Instant Home Estimate

For your home value estimate, enter the access code you received on the postcard, just click here:

Mortgage interest rates have already risen by over a quarter of a percentage point in 2018. Many are projecting that rates could increase to 5% by the end of the year.

Many quickly jump to the conclusion that an increase in mortgage rates will have a detrimental impact on real estate prices as fewer buyers will be able to qualify for a loan. This seems logical; if there is less demand for housing then prices will drop.

However, in a good economy, rising mortgage rates increase demand as many prospective purchasers immediately jump off the fence to guarantee they get the lower rate.

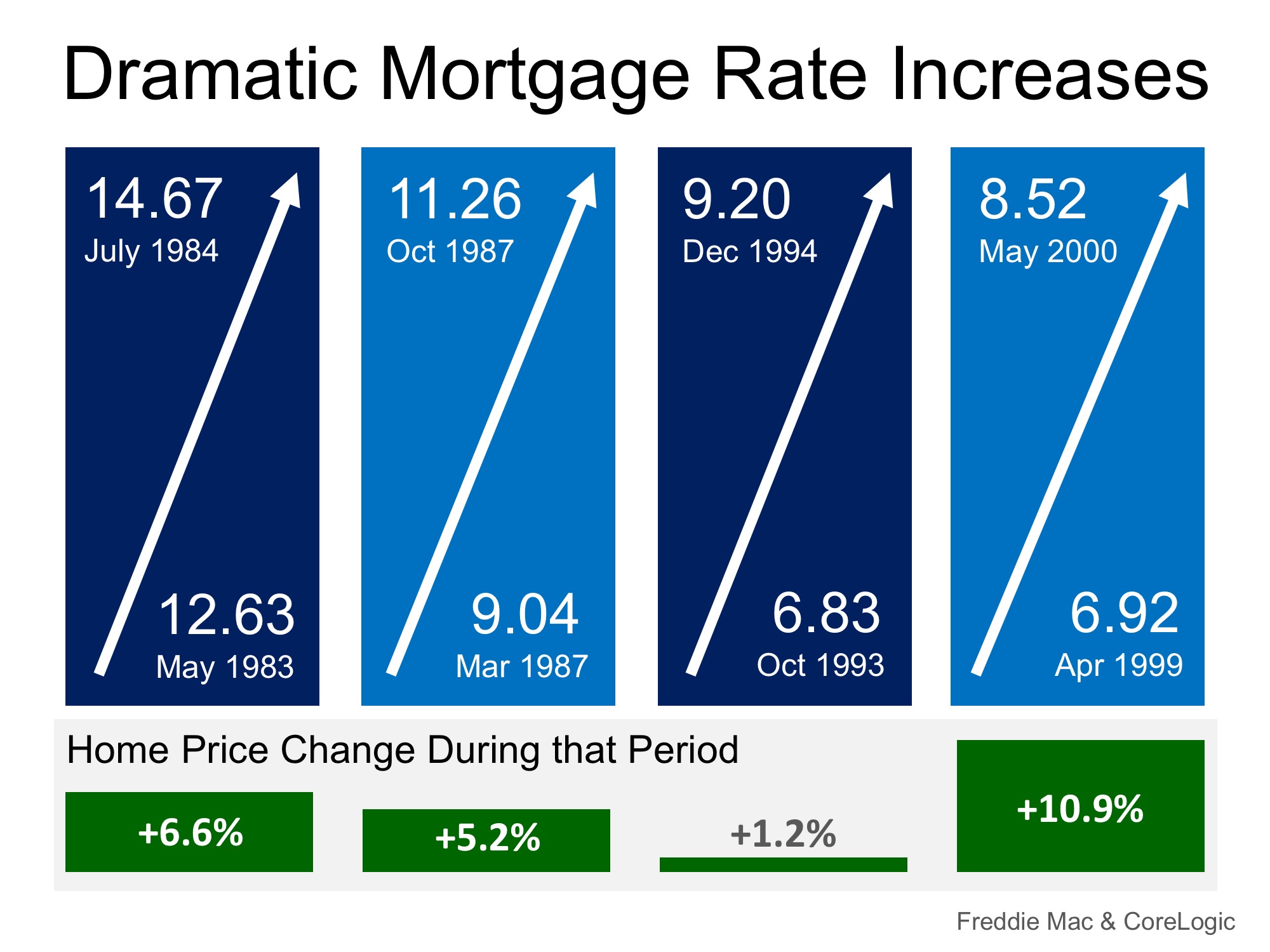

Let’s look at home prices the last four times mortgage rates increased dramatically.

In each case, home prices APPRECIATED and did not depreciate. No one is projecting as dramatic an increase in rates as the examples above. Most are projecting an increase of approximately 1% by the end of the year.

The last time mortgage rates increased by 1% over a twelve-month period was January 2013 (3.41%) to January 2014 (4.43%). What happened to house prices during that span? They appreciated by 9.8%.

Just two weeks ago, Rick Palacios Jr., Director of Research at John Burns Real Estate Consulting explained:

“Mortgage rates have risen 1% or more ten times in the last 43 years, with little impact on home sales and prices when the economy was also strong…Historically, rising confidence, solid job growth, and higher wages have more than offset reduced demand for housing resulting from higher mortgage rates.”

When mortgage rates increase, history has shown that prices appreciate (and do not depreciate) during that same time span.

Posted in First Time Home Buyers, For Buyers, For Sellers, Housing Market Updates, Interest Rates, Move-Up Buyers, Pricing

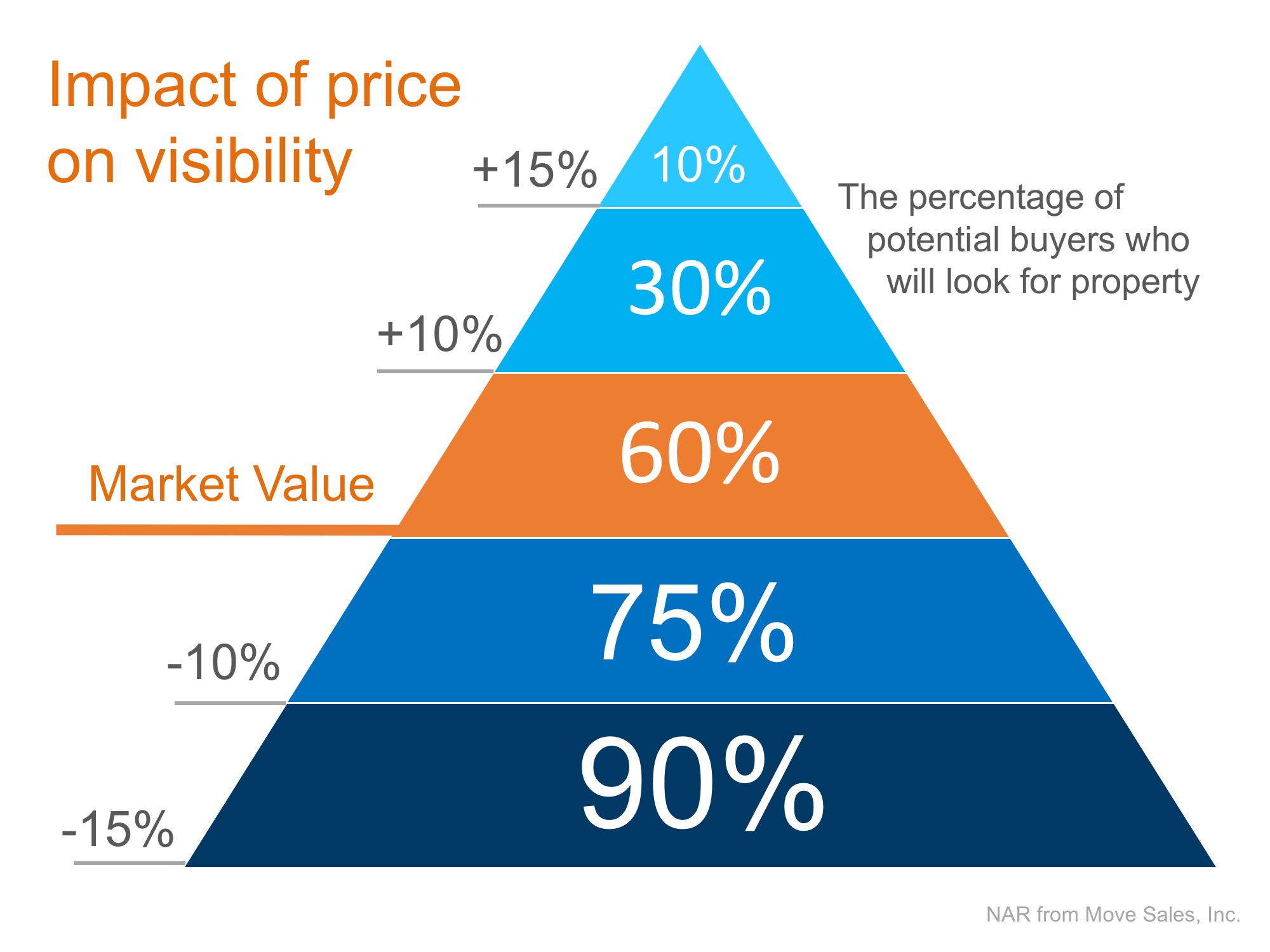

Every homeowner wants to make sure they maximize their financial reward when selling their home. But how do you guarantee that you receive the maximum value for your house?

Here are two keys to ensure that you get the highest price possible.

This may seem counterintuitive, but let’s look at this concept for a moment. Many homeowners think that pricing their homes a little OVER market value will leave them with room for negotiation. In actuality, this just dramatically lessens the demand for your house (see chart below).

Instead of the seller trying to ‘win’ the negotiation with one buyer, they should price it so that demand for the home is maximized. By doing this, the seller will not be fighting with a buyer over the price but will instead have multiple buyers fighting with each other over the house.

Realtor.com gives this advice:

“Aim to price your property at or just slightly below the going rate. Today’s buyers are highly informed, so if they sense they’re getting a deal, they’re likely to bid up a property that’s slightly underpriced, especially in areas with low inventory.”

This, too, may seem counterintuitive. The seller may think they would make more money if they didn’t have to pay a real estate commission. With this being said, studies have shown that homes typically sell for more money when handled by a real estate professional.

A study by Collateral Analytics, reveals that FSBOs don’t actually save any money, and in some cases may be costing themselves more, by not listing with an agent.

In the study, they analyzed home sales in a variety of markets in 2016 and the first half of 2017. The data showed that:

“FSBOs tend to sell for lower prices than comparable home sales, and in many cases below the average differential represented by the prevailing commission rate.”

The results of the study showed that the differential in selling prices for FSBOs when compared to MLS sales of similar properties is about 5.5%. Sales in 2017 suggest the average price was near 6% lower for FSBO sales of similar properties.

Price your house at or slightly below the current market value and hire a professional. This will guarantee that you maximize the price you get for your house.

Posted in For Sellers, FSBOs, Move-Up Buyers, Pricing, Selling Myths

Posted in First Time Home Buyers, For Buyers, Infographics, Interest Rates, Millennials, Move-Up Buyers, Pricing

According to CoreLogic’s latest Home Price Index, prices appreciated by 6.9% year-over-year from December 2016 to December 2017 on a national level. This marks the fifth month in a row with at least a 6.9% increase.

Dr. Frank Nothaft, Chief Economist for CoreLogic, gave insight into the reason behind the large appreciation,

“The number of homes for sale has remained very low. Job growth lowered the unemployment rate to 4.1 percent by year’s end, the lowest level in 17 years. Rising income and consumer confidence has increased the number of prospective homebuyers. The net result of rising demand and limited for-sale inventory is a continued appreciation in home prices.”

This is great news for homeowners who have gained nearly $15,000 in equity (on average) in their homes over the last year! Those homeowners who had been on the fence as to whether or not to sell will be pleasantly surprised to find out that they now have an even larger profit to help cover a down payment on their dream homes.

As we near the traditionally busy spring buyers season, there is still hope for buyers as mortgage rates remain low compared to recent decades. The report also predicted that home price appreciation will slow slightly, rising by 4.3% by this time next year.

If you are looking to enter the housing market, as either a buyer or a seller, let’s get together to go over exactly what’s going on in our neighborhood and discuss your options!

Posted in First Time Home Buyers, For Buyers, For Sellers, Move-Up Buyers, Pricing

Just like with any product or service, the law of supply and demand impacts home prices. Any time that there is less supply than the market demands, prices increase.

In many areas of the country, the supply of homes for sale in the starter and trade-up home markets is so low that bidding wars have ensued, and the busy spring-buying season is just around the corner.

CoreLogic recently conducted an analysis on national home prices at the time of sale for their January 2018 MarketPulse Report and found that a third of homes sold for at least list price.

“The share selling above list price was almost three times the trough in January 2008 and represented more than one-fifth of total sales.”

Many markets in the western part of the country and around major cities are experiencing higher shares of homes selling above list price.

“San Francisco had the largest share of homes—76 percent—that sold for at least the list price, and Seattle and Los Angeles followed with 63 and 51 percent, respectively. Miami had the lowest share—16 percent—of homes selling at or above the list price.”

Increased demand during the spring and summer months, the traditionally busier seasons for real estate, will no doubt influence how many homes continue to sell over list price.

This should not be seen by sellers as permission to overprice their homes, though. Buyers are becoming more and more educated, especially those who have been searching for their dream homes for a while now while waiting for new inventory to come to market.

Realtor.com gives this advice:

“Aim to price your property at or just slightly below the going rate. Today’s buyers are highly informed, so if they sense they’re getting a deal, they’re likely to bid up a property that’s slightly underpriced, especially in areas with low inventory.”

Without a large wave of new listings coming to market, buyers will continue competing with each other for the homes that are available. If you are thinking of selling your home, now may be the time to do so before more competition comes this spring. Let’s get together to determine the demand for your house in our area.

Posted in For Buyers, For Sellers, Move-Up Buyers, Pricing

In today’s housing market, where supply is very low and demand is very high, home values are increasing rapidly. Many experts are projecting that home values could appreciate by another 4% or more over the next twelve months. One major challenge in such a market is the bank appraisal.

When prices are surging, it is difficult for appraisers to find adequate, comparable sales (similar houses in the neighborhood that recently closed) to defend the selling price when performing the appraisal for the bank.

Every month in their Home Price Perception Index (HPPI), Quicken Loans measures the disparity between what a homeowner who is seeking to refinance their home believes their house is worth and what an appraiser’s evaluation of that same home is.

In the latest release, the disparity was the narrowest it has been in over two years, as the gap between appraisers and homeowners was only -0.5%. This is important for homeowners to note as even a .5% difference in appraisal can mean thousands of dollars that a buyer or seller would have to come up with at closing (depending on the price of the home)

The chart below illustrates the changes in home price estimates over the last two years.

Bill Banfield, Executive VP of Capital Markets at Quicken Loans urges homeowners to find out how their local markets have been impacted by supply and demand:

“Appraisers and real estate professionals evaluate their local housing markets daily. Homeowners, on the other hand, may only think about their housing market when they see ‘for sale’ signs hit front yards in the spring or when they think about accessing their equity.”

“With several years of growth, owners may have more equity than they realize. Many consumers use the tax season at the beginning of the year to reevaluate their entire financial life. It also provides a good opportunity for them to consider how best to take advantage of their equity while mortgage interest rates and borrowing costs are still near record lows.”

Every house on the market must be sold twice; once to a prospective buyer and then to the bank (through the bank’s appraisal). With escalating prices, the second sale might be even more difficult than the first. If you are planning on entering the housing market this year, let’s get together to discuss this and any other obstacles that may arise.

Posted in For Sellers, Move-Up Buyers, Pricing

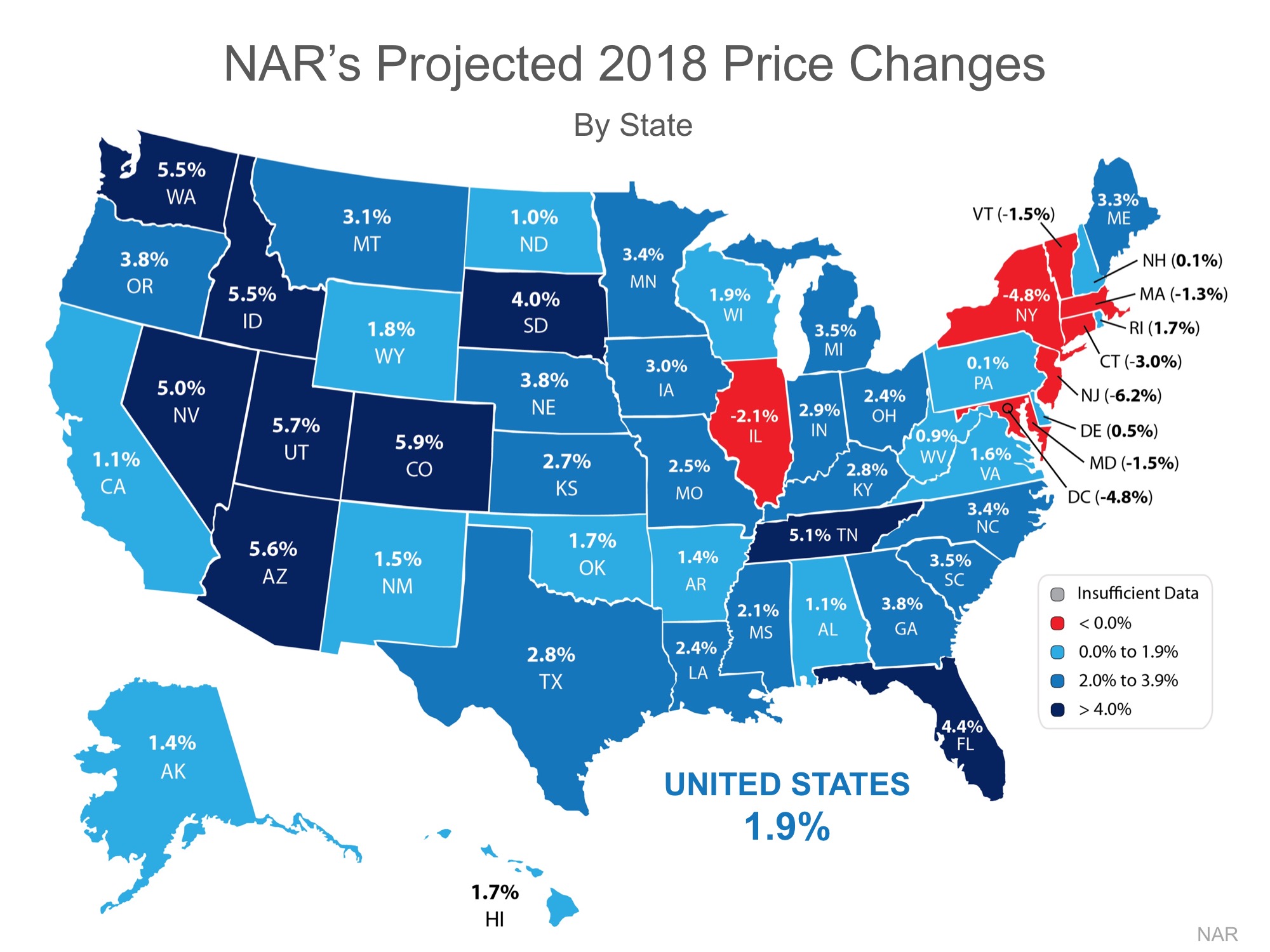

Every month, CoreLogic releases its Home Price Insights Report. In that report, they forecast where they believe residential real estate prices will be in twelve months.

Below is a map, broken down by state, reflecting how home values are forecasted to change by the end of 2018 using data from the most recent report.

As we can see, CoreLogic projects an increase in home values in 49 of 50 states, and Washington, DC (there was insufficient data for HI). Nationwide, they see home prices increasing by 4.2%.

Recently, the National Association of Realtors (NAR) conducted their own analysis to determine the impact the new tax code may have on home values. NAR’s analysis:

“…estimated how home prices will change in the upcoming year for each state, considering the impact of the new tax law and the momentum of jobs and housing inventory.”

Here is a map based on NAR’s analysis:

According to NAR, the new tax code will have an impact on home values across the country. However, the effect will be much less significant than what some originally thought.

Posted in First Time Home Buyers, For Buyers, For Sellers, Housing Market Updates, Move-Up Buyers, Pricing

As home values continue to increase at levels greater than historic norms, some are concerned that we are heading for another crash like the one we experienced ten years ago. We recently explained that the lenient lending standards of the previous decade (which created false demand) no longer exist. But what about prices?

Are prices appreciating at the same rate that they were prior to the crash of 2006-2008? Let’s look at the numbers as reported by Freddie Mac:

We must also realize that, to a degree, the current run-up in prices is the market trying to catch up after a crash that dramatically dropped prices for five years.

Prices are appreciating at levels greater than historic norms. However, we are not at the levels that led to the housing bubble and bust.

Posted in For Buyers, For Sellers, Housing Market Updates, Pricing

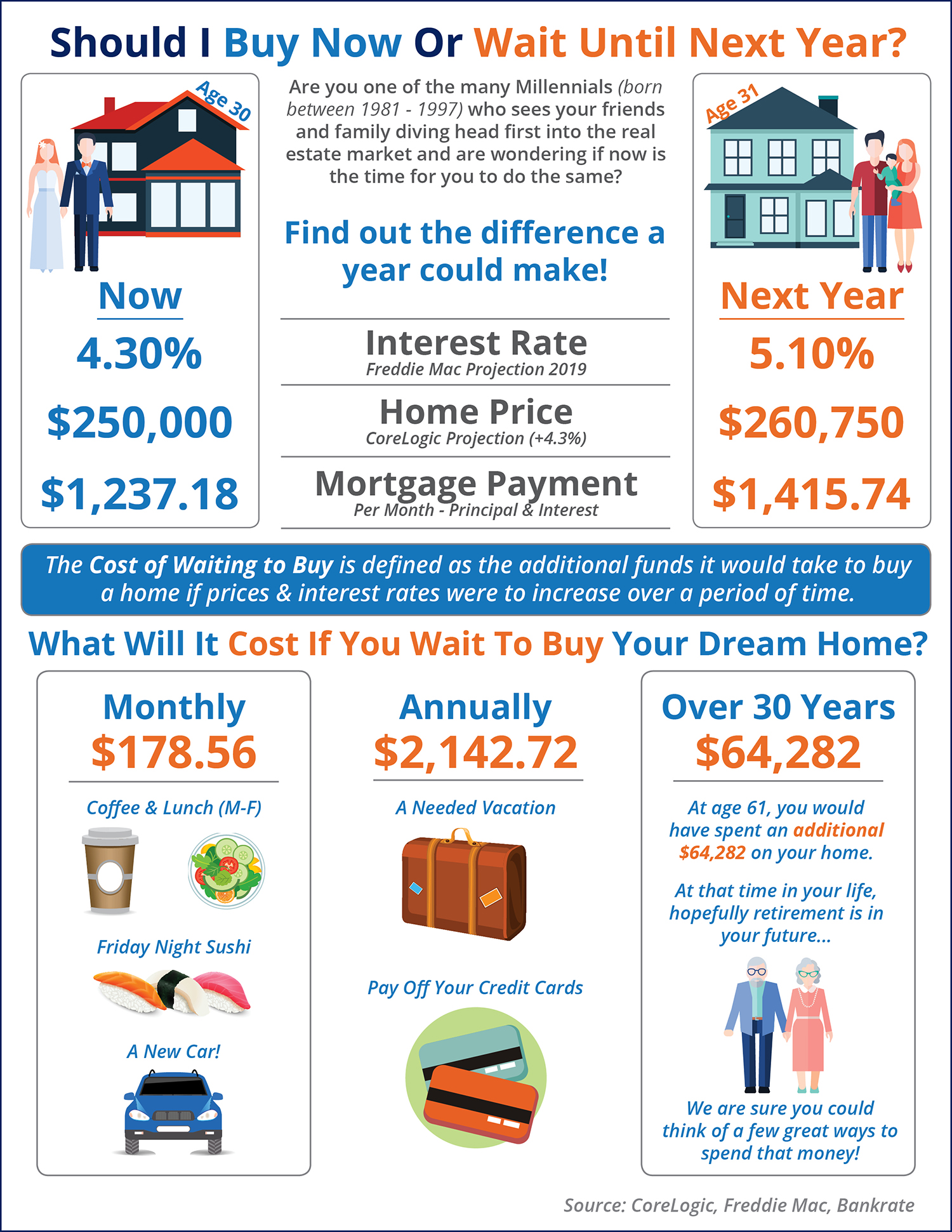

We recently shared that over the course of the last 12 months, home prices have appreciated by 7.0%. Over the same amount of time, interest rates have remained historically low which has allowed many buyers to enter the market.

As a seller, you will likely be most concerned about ‘short-term price’ – where home values are headed over the next six months. As a buyer, however, you must not be concerned about price, but instead about the ‘long-term cost’ of the home.

The Mortgage Bankers Association (MBA), Freddie Mac, and Fannie Mae all project that mortgage interest rates will increase by this time next year. According to CoreLogic’s most recent Home Price Index Report, home prices will appreciate by 4.7% over the next 12 months.

If home prices appreciate by 4.7% over the next twelve months as predicted by CoreLogic, here is a simple demonstration of the impact that an increase in interest rate would have on the mortgage payment of a home selling for approximately $250,000 today:

If buying a home is in your plan for 2018, doing it sooner rather than later could save you thousands of dollars over the terms of your loan.

Posted in First Time Home Buyers, For Buyers, For Sellers, Interest Rates, Move-Up Buyers, Pricing

According to CoreLogic’s latest Home Price Index, national home prices have appreciated by 7.0% from October 2016 to October 2017. This marks the second month in a row with a 7.0% year-over-year increase.

A lack of supply of homes for sale has led to upward pressure on home prices across the country, especially in areas where both existing and new home inventory have not kept up with buyer demand.

CoreLogic’s Chief Economist Frank Nothaft elaborated on the significance of such a large year-over-year gain,

“Single-family residential sales and prices continued to heat up in October. On a year-over-year basis, home prices grew in excess of 6 percent for four consecutive months ending in October, the longest such streak since June 2014.

This escalation in home prices reflects both the acute lack of supply and the strengthening economy.”

This is great news for homeowners who have gained over $13,000 in equity in their home over the last year! Those homeowners who had been on the fence as to whether or not to sell will be pleasantly surprised to find out that they now have an even larger profit to help cover a down payment on their dream home.

CoreLogic’s President & CEO Frank Martell had this to say,

“The acceleration in home prices is good news for both homeowners and the economy because it leads to higher home equity balances that support consumer spending and is a cushion against mortgage risk. However, for entry-level renters and first-time homebuyers, it leads to tougher affordability challenges.”

Any time the price of a home goes up there will likely be concern about the affordability of that home, but there is good news. Mortgage interest rates remain at historic lows, allowing buyers to enter the housing market and lock in a low monthly housing cost.

The report went on to mention that over the same 12-month period, median rental prices for a single-family home have also risen by 4.2%.

With rents and home prices rising at the same time, first-time buyers may find the task of saving for a down payment a little daunting. Low down payment programs are available and have been a very popular option for first-time buyers. The median down payment for first-time buyers in 2017 was only 5%!

If you are looking to enter the housing market, as either a buyer or a seller, let’s get together to go over exactly what’s going on in our neighborhood and discuss your options!

Posted in Down Payments, First Time Home Buyers, For Buyers, For Sellers, Move-Up Buyers, Pricing

For your home value estimate, enter the access code you received on the postcard, just click here: