in First Time Home Buyers, For Buyers, Move-Up Buyers

August 26th, 2016 by LHugh

Some Highlights:

- The concept of Supply & Demand is a simple one. The best time to sell something is when supply of that item is low & demand for that item is high!

- Anything under a 6-month supply is a Seller’s Market!

- There has not been a 6-months inventory supply since August 2012!

- Buyer Demand continues to outpace Seller Supply!

Posted in First Time Home Buyers, For Buyers, For Sellers, Housing Market Updates, Infographics, Move-Up Buyers

April 30th, 2016 by LHugh

We are often asked why there is so much paperwork mandated by the bank for a mortgage loan application when buying a home today. It seems that the bank needs to know everything about us and requires three separate sources to validate each and every entry on the application form.Many buyers are being told by friends and family that the process was a hundred times easier when they bought their home ten to twenty years ago.

There are two very good reasons that the loan process is much more onerous on today’s buyer than perhaps any time in history.

1. The government has set new guidelines that now demand that the bank prove beyond any doubt that you are indeed capable of affording the mortgage.

During the run-up in the housing market, many people ‘qualified’ for mortgages that they could never pay back. This led to millions of families losing their home. The government wants to make sure this can’t happen again.

2. The banks don’t want to be in the real estate business.

Over the last seven years, banks were forced to take on the responsibility of liquidating millions of foreclosures and also negotiating another million plus short sales. Just like the government, they don’t want more foreclosures. For that reason, they need to double (maybe even triple) check everything on the application.

However, there is some good news in the situation.

The housing crash that mandated that banks be extremely strict on paperwork requirements also allows you to get a mortgage interest rate as low as 3.43%, the latest reported rate from Freddie Mac.

The friends and family who bought homes ten or twenty years ago experienced a simpler mortgage application process but also paid a higher interest rate (the average 30 year fixed rate mortgage was 8.12% in the 1990’s and 6.29% in the 2000’s). If you went to the bank and offered to pay 7% instead of less than 4%, they would probably bend over backwards to make the process much easier.

Bottom Line

Instead of concentrating on the additional paperwork required, let’s be thankful that we are able to buy a home at historically low rates.

Posted in First Time Home Buyers, For Buyers, Move-Up Buyers

According to the latest Beracha, Hardin & Johnson Buy vs. Rent (BH&J) Index homeownership is a better way to produce greater wealth, on average, than renting.

The BH&J Index is a quarterly report that attempts to answer the question:

Is it better to rent or buy a home in today’s housing market?

The index examines the entire US housing market and then isolates 23 major markets for comparison. The researchers use a “’horse race’ comparison between an individual that is buying a home and an individual that rents a similar quality home and reinvests all monies otherwise invested in homeownership.”

Ken Johnson Ph.D., Real Estate Economist & Professor at Florida Atlantic University, and one of the index’s authors states:

“The nation as a whole is in buy territory. Continued near record low mortgage rates, unsteady stock market performance, and rents (on average) now out pacing the cost of ownership (maintenance, taxes, insurance, etc.) all combine to favor owning and building wealth through home equity over renting and reinvesting in a portfolio of stocks and bonds.”

Dallas, Denver and Houston currently remain deep in rent territory but, “there is some degree of good news from these markets for homeowners as the cost of renting is now increasing at a faster rate than the cost of homeownership — reducing the advantage of renting over buying.”

Bottom Line

Buying a home makes sense socially and financially. Rents are predicted to increase substantially in the next year, so lock in your housing cost with a mortgage payment now.

To Find Out More About the Study: The BH&J Index and other FAU real estate activities are sponsored by Investments Limited of Boca Raton. The BH&J Index is published quarterly and is available online at http://business.fau.edu/buyvsrent.

Posted in First Time Home Buyers, For Buyers, Housing Market Updates, Move-Up Buyers