Instant Home Estimate

For your home value estimate, enter the access code you received on the postcard, just click here:

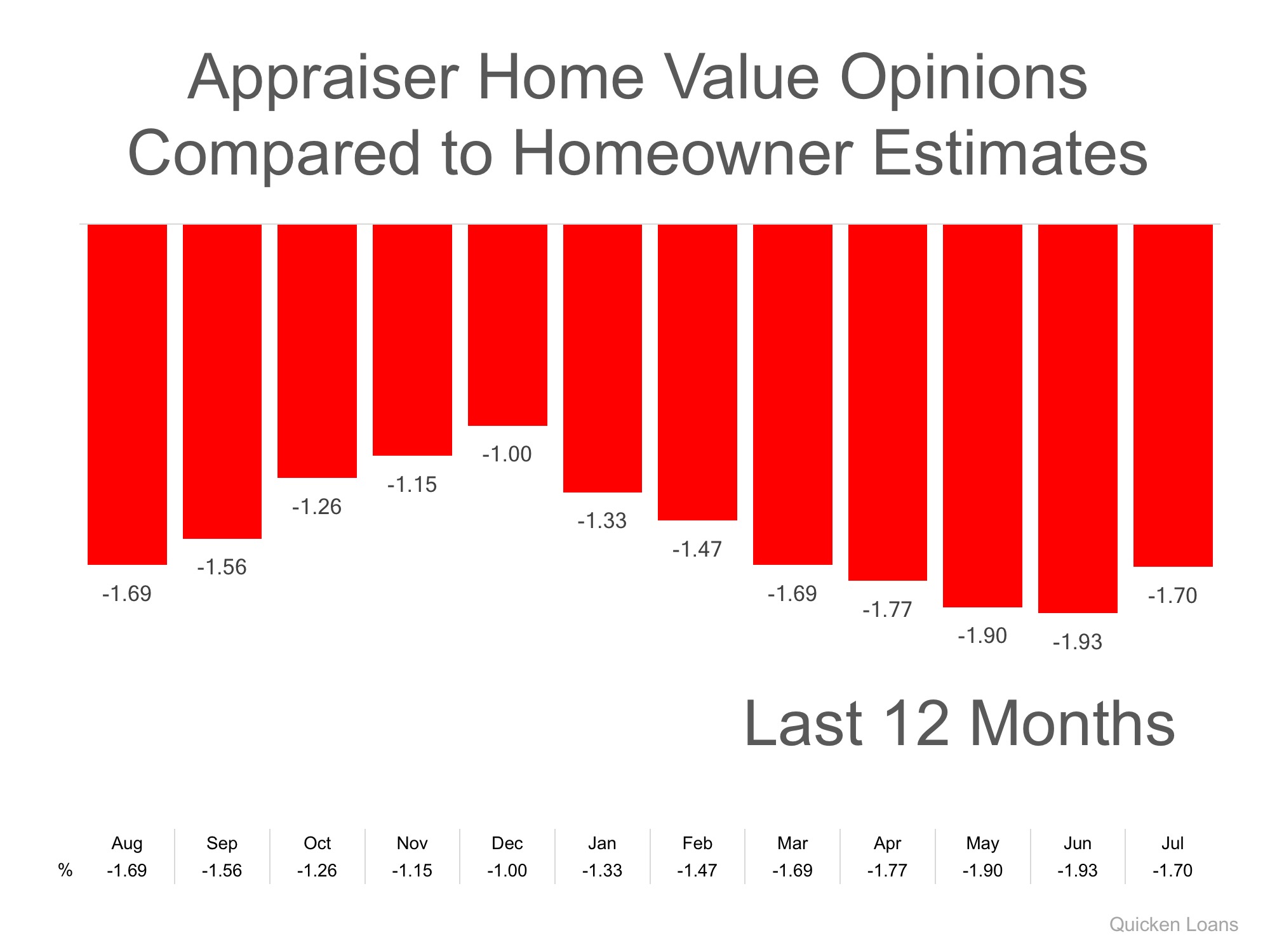

In today’s housing market, where supply is very low and demand is very high, home values are increasing rapidly. Many experts are projecting that home values could appreciate by another 5%+ over the next twelve months. One major challenge in such a market is the bank appraisal.

If prices are surging, it is difficult for appraisers to find adequate, comparable sales (similar houses in the neighborhood that recently closed) to defend the selling price when performing the appraisal for the bank.

Every month in their Home Price Perception Index (HPPI), Quicken Loans measures the disparity between what a homeowner who is seeking to refinance their home believes their house is worth, as compared to an appraiser’s evaluation of that same home.

Bill Banfield, VP of Capital Markets at Quicken Loans urges anyone looking to buy or sell in today’s market to remember the impact of this challenge:

“While a 1 or 2 percent difference in home value opinions may not seem like a lot, it could be enough to derail a mortgage.

A homeowner [or a buyer] could be forced to bring more cash to closing in order to make a mortgage work if the appraisal is lower than expected. On the other hand, if an appraisal comes in higher, they could be surprised with more equity than they had planned. Either way, if owners are aware of their local markets it will lead to smoother mortgage transactions.”

The chart below illustrates the changes in home price estimates over the last 12 months.

Every house on the market has to be sold twice; once to a prospective buyer and then to the bank (through the bank’s appraisal). With escalating prices, the second sale might be even more difficult than the first. If you are planning on entering the housing market this year, let’s get together to discuss this and any other obstacle that may arise.

Posted in For Sellers

In today’s market, with home prices rising and a lack of inventory, some homeowners may consider trying to sell their homes on their own, known in the industry as a For Sale by Owner (FSBO). There are several reasons why this might not be a good idea for the vast majority of sellers.

Here are the top five reasons:

Recent studies have shown that 94% of buyers search online for a home. That is in comparison to only 16% looking at print newspaper ads. Most real estate agents have an internet strategy to promote the sale of your home. Do you?

Where did buyers find the homes they actually purchased?

The days of selling your house by just putting up a sign and putting it in the paper are long gone. Having a strong internet strategy is crucial.

Here is a list of some of the people with whom you must be prepared to negotiate if you decide to For Sale by Owner:

The paperwork involved in selling and buying a home has increased dramatically as industry disclosures and regulations have become mandatory. This is one of the reasons that the percentage of people FSBOing has dropped from 19% to 8% over the last 20+ years.

The 8% share represents the lowest recorded figure since NAR began collecting data in 1981.

Many homeowners believe that they will save the real estate commission by selling on their own. Realize that the main reason buyers look at FSBOs is because they also believe they can save the real estate agent’s commission. The seller and buyer can’t both save the commission.

Studies have shown that the typical house sold by the homeowner sells for $185,000, while the typical house sold by an agent sells for $245,000. This doesn’t mean that an agent can get $60,000 more for your home, as studies have shown that people are more likely to FSBO in markets with lower price points. However, it does show that selling on your own might not make sense.

Before you decide to take on the challenges of selling your house on your own, let’s get together and discuss the options available in your market today.

Posted in For Sellers, FSBOs

Posted in For Buyers, For Sellers, Infographics

The Joint Center of Housing Studies (JCHS) at Harvard University recently released their 2017 State of the Nation’s Housing Study, and a recent blog from JCHS revealed some of the more surprising aspects of the study.

The first two revelations centered around the shortage of housing inventory currently available in both existing homes and new construction.

“For the fourth year in a row, the inventory of homes for sale across the US not only failed to recover, but dropped yet again. At the end of 2016 there were historically low 1.65 million homes for sale nationwide, which at the current sales rate was just 3.6 months of supply – almost half of the 6.0 months level that is considered a balanced market.”

“Markets nationwide are still feeling the effects of the deep and extended decline in housing construction. Over the past 10 years, just 9 million new housing units were completed and added to the housing stock. This was the lowest 10-year period on records dating back to the 1970s, and far below the 14 and 15 million units averaged over the 1980s and 1990s.”

The biggest challenge in today’s market is getting current homeowners and builders to realize the opportunity they have to maximize profit by selling and/or building NOW!!

Posted in For Sellers, Housing Market Updates, New Construction

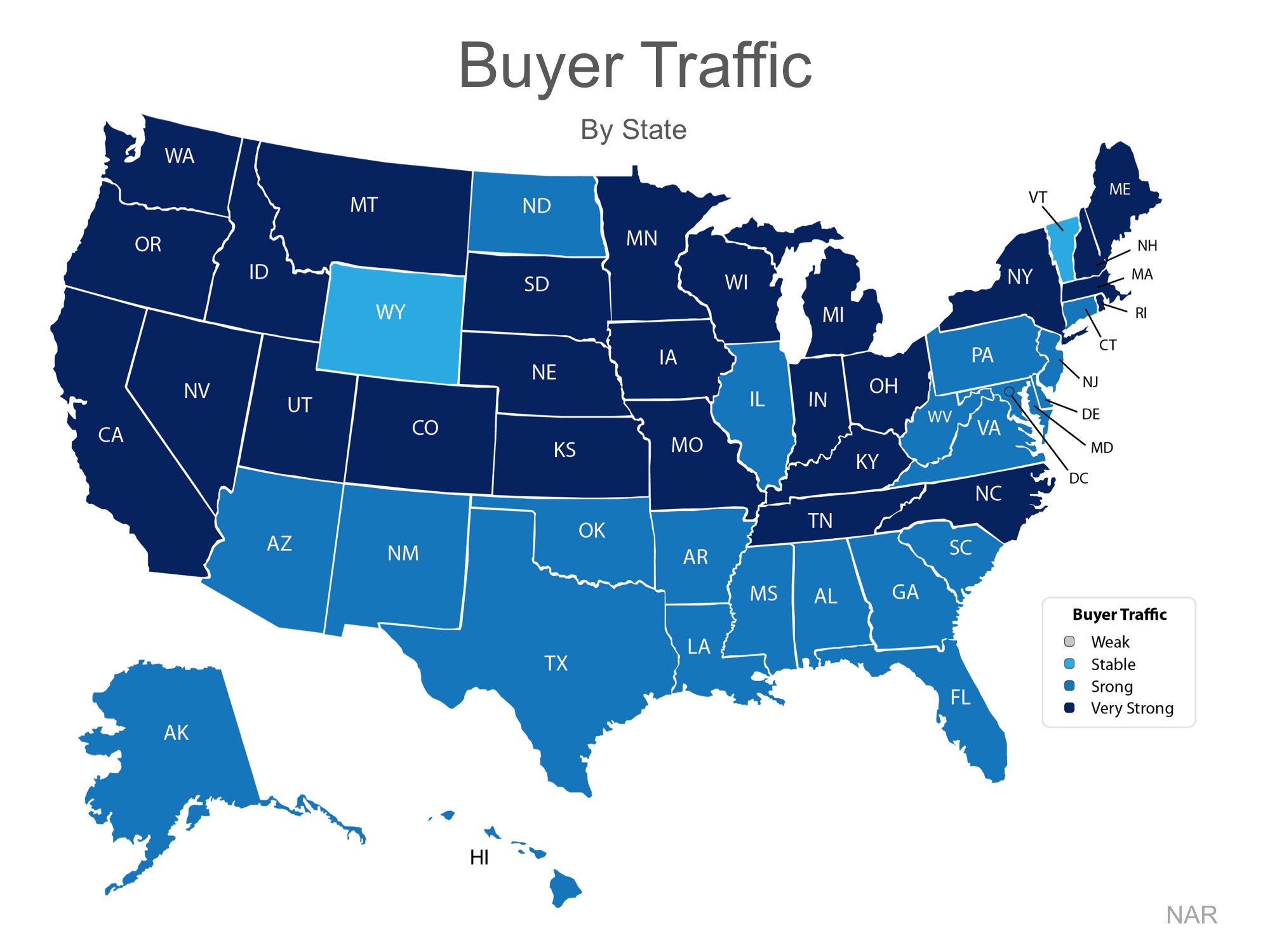

We all realize that the best time to sell anything is when demand is high and the supply of that item is limited. Two major reports issued by the National Association of Realtors (NAR) revealed information that suggests that now continues to be a great time to sell your house.

Let’s look at the data covered in the latest REALTORS® Confidence Index and Existing Home Sales Report.

Every month, NAR surveys “over 50,000 real estate practitioners about their expectations for home sales, prices and market conditions.” This month, the index showed (again) that home-buying demand continued to outpace supply in May.

The map below illustrates buyer demand broken down by state (the darker your state, the stronger the demand is there).

In addition to revealing high demand, the index also mentioned that “compared to conditions in the same month last year, seller traffic conditions were ‘weak’ in 24 states, ‘stable’ in 25 states, and ‘strong’ in D.C and West Virginia.”

Takeaway: Demand for housing continues to be strong throughout 2017, but supply is struggling to keep up, and this trend is likely to continue into 2018.

The most important data revealed in the report was not sales, but was instead the inventory of homes for sale (supply). The report explained:

According to Lawrence Yun, Chief Economist at NAR:

“Current demand levels indicate sales should be stronger, but it’s clear some would-be buyers are having to delay or postpone their home search because low supply is leading to worsening affordability conditions.”

In real estate, there is a guideline that often applies; when there is less than a 6-month supply of inventory available, we are in a seller’s market and we will see appreciation. Between 6-7 months is a neutral market, where prices will increase at the rate of inflation. More than a 7-month supply means we are in a buyer’s market and should expect depreciation in home values.

As we mentioned before, there is currently a 4.2- month supply, and houses are going under contract fast. The Confidence Index shows that 55% of properties were on the market for less than a month when sold.

In May, properties sold nationally were typically on the market for 27 days. As Yun notes, this will continue, unless more listings come to the market.

“With new and existing supply failing to catch up with demand, several markets this summer will continue to see homes going under contract at this remarkably fast pace of under a month.”

Takeaway: Inventory of homes for sale is still well below the 6-month supply needed for a normal market. And the supply will continue to ‘fail to catch up with demand’ if a ‘sizable’ supply does not enter the market.

If you are going to sell, now may be the time to take advantage of the ready, willing, and able buyers that are still out searching for your house.

Posted in For Sellers, Housing Market Updates

Posted in For Buyers, For Sellers, Housing Market Updates, Infographics

The National Association of Realtors (NAR) recently released the findings of their Q2 Homeownership Opportunities and Market Experience (HOME) Survey. The report covers core topics like, “if now is a good time to buy or sell a home, the perception of home price changes, perceived ability to qualify for a mortgage, and [an] outlook on the U.S. economy.”

The survey revealed that 75% of homeowners think now is a good time to sell, compared to 70% last quarter. This is a considerable increase from more than a year ago when 66% agreed.

Even though homeowners believe that now is a good time to sell, many have not taken the step to list their homes, as inventory shortages still exist across the country. Lawrence Yun, NAR’s Chief Economist, had this to say:

“There are just not enough homeowners deciding to sell because they’re either content where they are, holding off until they build more equity, or hesitant seeing as it will be difficult to find an affordable home to buy…

As a result, inventory conditions have worsened and are restricting sales from breaking out while contributing to price appreciation that remains far above income growth.”

If you are wondering if now is a good time to sell your house, let’s get together to discuss the opportunities available in our market.

Posted in For Sellers

We previously reported how a shortage of inventory in the starter and trade-up home markets is driving prices up and causing bidding wars, creating a true seller’s market. At the same time, in the premium home market, an over-abundance of inventory has started to see prices come down and put buyers in the driver’s seat, creating the beginning of a buyer’s market.

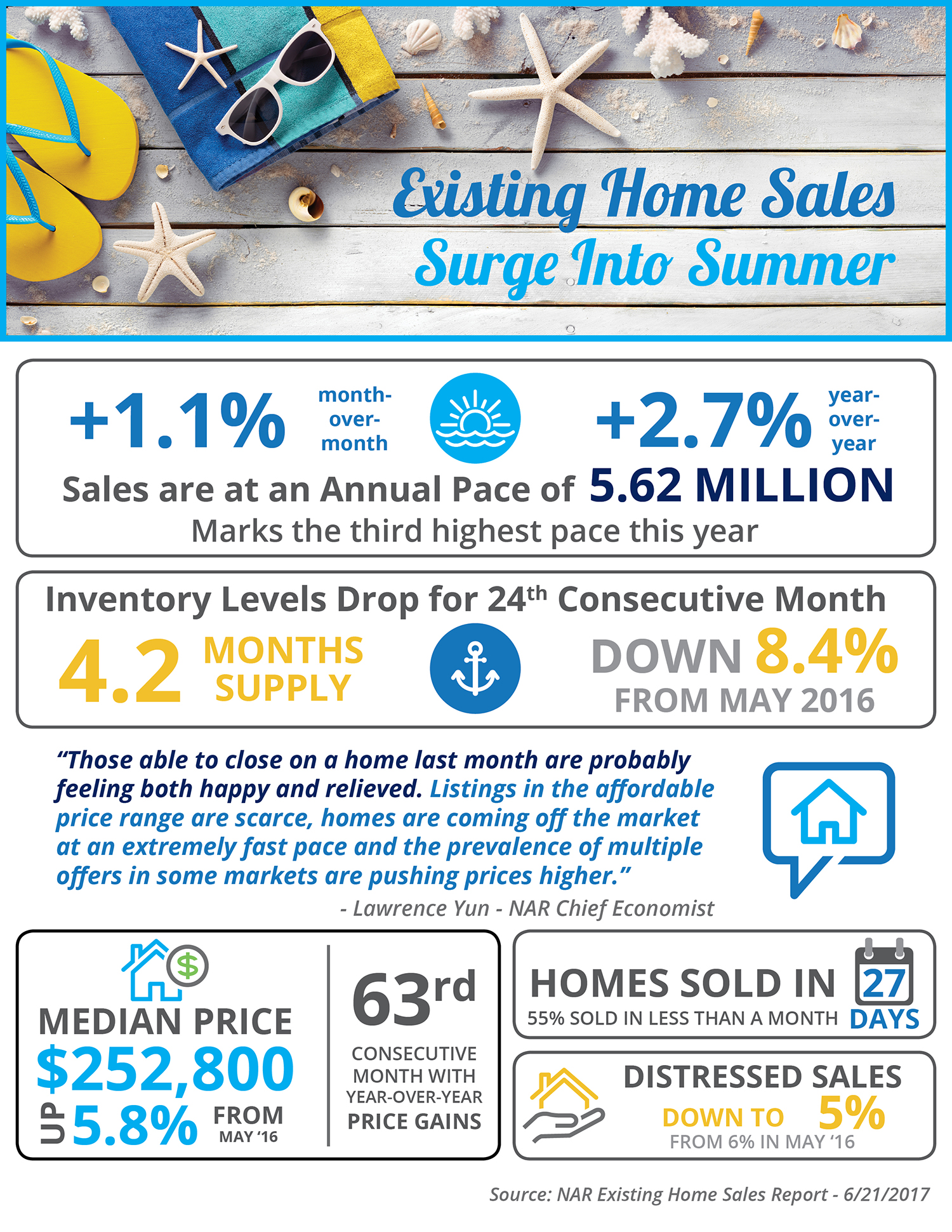

Last week, the National Association of Realtors released their Existing Home Sales Report which shed some additional light on the impact of inventory levels on sales in each price range.

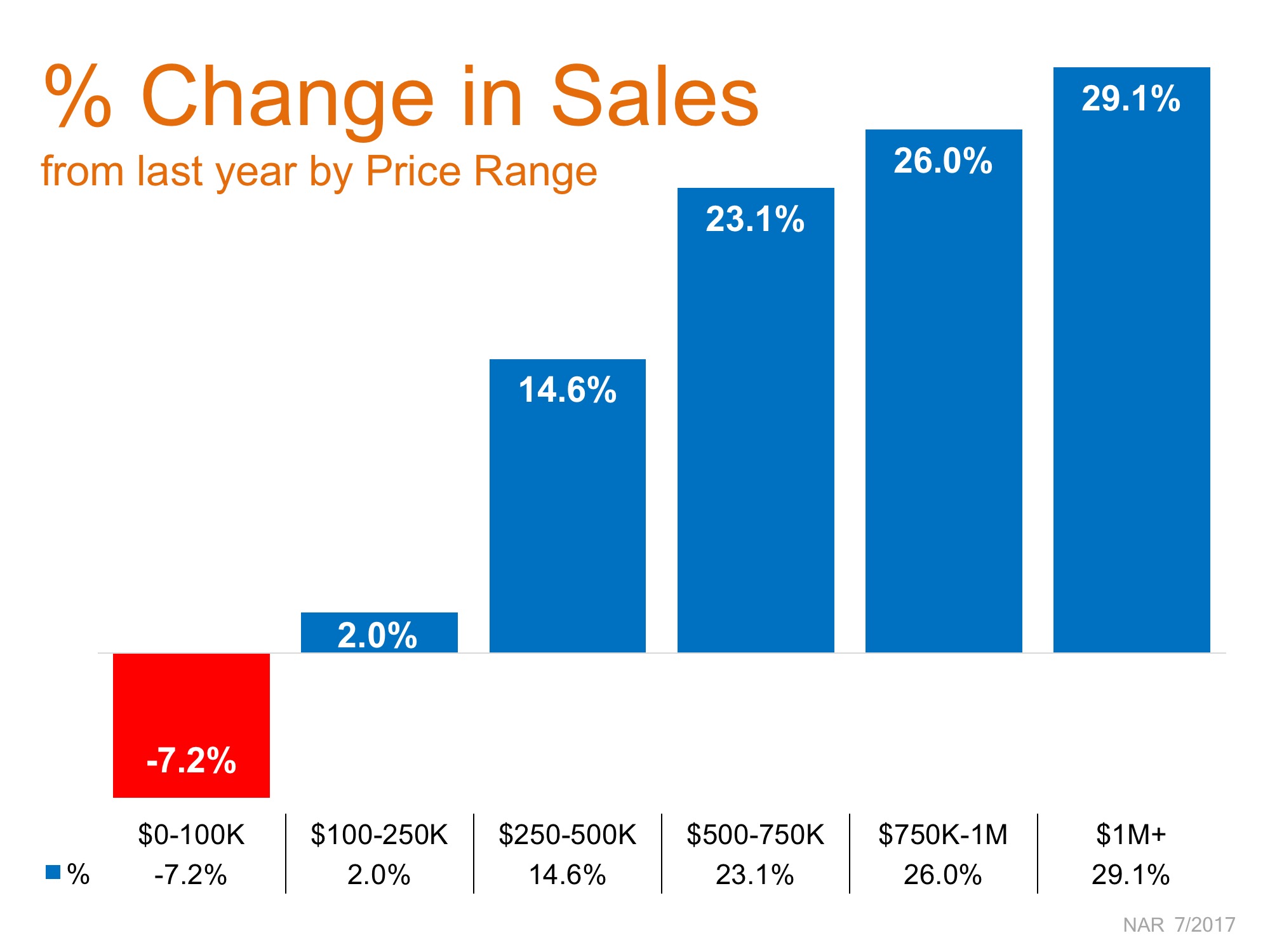

The chart below shows the year-over-year difference in sales at each price range.

The under $100K range has shown declines in recent years due to the shortage of distressed homes available for sale (just 5% of sales this past month, compared to 35% in January 2012). Sales in the next two price ranges are no doubt being hindered by low inventory as buyers compete for the same home.

NAR’s Chief Economist, Lawrence Yun, explained:

“Those able to close on a home last month are probably feeling both happy and relieved. Listings in the affordable price range are scarce, homes are coming off the market at an extremely fast pace and the prevalence of multiple offers in some markets are pushing prices higher.”

The biggest surprise? This is the first time in years where the $1M and up price range had the highest jump in sales when compared to last year and to all other price ranges (29.1%)! The two price ranges right underneath the $1M range were a close second and third. As the price went up, so did the sales!

With additional inventory available in the higher price ranges, and the economy improving, many luxury buyers are finding it easier to find their dream homes. Yun commented,

“The job market in most of the country is healthy and the recent downward trend in mortgage rates continues to keep buyer interest at a robust level.”

If you are one of the many homeowners who is looking to sell your starter or trade up home and move up to a luxury home, now is the time!

Posted in First Time Home Buyers, For Buyers, For Sellers, Move-Up Buyers

We often discuss the difference in family wealth between homeowner households and renter households. Much of that difference is the result of the equity buildup that homeowners experience over the time that they own their home. In a report recently released by the nonpartisan Employee Benefit Research Institute (EBRI), they reveal how valuable equity can be in retirement planning.

Craig Copeland, Senior Research Associate at EBRI, recently authored a report, Importance of Individual Account Retirement Plans and Home Equity in Family Total Wealth, in which he reveals:

“Individual account retirement plan assets, plus home equity, represent almost all of what families have to use for retirement expenses outside of Social Security and traditional pensions. Those families without individual account assets typically have very low overall assets, so they have almost nothing to draw from for retirement expenses.”

The report echoed the findings of a working paper, Home Equity Patterns among Older American Households, authored by Barbara Butrica and Stipica Mudrazija of Urban Institute. Fannie Mae highlighted these findings for their blog The Home Story this past winter, quoting Butrica and Mudrazija:

“For most adults near traditional retirement age, a home is their most valuable asset — dwarfing retirement accounts, other financial assets, and other nonfinancial assets. Although relatively few retirees tap into their home equity, having it provides financial security… In fact, many retirement security experts argue that the conventional three-legged stool of retirement resources — Social Security, pensions, and savings — is incomplete because it ignores the home.”

USAToday interviewed two area experts to comment on the EBRI report. Randy Bruns, a private wealth adviser with HighPoint Planning Partners, agreed with the findings:

“Social Security and home equity are major pieces of the retirement puzzle.”

Wade Pfau, Professor of Retirement Income at The American College of Financial Services and author of “Reverse Mortgages: How to use Reverse Mortgages to Secure Your Retirement,” said having the equity without a plan to use it won’t help:

“Home equity is a very important asset for American retirees, and so it is important to think about how to make best use of home equity in retirement planning.”

Whether you use the equity in your home through a reverse mortgage or by selling and downsizing to a less expensive home, it should be a crucial piece of your retirement planning.

Posted in For Buyers, For Sellers

CoreLogic’s latest Equity Report revealed that 91,000 properties regained equity in the first quarter of 2017. This is great news for the country, as 48.2 million of all mortgaged properties are now in a positive equity situation.

Frank Nothaft, CoreLogic’s Chief Economist, explains:

“One million borrowers achieved positive equity over the last year, which means risk continues to steadily decline as a result of increasing home prices.”

Frank Martell, President and CEO of CoreLogic, believes this is a great sign for the market in 2017 as well, as he had this to say:

“Homeowner equity increased by $766 billion over the last year, the largest increase since Q2 2014. The rising cushion of home equity is one of the main drivers of improved mortgage performance. Since home equity is the largest source of homeowner wealth, the increase in home equity also supports consumer balance sheets, spending and the broader economy.”

According to the Fannie Mae’s Home Purchase Sentiment Index (HPSI), more homeowners are beginning to realize that they may have more equity than they first thought.

“This is only the second time in the survey’s history that the net share of those saying it’s a good time to sell surpassed the net share of those saying it’s a good time to buy.”

This means that many Americans with a mortgage have an opportunity to take advantage of today’s seller’s market. With a sizeable equity position, many homeowners could easily move into a housing situation that better meets their current needs (moving to a larger home or downsizing).

Doug Duncan, Senior Vice President and Chief Economist at Fannie Mae spoke out on this issue:

“High home prices have led many consumers to give us the first clear indication we’ve seen in the National Housing Survey’s seven-year history that they think it’s now a seller’s market. However, we continue to see a lack of housing supply as many potential sellers are unwilling or unable to put their homes on the market…”

If you are one of the many Americans who is unsure of how much equity you have built in your home, don’t let that be the reason you fail to move on to your dream home in 2017! Let’s get together to evaluate your situation!

Posted in For Buyers, For Sellers, Move-Up Buyers

For your home value estimate, enter the access code you received on the postcard, just click here: