Instant Home Estimate

For your home value estimate, enter the access code you received on the postcard, just click here:

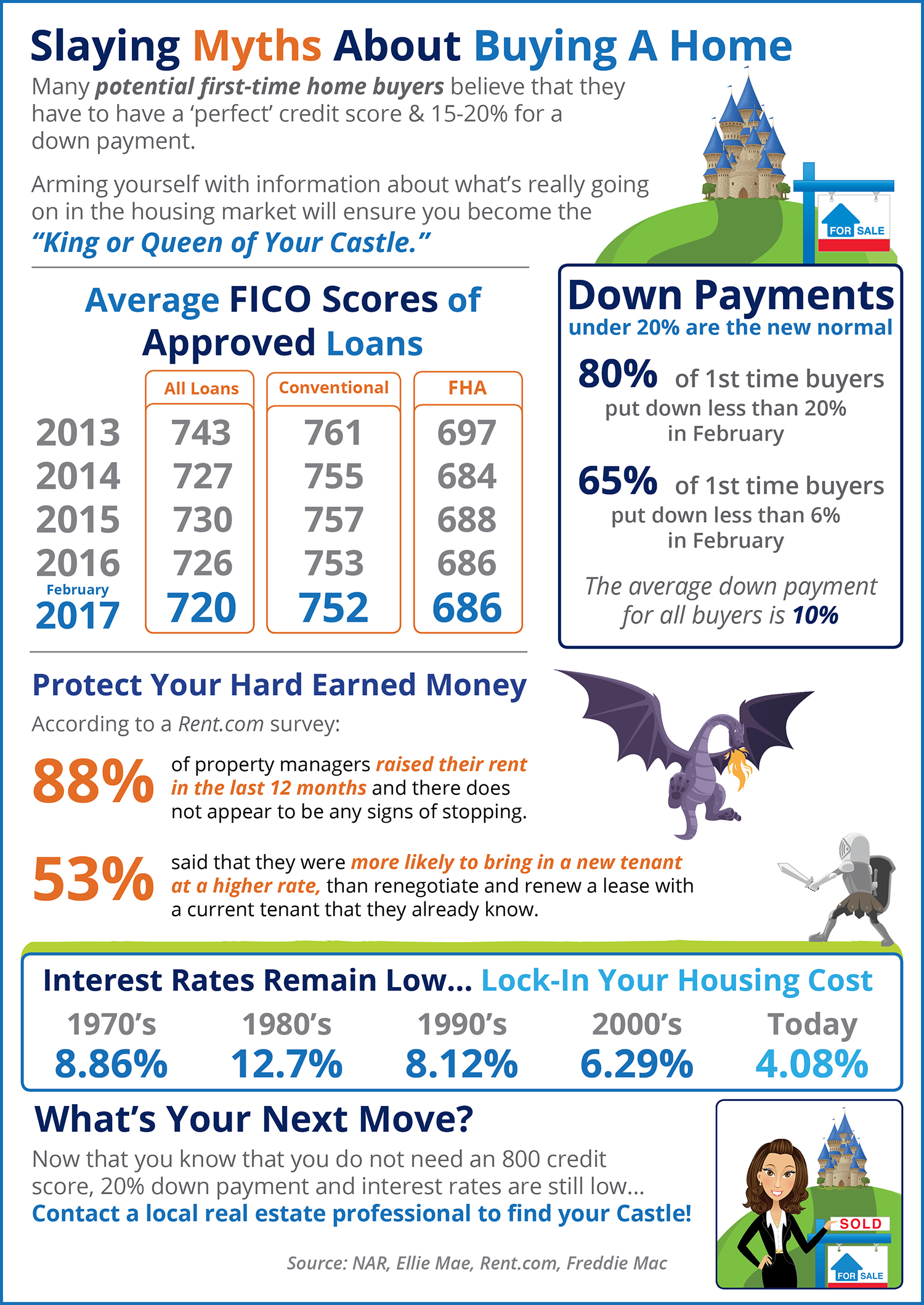

Many potential homebuyers believe that they need a 20% down payment and a 780 FICO® score to qualify to buy a home, which stops many of them from even trying! Here are some facts:

Posted in Buying Myths, Down Payments, First Time Home Buyers, For Buyers, Infographics, Millennials

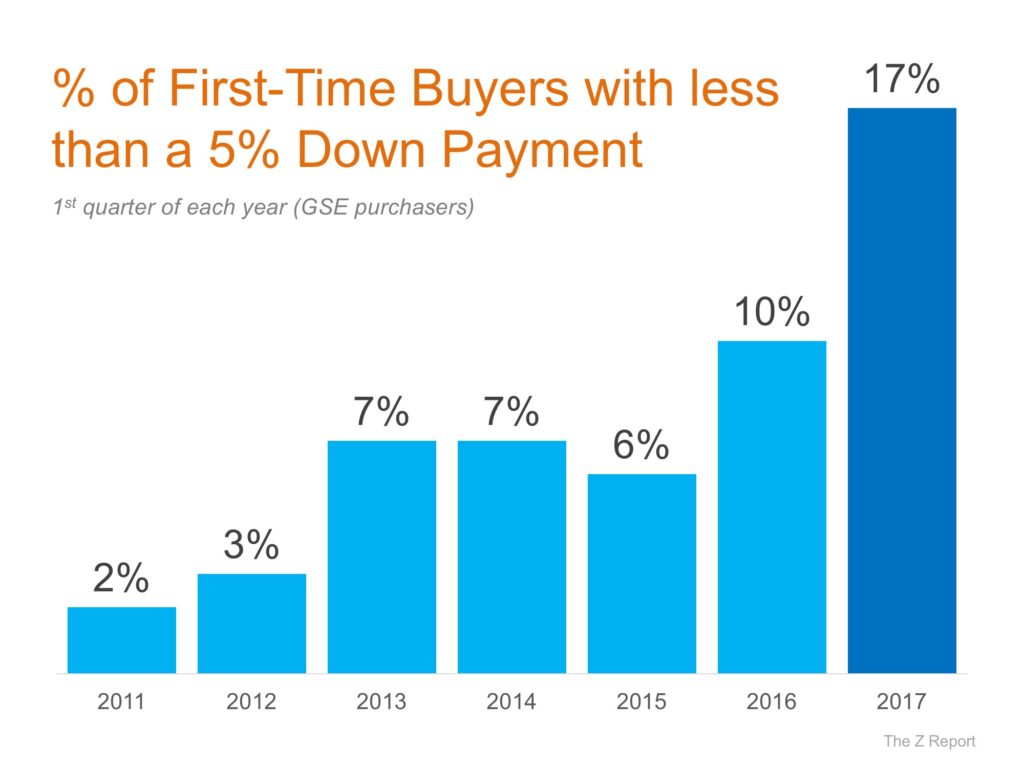

A report released by Down Payment Resource shows that 61% of first-time homebuyers purchased their homes with a down payment of 6% or less.

The trend continued among all buyers with a mortgage, as 73% made a down payment of less than 20%.

An article by Chase points to a new wave of millennial homebuyers:

“We teamed up with Google to help us better understand what customers are searching for and how the home buying landscape is evolving. We found that millennials and first-time homebuyers are making a big splash in the market, and affordability remains top of mind.”

Among millennials who purchased homes, David Norris, Loan Depot’s Head of Retail Lending, said:

“It’s clear from the survey results that Millennials have a lot of anxiety built up about the home buying process.

There is good news, however, as there’s more flexibility than most Millennials think regarding how to qualify for a loan and what’s needed for a down payment.”

If you are one of the many millennials who is debating a home purchase this year, let’s get together to help you understand your options and set you on the path to preapproval.

Posted in Buying Myths, Down Payments, First Time Home Buyers, For Buyers, Millennials, Move-Up Buyers

The Aspiring Home Buyers Profile from the National Association of Realtors (NAR) found that the American public is still somewhat confused about what is required to qualify for a home mortgage loan in today’s housing market. The results of the survey show that non-homeowners cite the main reason for not currently owning a home, as not being able to afford one.

This brings us to two major misconceptions that we want to address today.

NAR’s survey revealed that consumers overestimate the down payment funds needed to qualify for a home loan. According to the report, 39% of non-homeowners say they believe they need more than 20% for a down payment on a home purchase. In actuality, there are many loans written with a down payment of 3% or less.

Many renters may actually be able to enter the housing market sooner than they ever imagined with new programs that have emerged allowing less cash out of pocket.

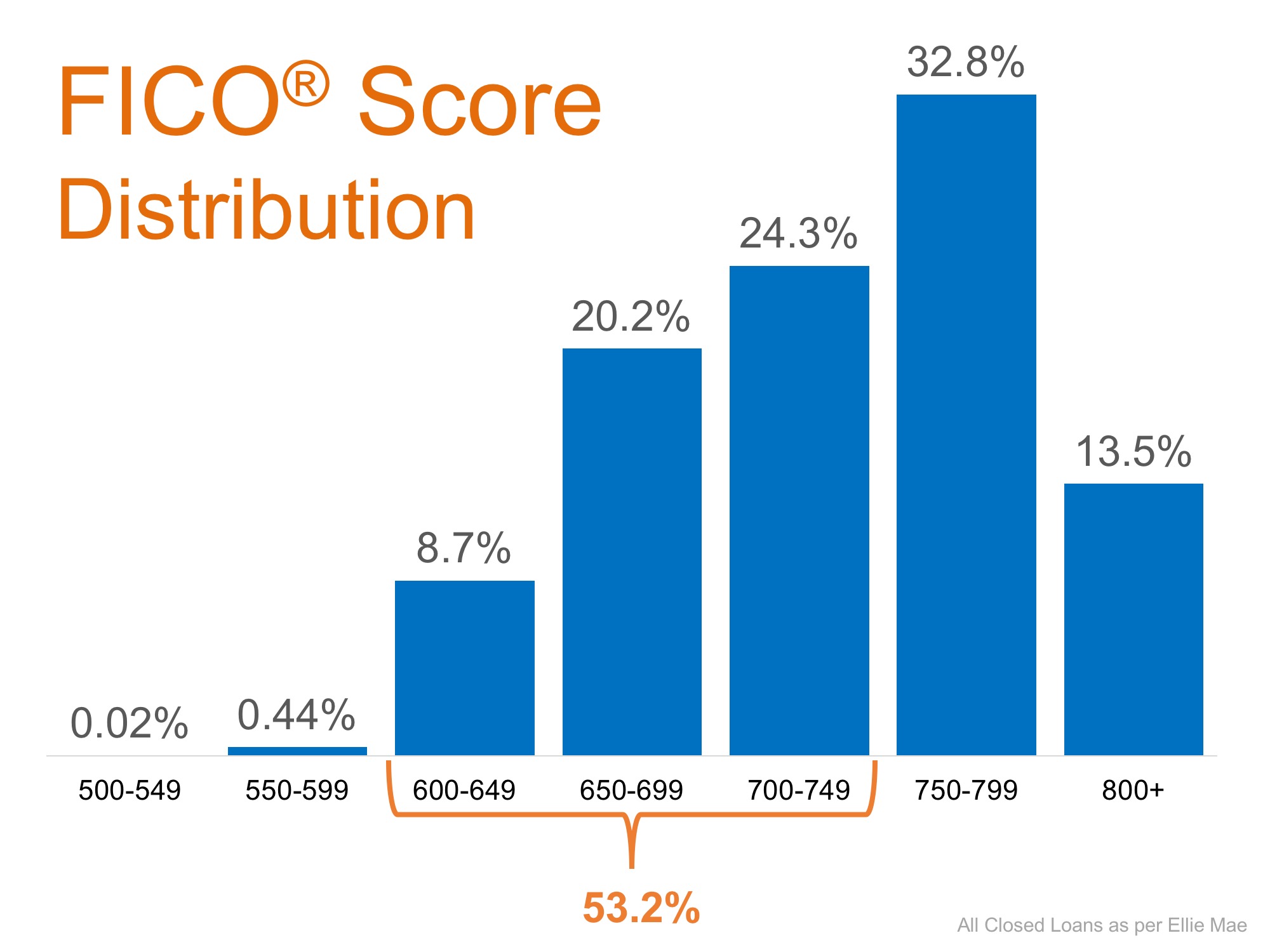

An Ipson survey revealed that 62% of respondents believe they need excellent credit to buy a home, with 43% thinking a “good credit score” is over 780. In actuality, the average FICO® scores of approved conventional and FHA mortgages are much lower.

The average conventional loan closed in August had a credit score of 752, while FHA mortgages closed with a score of 683. The average across all loans closed in August was 724. The chart below shows the distribution of FICO® Scores for all loans approved in August.

If you are a prospective buyer who is ‘ready’ and ‘willing’ to act now, but are not sure if you are ‘able’ to, let’s sit down to help you understand your true options.

Posted in Down Payments, First Time Home Buyers, For Buyers, Move-Up Buyers

According to Black Knight Financial Service’s Mortgage Monitor Report, 1.5 million Americans have purchased a home with down payments under than 10% over the last 12 months. This is great news for buyers as this marks a 7-year high.

Many mortgage programs offered by agencies like Freddie Mac and Fannie Mae allow buyers to put down as low as 3% to purchase their dream homes. The strength of the housing market has aided buyers who used low-down-payment programs to buy. As a recent CNBC article points out,

“Defaults on recent low down payment loans, so far, are slow, but that is as much a factor of the good credit quality as it is the strength of the housing market. Home prices are rising incredibly fast, meaning those borrowers are gaining equity in their homes quickly.”

Low down payments aren’t just great for first-time homebuyers. These programs have allowed homeowners who want to capitalize on the equity they have in their homes to use the profit from their sale to pay off high-interest credit cards, fund education or even start a business.

According to a new Census Report, the Annual Survey of Entrepreneurs, home equity was used to start 7.3% of all businesses in the United States, which equates to over 284,000! The industries that saw the most growth from home equity are accommodation & food services, manufacturing and, retail trade.

Gone are the days of ‘20% down or no mortgage.’ What could you build with the equity in your house? Let’s get together today to evaluate your ability to achieve your dreams today!

Posted in Down Payments, For Buyers, For Sellers, Move-Up Buyers

In Realtor.com’s recent article, “Home Buyers’ Top Mortgage Fears: Which One Scares You?” they mention that “46% of potential home buyers fear they won’t qualify for a mortgage to the point that they don’t even try.”

Buyers overestimate the down payment funds needed to qualify for a home loan. According to the First Quarter 2017 Homeownership Program Index (HPI) from Down Payment Resource, saving for a down payment was the barrier that kept 70% of renters from buying.

Rob Chrane, CEO of Down Payment Resource had this to say,

“There are many mortgage-ready renters today, but they don’t know it. Often, homebuyers remain sidelined for years due to the down payment.”

Many believe that they need at least 20% down to buy their dream home, but programs are available that allow buyers put down as little as 3%. Many renters may actually be able to enter the housing market sooner than they ever imagined with new programs that have emerged allowing less cash out of pocket.

The survey revealed that 59% of Americans either don’t know (54%) or are misinformed (5%) about what FICO® score is necessary to qualify.

Many Americans believe a ‘good’ credit score is 780 or higher.

To help debunk this myth, let’s take a look at Ellie Mae’s latest Origination Insight Report, which focuses on recently closed (approved) loans.

As you can see in the chart above, 53.2% of approved mortgages had a credit score of 600-749.

Whether buying your first home or moving up to your dream home, knowing your options will make the mortgage process easier. Your dream home may already be within your reach.

Posted in Down Payments, First Time Home Buyers, For Buyers, Move-Up Buyers

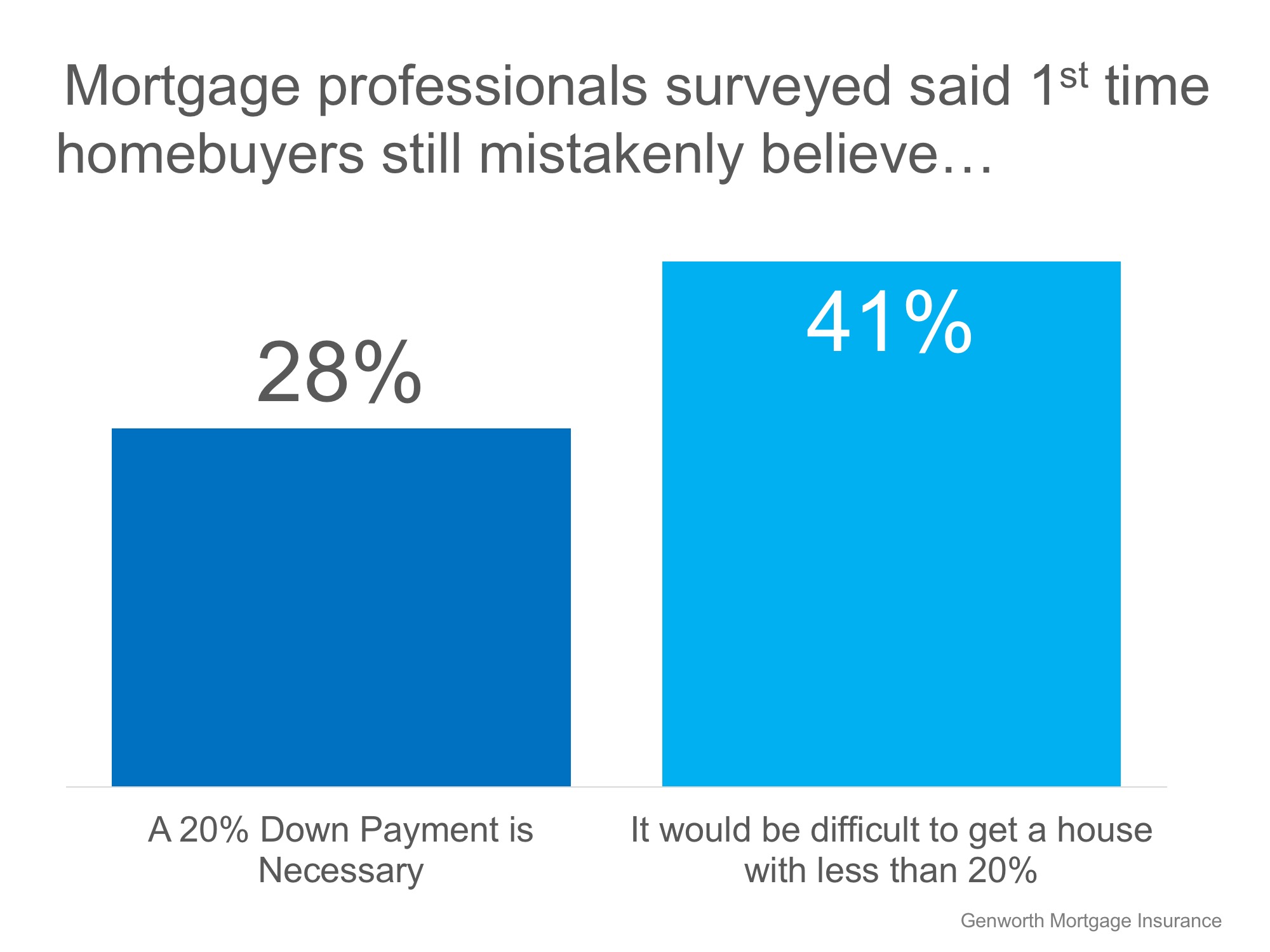

According to a recent survey conducted by Genworth Financial Inc. at the Annual Mortgage Bankers’ Association Secondary Market Conference, mortgage professionals say that first-time buyers still believe a 20% down payment is necessary to buy in today’s market.

Nearly 40% of mortgage industry professionals surveyed believe that a lack of knowledge about the home-buying process is keeping potential buyers on the sidelines. Saving for a down payment is often cited as a huge barrier for first-time homebuyers to make the leap into homeownership.

If homeowners believe that they need a 20% down payment to enter the market, they also believe that they will have to wait years (in some markets) to come up with the necessary funds to buy their dream homes.

The greatest source of confusion cited in the survey results centered around down payments. The results are broken down in the chart below:

Rohit Gupta, CEO of Genworth Mortgage Insurance had this to say,

“While first-time homebuyers continue to drive the purchase market, we believe many are staying on the sidelines due to the misconception that a 20 percent down payment is required to secure a mortgage.

There are various low down payment options available today that allow prospective homebuyers to reach their dreams of homeownership sooner. It is crucial that, as an industry, we proactively educate eligible borrowers about solutions that will enable them to buy a home when they’re ready.”

Don’t let a lack of understanding of the home-buying process keep you and your family out of the housing market. Let’s get together to discuss your options!

Posted in Down Payments, First Time Home Buyers, For Buyers, Move-Up Buyers

This time of year, many people eagerly check their mailboxes looking for their tax return check from the IRS. But, what do most people plan to do with the money? GO Banking Rates recently surveyed Americans and asked the question – “What do you plan on doing with your tax refund?”

The results of the survey were interesting. Here is what they plan to do with their money:

Upon seeing the research, The National Association of Realtors (NAR) wondered if this could help with a constant challenge cited by many people who wish to purchase a home – saving for the down payment.

In a recent post in NAR’s Economists’ Outlook Blog, they explained:

“With a sizable tax refund, the average American would have a decent down payment depending on which region or market you live in.”

They went on to add:

“[A]pproximately 5 percent of all respondents indicated they would make a major purchase which does not seem like a lot. However, there is a bigger group 41 percent who see saving the tax return is best and that group could be potential homebuyers if they are not already.”

In other words, putting that money toward purchasing a home is a form of savings.

When one considers that first-time home buyers in 2016 had an average down payment of 6%, a decent tax return could go a long way toward the necessary funds needed for a down payment on a house. Or perhaps, the down payment needed by a son or daughter to make their homeownership dream a reality. How are you going to spend your return?

Posted in Down Payments, First Time Home Buyers, For Buyers

Saving for a down payment is often the biggest hurdle for a first-time homebuyer. Depending on where you live, median income, median rents, and home prices all vary. So, we set out to find out how long would it take you to save for a down payment in each state?

Using data from the United States Census Bureau and Zillow, we determined how long it would take, nationwide, for a first-time buyer to save enough money for a down payment on their dream home. There is a long-standing ‘rule’ that a household should not pay more than 28% of their income on their monthly housing expense.

By determining the percentage of income spent renting a 2-bedroom apartment in each state, and the amount needed for a 10% down payment, we were able to establish how long (in years) it would take for an average resident to save enough money to buy a home of their own.

According to the data, residents in Iowa can save for a down payment the quickest in just under 2 years (1.99). Below is a map created using the data for each state:

What if you were able to take advantage of one of Freddie Mac’s or Fannie Mae’s 3% down programs? Suddenly, saving for a down payment no longer takes 5 or 10 years, but becomes attainable in a year or two in many states as shown in the map below.

Whether you have just started to save for a down payment, or have been saving for years, you may be closer to your dream home than you think! Let’s meet up so I can help you evaluate your ability to buy today.

Posted in Down Payments, First Time Home Buyers, For Buyers

Posted in Down Payments, First Time Home Buyers, For Buyers, Infographics, Interest Rates

The media has extensively covered the rise in mortgage interest rates since last fall (from 3.42% last September to the current 4.1% according to Freddie Mac). However, a less covered aspect of the mortgage market is that requirements to get a mortgage have eased while rates have risen.

The Mortgage Bankers Association (MBA) quantifies the availability of mortgage credit each month with their Mortgage Credit Availability Index (MCAI). According to the MBA, the MCAI is:

“A summary measure which indicates the availability of mortgage credit at a point in time.”

The higher the index, the easier it is to get a mortgage. Here is a chart showing the MCAI over the last several months as rates have increased.

Yes. Here are two examples:

Whether you are a current homeowner looking to move to a home that will better serve your family’s current needs, or a first-time buyer looking for a starter home, it is easier to get a mortgage today than it has been at any other time in the last ten years.

Posted in Down Payments, First Time Home Buyers, For Buyers, Interest Rates, Move-Up Buyers

For your home value estimate, enter the access code you received on the postcard, just click here: